The Wall Street Journal has a report from the Conference Board on a slowing China:

China’s growth will slow sharply during the coming decade to 3.9% as its productivity nose dives and the country’s leaders fail to push through tough measures to remake the economy, according to a report expected to come out Monday.

…Foreign companies should realize that China is in “a long, slow fall in economic growth,” the report said. “The competitive game has changed from one of investment-driven expansion to one of fighting for market share.”

The Conference Board forecasts that China’s annual growth will slow to an average of 5.5% between 2015 and 2019, compared with last year’s 7.7%. It will downshift further to an average of 3.9% between 2020 and 2025, according to the report.

…The New York-based Conference Board argues that productivity in China is declining, in part because investments in infrastructure and real estate don’t have the payoff they once did. Meanwhile, government and Communist Party officials who don’t give market forces a large-enough role are stifling innovation.

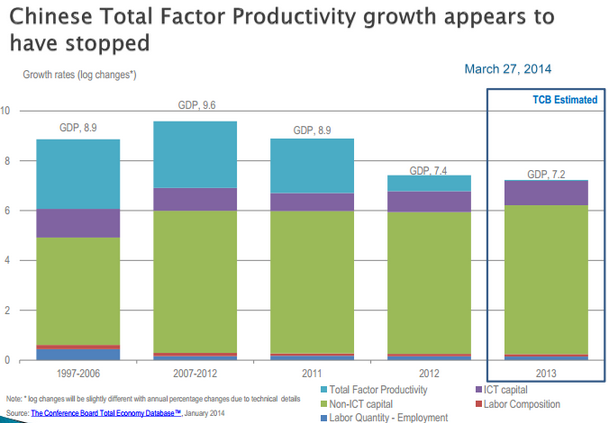

Fair enough. Here’s the problem chart:

Zero multi-factor productivity growth in 2013.

But it is a little more complex. If the Conference Board is right and China does not reform then it will grow at better rates for longer as credit growth and investment are propped up at the expense of productivity. That will end in tears at some point as growth crashes into a debt crisis.

Thus the Conference Board forecast of a growth glide slope is actually the successful reform path in which credit and malinvestment are reined in and productivity gains boost income and consumption in the household sector, the so-called rebalancing championed by Michael Pettis.

It’ll be no small feat but I draw the opposite conclusion to the Conference Board, that China’s central authorities have the motivation and wherewithal to do it. If it were a democracy it’d be stuffed. And yes, ironies abound!

Here is more, too, from yesterday’s Larry Summers piece predicting even lower growth rates:

We are trying to reverse the default assumptions often made in forecasting GDP, which is that, in the absence of any reason to think otherwise, the current growth rate persists. In this view what has to be justified with argumentation is why the growth rate would decelerate. However, this mode of forecasting or projection or even formulation of scenarios is counterfactual to the single most robust fact about growth rates, which is strong reversion to the mean. Our argument is that the default prediction/projection/forecast should be that a country’s growth rate will be subject to regression to the mean. What has to be justified with argumentation is why the growth rate would persist at rates higher (or lower) than the world mean growth rate.

…knowing the current growth rate only modestly improves the prediction of future growth rates over just guessing it will be the (future realized) world average. The R-squared of decade-ahead predictions of decade growth varies from 0.056 (for the most recent decade) to 0.13. Past growth is just not that informative about future growth and its predictive ability is generally even lower over longer horizons…

There is some consensus that China will not maintain 9 to 10 percent growth rates, but even the view that China’s growth will slow to something like 7 percent assumes substantial persistence. The predicted growth over the next two decades using regressions is 3.9 percent (with a coefficient on past growth of 0.24), and the regression standard error of estimation is 1.6 percent, so a continuation of even 7 percent is two standard deviations in the tail, and a continuation of a growth rate of 9 percent is three standard deviations.

…Among 22 countries in which episodes of large democratic transition coincided with above-average growth, all but one (Korea in 1987 with an acceleration of only 0.22 percent) experienced a growth deceleration. The combination of high initial growth and democratic transition seems to make some deceleration all but inevitable. The magnitude of the decelerations was very large: The median deceleration across the 22 countries was 2.99 percent and the average deceleration was 3.53 percent.

…If China and India continued at their current rate, they would reach over $66 trillion and hence just mechanically the annual growth rate of world GDP is 3.5 percent and then 4.45 percent in the next two decades (accelerating just because India and China mechanically have a larger share of the total). Conversely, with regression to the mean scenarios for China and India, the global growth rate is 2.48 percent and 2.27 percent.

Of course this mechanical calculation underestimates the role of China and India as growth engines by assuming that other country growth rates are not raised by faster growth in the giants. To the extent there are positive linkages, then this mechanical calculation underestimates (perhaps substantially) the impact on global growth of regression to the mean.

…We suggest several implications of these conclusions. First, there will be a strong tendency to assume that, if growth slows substantially in China or India, it will represent an important policy failure. This is not right. Regression to the mean in a decade or so is the rule, not the exception. What would require much more explanation would be continued rapid growth, which would be very much outside the general run of experience. Second, those making global projections should allow a very wide confidence interval with respect to growth for countries whose current growth rates are far from the mean. Given the sensitivity of commodity demands in particular to growth rates in Asia, this suggests substantial uncertainty about the medium-term path of commodity prices. In the same way, forecasts of global energy use and climate change impacts should also recognize the possibility of discontinuities in Asia. Third, much geopolitical analysis has focused on the implications of a rising China, and certainly Chinese international relations theorists have extensively studied past rising powers. Contingency planning should also embrace scenarios in which Chinese growth slows dramatically, presumably bringing with it a range of domestic and international political implications.

Nah, sell ’em dirt! Full paper here.