From Westpac’s excellent Red Book,the bible of consumer attitudes:

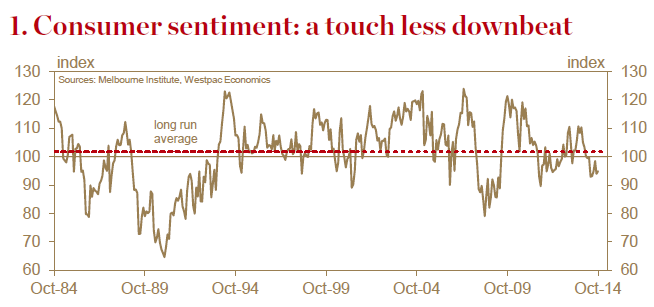

― The Westpac–Melbourne Institute Index of Consumer Sentiment rose by 0.9% from 94.0 in Sep to 94.8 in Oct, a slight improvement but

still leaving the index stuck in a pessimistic range.

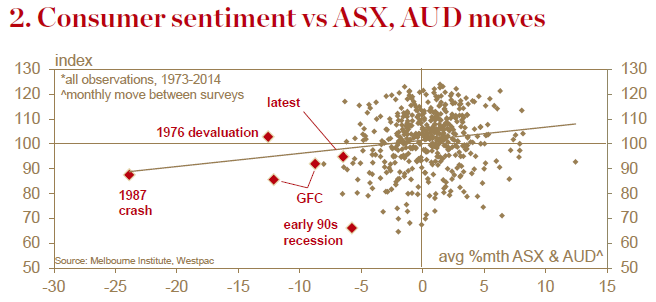

― The Oct result appears to reflect a mix of negatives from financial market developments (the ASX fell 6½% between the Sep and Oct surveys) and positives on ‘Budget and tax’ issues with the Government announcing it was setting aside controversial Budget measures.

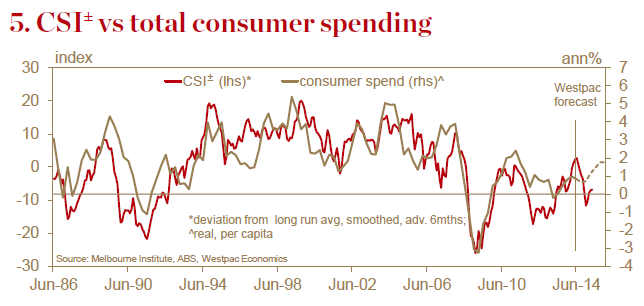

― CSI±, our modified sentiment indicator that we favour as a guide to actual spending, also showed a slight improvement in Oct, rising

1.1%. The index continues to point to per capita spending growth of 0-½%yr, a aggregate pace of 1.5-2%yr once population growth is factored in. That is a slightly slower pace than the 2% annual growth rate seen in H1.

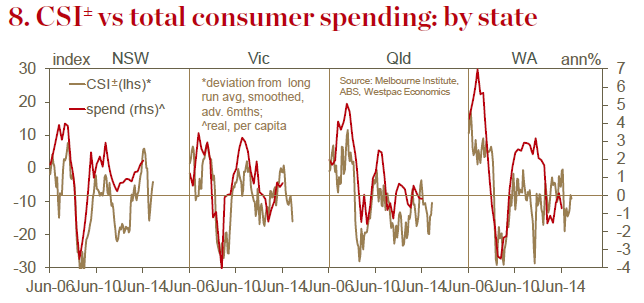

― Latest data on actual spending and surveyed business conditions remain mixed with some signs of cyclical slowing. Divergences across states are also becoming more pronounced with NSW the only state showing solid per capita spending gains.

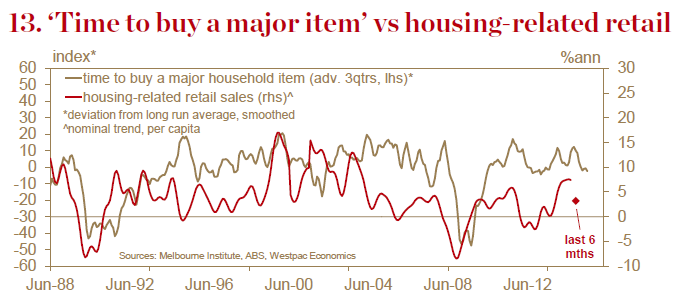

― The sub-index on ‘time to buy a major item’ fell 0.4% to be down 8.4%yr and 2.8% below its long run average. Household goods retail recorded a disappointing 0.8% decline in Aug, the fall also aff ecting relatively strongly growing housingrelated segments.

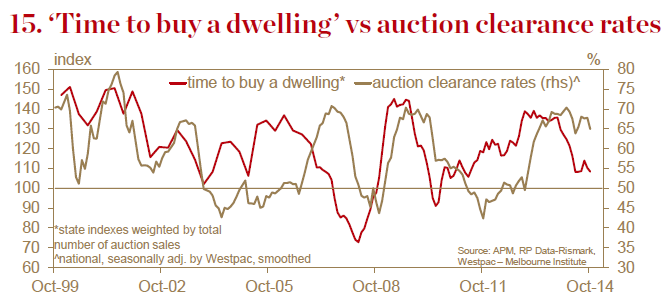

― Confidence around housing remains fragmented. The ‘time to buy a dwelling’ index increased by 2.3% from 111.3 to 113.9. The sub-group detail shows strong gains in Sydney and across potential FHB groups but declines in investor-related segments that may refl ect recent signs from the RBA that it is seeking to cool investor housing activity in some markets.

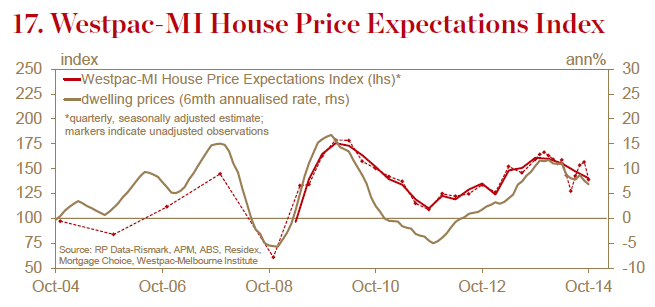

― We are seeing some caution emerge around the outlook for house prices. The Westpac- Melbourne Institute Consumer House Price Expectations Index fell 11.2% in Oct to be 12.8% below its level of a year ago. Expectations are still positive overall but are sharply lower in NSW (–18%) and Vic (–16%).

― Perhaps the most promising aspect of the rvey was around the labour market. The Westpac-Melbourne Institute Unemployment Expectations Index fell 3.9% in Oct, the largest monthly fall in just over a year. That said, the starting point is very weak and previous improvements in 2012 and 2013 were not sustained. Confusion around offi cial ABS employment data may also have distorted the result.

MB take: With housing to slow, income to weigh, unemployment slow to improve and the resource states to deteriorate, Westpac is too bullish on a consumer rebound.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.