Cross posted from Investing in Chinese Stocks.

Two Beijing real estate agencies are on pace to hit 17,000 sales in October, up from the 9109 sales the two combined for in September. Since their market share is 55%, analysts are extrapolating sales citywide hitting 11,500 already, while one insider at another agency thinks sales have already hit 16,000 homes. Average transaction price increased 2.6% in the past week, and another agency that measures bargaining room says the space for haggling has shrunk from over 3% in early October to 2.6% last week. iFeng: 房贷松绑20天作用渐显 京二手房签约量激增

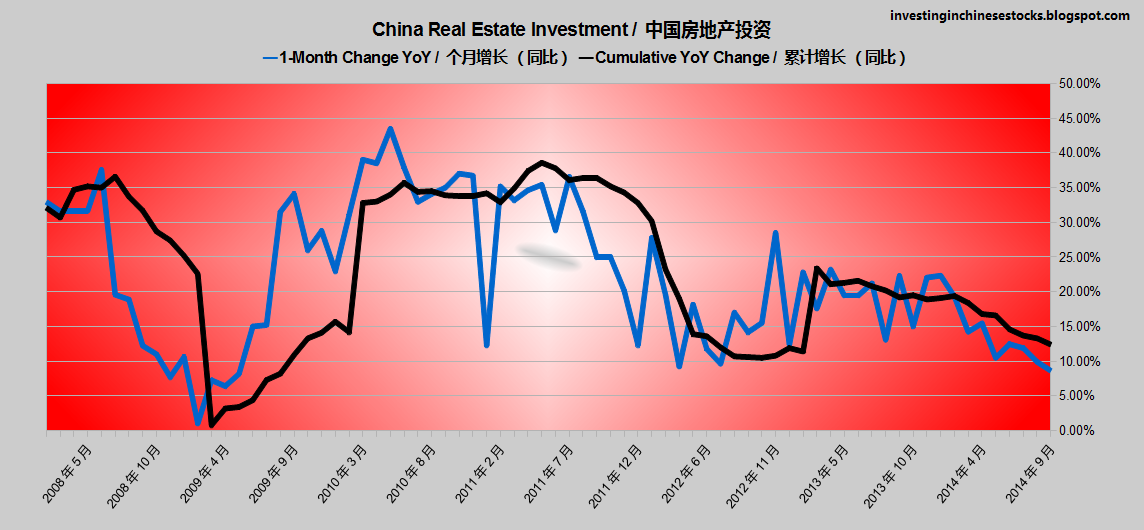

The lift in sales has some work to do. Here’s a chart showing Chinese real estate investment by month compared to the cumulative figure. Absent a trend change, you can see where that cumulative growth line is headed:

Meanwhile, reform moves on with efforts to boost the mortgage backed securities market (MBS). MBS solves two problems for China. One, it needs a way to get credit flowing to home buyers. Two, it needs a large and deep market of RMB bonds in order to interntionalize the yuan.

ECNS: China encourages RMBS to boost housing market

“I think encouraging MBS is the most important part of this policy,” said Jiang Xun, chief economist at a Chinese think tank, referring to the financial instrument’s ability to free up capital for lending and potentially making it easier for home buyers to obtain loans.

Statistics show that the country’s individual home loan balance has reached 10 trillion yuan ($1.6 trillion), a huge potential pool for MBS.

There are worries too, however. Products with short terms and high yields have been prominent in the Chinese market, and MBS, which usually has a maturity of 10 years or longer, may find it hard to lure investors, at least at the early stages.

Until a crisis wipes out short-term high interest loans, then investors will be clamoring for the relative safety of MBS.

SCMP: China calls on banks to boost mortgage securities market

The mainland’s central bank and banking regulator have called on lenders to create a larger mortgage-backed securities market as part of an effort by the central government to revive a flagging real estate sector.

ECNS: MBS unlikely to find favor in China

MBS are underdeveloped in China for a number of reasons. First, there are no State-backed institutions in the country which can provide credit guarantees. Second, it is difficult to fix prices for such products, making them unattractive to both issuers and investors. Looking ahead, it will also be difficult for these securities to gain traction in the local market without further liberalizing interest rates.

If you build it, they will come. There are problems to overcome, but the MBS market would be a great improvement over the opaque trusts and WMPs savers currently buy.