UBS is one of those sensible sell side shops that has been pushing ideas similar to my own post-2011 allocation thoughts for Australian shares in positioning for the falling currency and slowing China:

Correction Restores Some Value

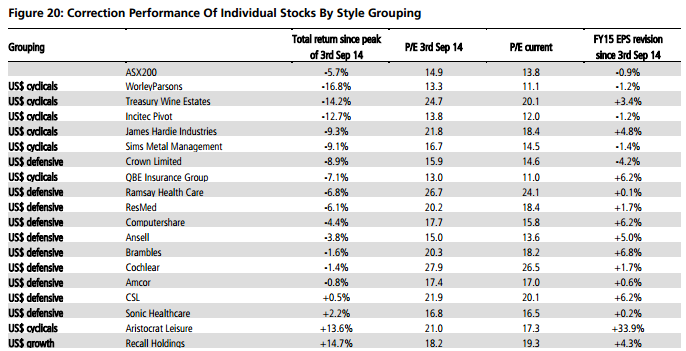

Since our last rebalance in early September the Australian market experienced a 9% correction before bouncing just over 3% from the lows of last week. The correction has restored some value to the market with the market PE (1 year forward) retracing from 14.9x in early September to 13.8x currently. We believe the market P/E can push back into the 14.0 to 14.5x long term average valuation level and we retain our c5600 (ASX200) year-end target.Trimming US$ Defensive Winners – Adding US$ Cyclicals

We see some opportunity in US$ exposed cyclicals given their recent underperformance despite the benefit from a lower A$. We continue to sit with a neutral Mining view and an overweight energy view based on the strong growth in free cash flow we expect from the Energy sector. We have upgraded Banks to neutral from underweight given capital concerns seemingly digested and bond yield risk receding for now.Portfolio Additions & Removals

We added James Hardie Industries and removed Westfield Corporation and Fletcher Building.

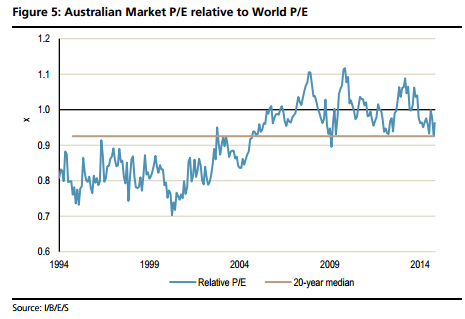

And fair enough. To the charts, and the ASX is going through a post-mining boom malaise that threatens to turn into a global de-rating:

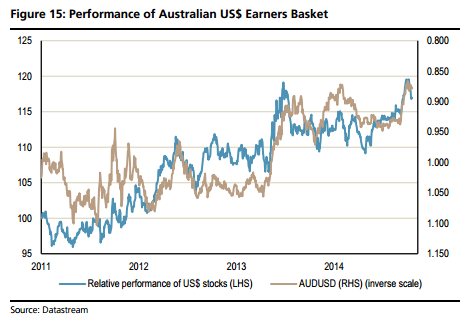

That fits nicely with the MB thesis of a lost decade ahead for the Australian economy. But not for the external-facing industrials:

And here they are:

The great ASX-de-rating is an opportunity like any other.