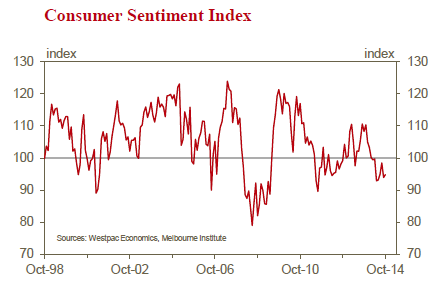

The Westpac Melbourne Institute Index of Consumer Sentiment rose by 0.9% from 94.0 in September to 94.8 in October.

This is the eighth consecutive month that the index has printed below 100, indicating that pessimists have outnumbered optimists for eight consecutive months. That had followed sixteen months where the index had registered above 100 on all but one occasion. The current reading for the index is 1.2% below the average for those eight months indicating that while the index seems to be “stuck” in a pessimistic range there is no sign, at this stage, of ongoing deterioration. Although we are observing this ongoing pessimism the result of this particular month is probably better than might have been expected given the violent moves in global financial markets that might have further unnerved respondents.

Since the survey in September the Australian dollar has fallen by around 6% against the USD and the Australian share market has come down by around 6.5%.

On the other hand households, who reacted negatively to the Commonwealth Government’s May Budget (the index fell by 6.8% in the wake of the budget) may have been encouraged by recent announcements that a number of budget initiatives have been set aside for the time being.

The movements in the components of the index seem to confirm these key factors. Possibly in response to more comfort around the budget initiatives we saw improvements in respondents’ assessments of their own finances. The component “family finances vs a year ago” increased by 4.4% while “family finances next 12 months” improved by 1.2%. Global developments have clearly unnerved respondents’ attitudes to the short term economic outlook. “Economic conditions over the next 12 months” fell by 5.2% while the five year economic outlook actually improved by 5.5%.

The component “whether now is a good time to buy a major household item” fell by 0.4%. This component is down by 8.4% compared to a year ago; the family finance components are down by an average of 5.6% whereas the economic outlook components are down by an average of 21% compared to a year ago.

There was better news around the labour market. The Westpac Melbourne Institute Unemployment Expectations Index fell by 3.9%. A fall in this index indicates that respondents are feeling more comfortable with respect to job security or employment prospects. This is the lowest print for this index since November 2013; the largest fall since September 2013 and the index is now 9.6% below the recent high in March this year.

Of course we cannot be sure whether the recent volatility in the official employment report has been impacting this promising development in the index.

Confidence around housing remains fragmented. The index “whether now is a good time to purchase a dwelling” increased by 2.3% from 111.3 to 113.9. However it remains 12.4% below its level of a year ago and 18.5% below its level two years ago.

The change in the index over the last year has varied markedly across states. In NSW the index has been steady whereas it has fallen by 27% in Victoria and 17% in Queensland.

We are seeing some caution emerge around the outlook for house prices. The Westpac Melbourne Institute House Price Expectations Index fell by 11.2% in October to now be 12.8% below its level of a year ago. The proportion of respondents expecting house prices to rise fell from 66% to 53.8%.

The Reserve Bank Board next meets on November 4. In the Governor’s statement following the October board meeting he restated his position that we can expect a period of stability for interest rates. Westpac remains comfortable with its forecast that the next move in the overnight cash rate will be an increase of 0.25% in August next year. This is in sharp contrast with the financial markets that are not looking for any significant move in rates by the end of 2016. A slowdown in global growth and associated weakness in global inflation has been driving market pricing. We expect global growth to recover in 2015 as the US gathers momentum and China continues to introduce more stimulatory policy measures.

Increasing “targeted” stimulus measures, Bill, with a view to supporting a structural adjustment that implicitly slows growth and even more so commodity demand.

Also, it looks like the RBA house price jawboning is starting to get through.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.