We are more concerned about the outlook for the major Australian banks because we think the EPS upgrade cycle is coming to an end and investors are under-estimating the downside risk to ROEs from the Murray Inquiry. Against this backdrop, elevated trading multiples are hard to justify.

The EPS upgrade cycle is coming to an end

EPS upgrades over the past 2 years were primarily driven by loan loss normalization, home loan standard variable rate re-pricing, lower funding costs and good cost discipline. Better than forecast outcomes now look unlikely. In fact, both revenue and loan loss outcomes missed our estimates in the June quarter. We forecast EPS growth to slow from ~8% in FY14E to just ~5% in FY15E.

Investors are under-estimating the downside risk to ROEs from the Murray Inquiry

We believe that the Financial System Inquiry, led by David Murray, will recommend that capital requirements for the major Australian banks should be revised in order to: (1) enhance financial stability; (2) stay at the forefront of emerging international standards and global best practice; and (3) help to restore competitive neutrality in the mortgage market. We anticipate that the bank regulator (APRA) will then require the major banks to meet more onerous capital requirements over the next few years. This will see ROEs ~1.5%pts lower in the medium-term than they are today.

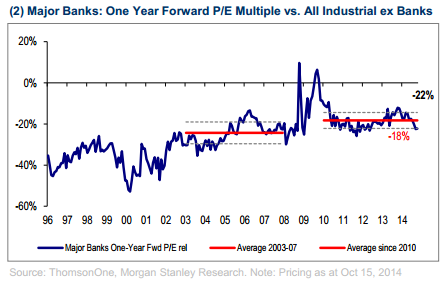

Elevated trading multiples are hard to justify

In our view, the banks’ P/E re-rating has not simply been about the search for yield in a low interest rate environment. It has also reflected a reduction in banks’ risk profile, reduced regulatory uncertainty, renewed confidence in their oligopoly power, higher payout ratios and stronger dividend growth. However, we expect that new capital requirements will lead to dilutive equity issues, lower cross-cycle ROE expectations and concern about sustainable payout ratios. Against this backdrop, P/E and P/BV multiples still look full.

Concerned, but not outright bearish

We expect the major banks to underperform the ASX200. However, there are four reasons why we are not outright bearish: (1) we expect APRA will allow the major banks a transition period to meet new capital requirements; (2) oligopoly power provides the banks with some scope to mitigate the downside risk to EPS and ROE; (3) an Australian economic downturn is not our base case; (4) we do not expect a material Australian house price correction in the near-term while interest rates remain near current levels.

That chart screams financialisation. Certainly it’s hard to imagine things getting any better for banks given globally cheap capital, the search for yield, regulatory sympathy past its apogee and an economy falling away as assets values soar and the resulting macroprudential push…

Other disagree, from the SMH blog:

Deutsche Bank says concerns around higher capital requirements for banks resulting from David Murray’s Financial Services Inquiry have been dramatically overplayed and equity raisings are unlikely.

Analyst James Freeman said a large increase in capital requirements would be difficult to justify and an uptick of around $5 billion to $10 billion for the sector over three to four years looked more realistic.

…Meanwhile, UBS analysts are “warming” to the banks, after being among the most vocally negative in the past on the sector, and expect “a strong” reporting season, which begins October 30 with NAB, followed by ANZ the next day and Westpac Nov 3.

“Revenue should be the highlight,” they write, expecting an aggregate increase of around 5.8 per cent, “the strongest since the post-GFC bounce”.

“Net interest income is the driver, with solid balance sheet growth and modest [net interest margin] compression.”

They are also sanguine on the risks to the Big Four from the Murray Inquiry, saying “the likely impacts are quantifiable”.

I argued two years ago that the banks were a superior proxy for investment in property given their greater liquidity. No longer, though the trip down will be slow as shown by last week’s tumbling bond yields and next year’s rate cuts…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.