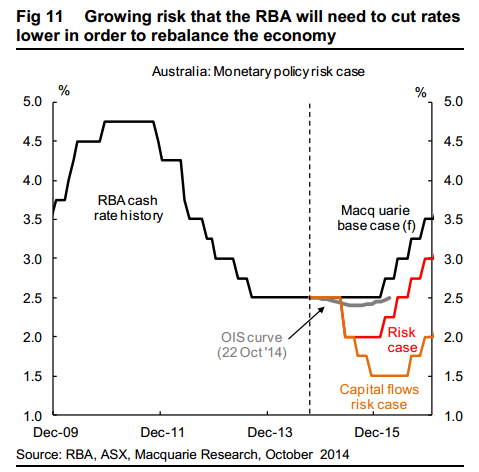

Macquarie Bank still has a base of no rate rises until January 2016 but it has introduced a “risk case” for interest rates based around the adoption of macroprudential tools:

The key hurdles, or catalysts, we think would be necessary for push the RBA into action are:

Non-mining capex intentions for FY16 falling short of the level needed to deliver enough demand to a balance the labour market;

The unemployment rate, after allowing sufficient time to elapse in order to smooth out the rogue July-September outcomes, pushing up towards the 6.5% mark;

Signs that fiscal policy is going to exert additional dampening on the economy directly, and how sentiment is holding up in the lead up to the 2015/16 Budget; and

Whether the disinflation has continued to provide scope for policy easing.

In terms of timing, we think the above catalysts point to a window for any policy move by the RBA opening up over the March-June Board meetings. This would have given sufficient time for initial assessment of the introduction of macroprudential tools, for the FY16 capex estimates and for improved clarity about the likely economic impacts (direct and confidence) from the budget.

With the door opened, if pushed we think the RBA would be likely to cut by at least 50bps. We estimate that this would be the minimum required to push the A$ below the US$0.85 mark. The RBA may need to go further than this, depending on the strength of yield-seeking capital flows.

The addition of €700bn of liquidity from the ECB, the potential for further policy easing by the BoJ and the risk of asset managers front-running in anticipation of portfolio reallocation by the Japanese Government Pension Investment Fund are all potential sources of capital flows that could pose a challenge to A$ weakness. This is one factor that could require the RBA to deliver a greater offsetting interest rate response.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.