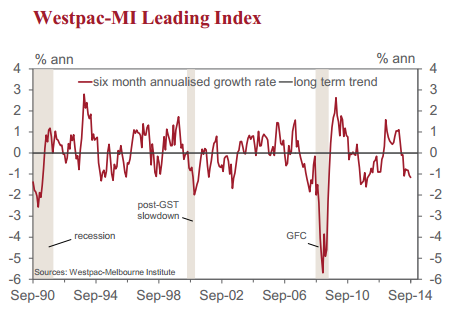

The six month annualised deviation from trend growth rate of the Westpac Melbourne Institute Leading Index which indicates the likely pace of economic growth three to nine months into the future fell from –1.07% in August to –1.16% in September.

This is the eighth consecutive month where the growth rate in the Index has been below trend. That follows 13 consecutive months to February this year when the growth rate was above trend. The index continues to indicate that we can expect growth in the Australian economy to stay below trend in the final quarter of 2014 and into the first half of 2015.

This September print represents the largest negative deviation from trend since November/December 2011 when the RBA had just embarked upon its easing cycle. Recall that over the period November 2011 to August 2013 the RBA cut the overnight cash rate by 225 bp’s. Disappointingly, the deviation from trend in the annualised growth rate has now fallen back to around those levels we experienced at the start of the easing cycle. The Leading Index is indicating that the lift to momentum which was eventually delivered as a result of the rate cuts appears to have dissipated.

That view is consistent with the revised forecasts recently released by the Reserve Bank of Australia in its August Statement on Monetary Policy. While the Bank forecasts using ranges, an analysis of the mid points of these ranges indicates that its forecasts imply that the growth ‘pace’ of the Australian economy is likely to have slowed to 2% (annualised) in the second half of 2014. It has also lowered its forecast (mid-point) for 2015 from 3.25% to a below trend 3%. Growth momentum in the first half of 2015 is forecast to lift from 2% to 3% (still below trend).

Westpac is more optimistic around the growth outlook thanthe Reserve Bank. Partly consistent with the signal from the Leading Index we expect below trend growth in the second half of 2014 but at a 3% annualised pace rather than the 2% implied by the Reserve Bank. In particular we are expecting the pace of consumer spending in the second half to lift from 2% (annualised) in the first half of 2014 to 3% in the second half. That more positive consumer outlook is expected to strengthen further in the first half of 2015, reaching a 3.5% annualised pace. That is consistent with our more upbeat view on the first half of 2015 than implied by the index. We expect that growth momentum in the economy can lift to a trend 3.25% pace in the first half of 2015 , whereas the index is clearly pointing to a below trend performance for the economy in the first half of 2015.

Over the last six months the index’s growth rate has remained at a below trend growth pace. In April, when the Index’s growth rate was 1.09 % below trend, the key drivers were: aggregate monthly hours worked (–0.43 ppt’s); the Westpac –MI Consumer Sentiment Expectations index (–0.36 ppts); the Westpac MI Unemployment Expectations index (–0.14ppts); RBA commodity price index in AUD (–0.26ppts) and dwelling approvals (–0.10 ppt’s). Offsetting those negative effects were US industrial production (0.23ppts). The yield spread and the ASX 200 had minimal impact on the growth rate.

In September the growth rate in the Index has fallen further below trend to –1.16%. The major contributors are now: commodity prices (–0.63ppts); yield spread (–0.24ppts); Westpac – MI Consumer Sentiment Expectations Index (–0.15ppts); average monthly hours worked (–0.32 ppt’s) and the ASX 200 (–0.12 ppt’s). Offsetting those drags on growth are US industrial production (0.15ppts) and the Westpac – MI Unemployment Index (0.15ppts). Dwelling approvals had no impact on the deviation in September after being a consistent drag over previous months.

Overall we can see that commodity prices have intensified their drag on the growth rate; consumers are less nervous around the labour market; and the flattening of the yield curve has become a drag on growth (indicating that monetary policy is too tight given the movement in long term bond rates). The only consistent boost to the growth rate in the Index over the last six months has been US industrial production.

The changed contribution from the yield spread has resulted from a flattening of the yield curve. A fall in long rates which is not matched by lower short rates indicates that the stance of monetary policy may have tightened. Of course the yield curve, in particular the long end of the curve, is capturing both domestic and international influences. Since April the yield curve has flattened by around 80 bp’s.

We do not expect to see the Reserve Bank changing rates until well into 2015. Indeed, the Bank once again confirmed its intentions in its October board minutes for a period of stability in rates. Westpac expects that, with our expectation of a more favourable economic environment than is anticipated by the Reserve Bank, the next move in rates will be a tightening but not until the second half of 2015, with August currently appearing to be the date for the first move.

Nup. China may stabilise but won’t lift much and the pressure on the terms of trade will continue. The consumer is not going to lift either as real incomes fall and the budget is tightened again in December, then macroprudential arrives in the new year and slows the property market. Meanwhile, the capex cliff sheds jobs and the home building boom peaks. Rate cuts next year.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.