From Goldies comes a good summary of the dynamics loose in the oil (and LNG) market as shale output outpaces demand growth, cost-out is taking a hold of the supply curve and OPEC losing its marginal cost producer role in the market:

Oil prices will need to decline to slow US shale

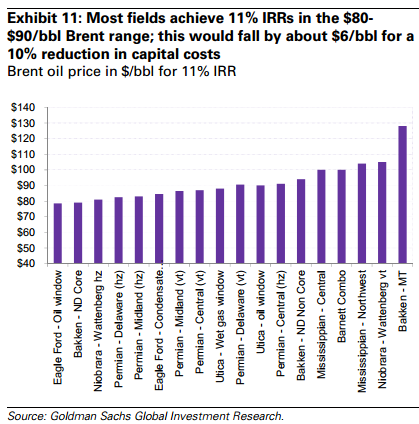

We are lowering our oil price forecast to reflect the required slowdown in US production growth: our WTI crude oil forecast is $75/bbl for 1Q15 and 2H15 (from $90/bbl previously). Given our unchanged WTI-Brent spread forecast of $10/bbl, our Brent forecast is now $85/bbl ($100/bbl previously). Our forecast path reflects our expectation that timespreads will be weakest in 2Q15 when the global oversupply will be largest with Brent prices reaching $80/bbl and WTI prices $70/bbl. In 2016 we expect stabilizing fundamentals with moderate cuts to OPEC production once a slowdown in US production growth is apparent. Our 2016 and long-term forecasts are now $80/bbl WTI, $90/bbl Brent. Uncertainty around the required price to slow down US shale production growth is a key risk to our price forecast.

OPEC loses pricing power, shale shifts to the margin

A tight global oil market had until now required strong OPEC production and US shale production growth. While getting to a point where the market shifted back into surplus was only a matter of time, as US shale oil production grows by Libya’s capacity every year, we now have higher confidence that a structural transition has been reached and that US production growth needs to slow. Accordingly, our forecast also reflects the realization of a loss of pricing power by core-OPEC. Consistent with the economics of the “dominant firm/competitive fringe” market structure and shale production exceeding OPEC spare capacity, pricing dynamics in the oil market have moved away from the dominant firm’s production decision and towards the marginal cost of US shale oil production.

As we’ve seen repeatedly with these commodity market share battles, lower prices than the cost curve suggests are the norm. $70 WTI for much of next year is a reasonable base case.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.