Fresh from Westpac’s Huy McKay (who really should be commended for the creation of this survey):

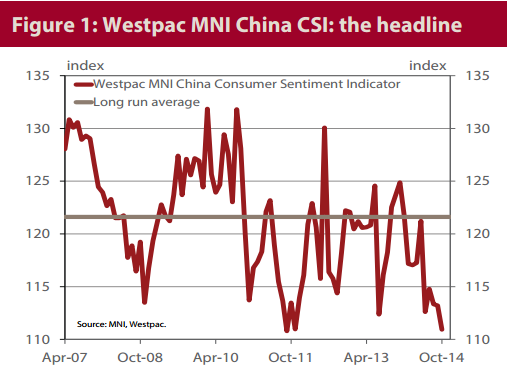

The Westpac MNI China Consumer Sentiment Indicator, hereafter the Westpac MNI China CSI, fell markedly in October from an already weak level, printing 110.9 versus 113.2 in September, a –2.0% change over the month and –9.5% over the year. The October outcome is 8.8% below the long run average. The survey indicates that the anxieties gnawing away at the Chinese consumer through most of this year remain very much in evidence as Q4 opens. Indeed, those anxieties arguably now run even deeper.

• We have noted repeatedly that households have been considerably less impressed with the state of the economy than have been manufacturing firms. Taking into account the weak tone of the general data flow over the last quarter or so, with hindsight we can safely claim that the scepticism of the consumer was closer to the mark.

• Each of the five components that go into the calculation of the Westpac MNI China CSI declined from the previous month. Current and expected family finances moved lower, by 1% and 2.5% respectively, while ‘time to buy a major household item’ declined by 2%. ‘Business conditions one year ahead’ and ‘five years ahead’, fell by 2.3% and 2.2% respectively. Current business conditions (not a part of the headline composite, but tightly correlated with official industrial production data) also declined, but by somewhat less than the forward lookingmeasures. A month ago it seemed as though consumers did not expect the economy to weaken anew from its already underwhelming state. This survey questions that assumption.

• Back in June the employment indicator was sitting at levels that have been associated with policy easing in previous cycles. Four consecutive declines from those already depressed levels alongside weak official data provide a watertight case to strengthen policy support for growth. Westpac applauds the administration’s plan to proceed with the publication of an internationally comparable unemployment rate. To date, the employment indicator from this survey has been the only reliable measure of labour market trends. We look forward to benchmarking to a credible official baseline before too long.

• The consumers’ attitude towards real estate has been evolving in step with the market correction. Expectations for house prices fell for the fourth consecutive month in October; the share of respondents reporting it was a ‘good time to buy a house’ fell further, while the proportion of consumers nominating a housing purchase as their primary motivationfor saving fell. 15.6% of consumers now nominate domestic real estate as the ‘wisest place for their savings’, down from 22.1% in June. The reasoning behind the good/bad ‘time to buy a house’ questions continue to imply that a durable upturn in the housing market will require an improvement in overall conditions, in addition to the easing of sectoral controls. The fact that the Sept 30 policy package was announced prior to this survey being undertaken underscores the point.

• Overall, this survey does not augur particularly well for the November 11 ‘Single’s Day’ online shopping sales, which is China’s version of the US’ Black Friday.

It doesn’t bode well for Westpac’s forecast for a rebound in Chinese property, the iron ore price, the Australian dollar and interest rates, either.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.