Fitch is out with a new report on Australian banks and does the delicate dance of the conflicted ratings agency, pointing to skyrocketing risk while playing it down:

Slower Housing Credit Growth: Fitch Ratings expects a slowing of housing credit growth and, potentially, a stabilisation in household debt levels as wage increases ease and unemployment rises. Risks in the Australian banking system would rise if house prices were to continue their strong growth of 2013 and 2014.

Credit Boosted Price Gains: The availability of credit is one of many factors responsible for the spike in Australian house-price appreciation during 2013 and 2014. Competition for new mortgages has been fierce among banks, helped by record low interest rates; still, credit standards appear to have been broadly maintained and mortgage rates remains the main competitive outlet. Other factors include immigration, better infrastructure in the popular cities, rising foreign investment, and higher borrowing limits for self-managed superannuation funds.

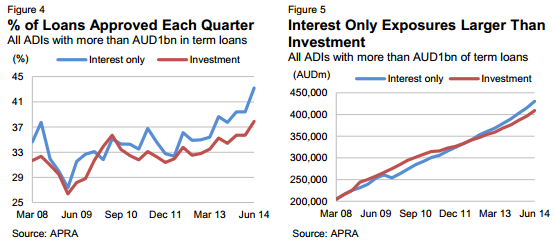

Risk Appetite Growing: Mortgage growth has been strongest in potentially higher-risk segments – investor loans and interest-only loans. The former is probably a result of low interest rates and brings a speculative element to recent house-price appreciation; the latter is in part driven by the growth in investor loans, which benefit from tax-deductible interest payments.

Historical Data Belie Risks: Investment mortgages are likely to experience higher arrears and loss rates than owner-occupier mortgages in a significant downturn; that’s despite bank data that suggest the difference in performance has been negligible since 2008. The relatively benign economic environment over the past 20 years is not a realistic basis upon which to estimate how investor loans would fare in a downturn.

Owner-Occupiers Pursue Interest-Only Loans: The increased use of interest-only loans by owner-occupiers may leave weaker borrowers vulnerable to rising interest rates. Australian banks offset some of the risk by testing loan serviceability at higher interest rates. The factors behind the rise in owner-occupier interest-only loans are less clear and could be numerous as interest payments are not tax deductible, unlike investment loans.

Regulators Increasing Focus: Bank regulators are becoming more vocal on the housing sector risks, and intervention appears increasingly likely. The Reserve Bank of Australia has publicly discussed several macroprudential tools, while the interim report of the financial system inquiry has put forward a number of possible actions to lower risks in the household sector.

Significant Losses Still Remote: Fitch believes significant losses in the mortgage books of Australian banks are unlikely despite the increase in risk during 2013 and 2014. The mortgage portfolios are well seasoned and benefit from relatively conservative underwriting. Losses would be more likely to emerge from commercial loan portfolios in a significant downturn.

Cutting through the guff, interest only and investment loans are Australia’s subprime accident in the making.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.