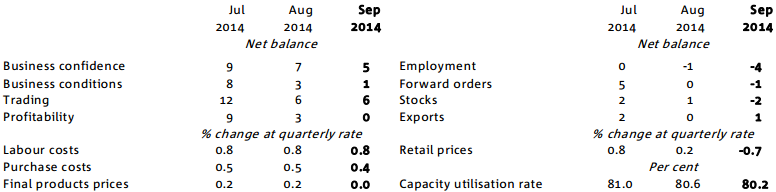

The September NAB business survey is out and the flush of post-election exuberance is fading as expected. Here are the key numbers:

Confidence down to 5 from 8 and 12 at the peak. Conditions down to 1 from 3 and 7 at the peak. Employment fell to -4 from -1. NAB reckons:

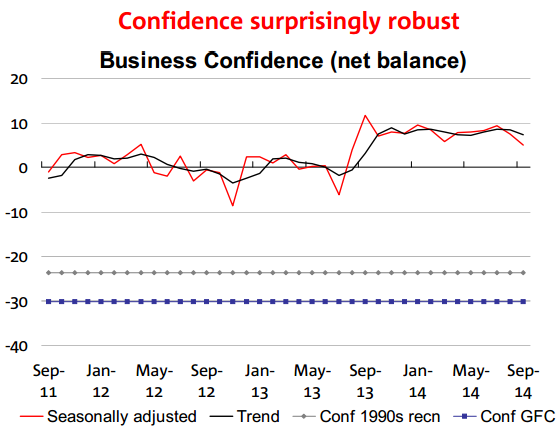

- Business confidence lost ground in September –lowest level since pre election – in the face of a persistently soft operating environment for many firms. Forward orders remained soft, prompting de-stocking and competitive pricing which appears to have weighed on profitability. Confidence varies significantly across industries, with services firms the most optimistic.

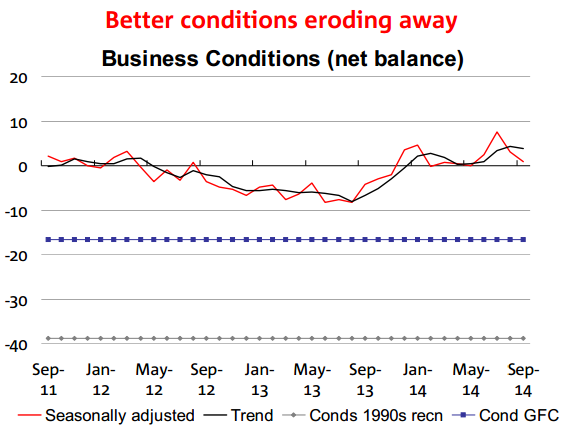

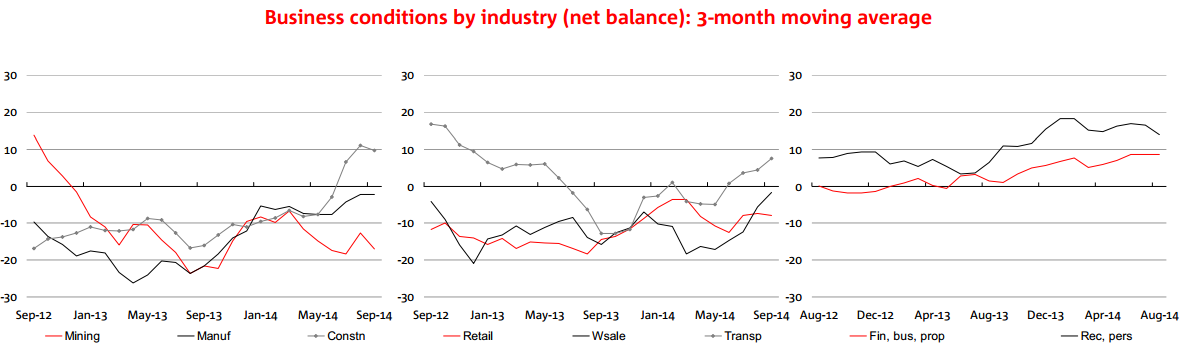

- Business conditions fell again in September bringing the index back to its lowest level in 4 months and confirms our expectation that the (narrowly based) jump in July would be short lived. Most industries recorded a drop in September, although transport & utilities were surprisingly strong (falling oil prices and removal of carbon tax?). Forward orders eased again, implying Q3 domestic demand will remain soft. Capacity utilisation also fell noticeably.

- A drop in profits and employment drove conditions lower, with the latter moving significantly into negative territory – in contrast to some other labour market partials. Forward indicators are soft, but trend conditions in the ‘bellwether’ wholesale industry are a little less weak. Our wholesale leading indicator implies soft underlying conditions and below trend growth in Q3.

- GDP forecasts revised down modestly: 2014/15 2.8% (was 2.9%) and 2015/16 3.2% (was 3.4%). Unemployment rate still to peak at around 6½%. No change likely in cash rate until near the end of 2015.

And the charts:

I’d call the next one “confidence breaking down”:

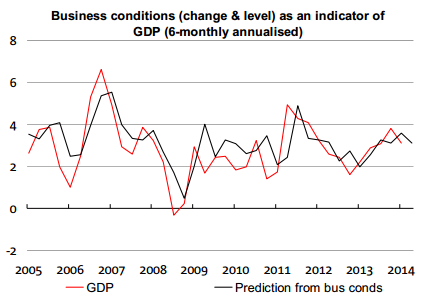

Suggesting weakening GDP ahead:

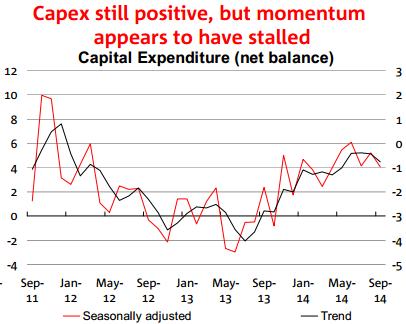

Capex stall:

And by industry:

Looks like the battle between dour consumers and ebullient businesses is being won by the former, as expected. Full report here.

Advertisement