The Reserve Bank Board meets next week on November 4. November has been a remarkably popular month for the Bank to move rates. In the first six years of the Governor’s tenure every November proved to be a moving month (2006-2011). In 2012 the Bank was certainly ‘in play’ with moves occurring in both October and December while, arguably, the Bank was also ‘in play’ in November last year.

Next week will be the first November of the Governor’s long tenure that there is no chance of a November move.

In fact it seems highly unlikely that there will be any major surprises. In his statement the governor is likely to maintain the two key assertions which have been used all year: an overvalued currency; and the expectation that rates will remain unchanged for some period.

Specifically, we expect the statement to repeat key phrases: “the exchange rate… remains high by historical standards”; and “the most prudent course is likely to be a period of stability in interest rates”.

We were surprised that the October statement did not include something along the lines of the ‘warning’ contained in the minutes to the September Board meeting, that “policy also needed to be cognisant of the risks to future growth that could accompany a large further build-up in asset prices, particularly if that was associated with an increase in leverage”.

Even the minutes to the October Board meeting were not as strident around the Bank’s concerns about asset prices and leverage. With house price inflation slowing from its 2013 H2 pace, it appears the Bank might be easing up on its concerns around the property market. There is still likely to be some RBA/APRA package of initiatives announced before year’s end but, given the authorities do not appear to be inclined towards ‘heavy handed’ actions and the flexibility of Australia’s financial system, particularly around an active non-bank sector, it seems unlikely that these moves will have a marked effect on the availability of credit overall.

The second important RBA missive next week will be the Statement on Monetary Policy (SoMP). Of considerable interest will be its revised GDP growth and inflation forecasts. As discussed in last week’s note we do not expect any significant changes in either of these. Supporting an upgrade to the growth forecasts will be a new set of AUD forecasts (given the around 5% fall in the AUD since the last SoMP in August).

However confidence measures and the terms of trade have also fallen since August and the global outlook appears more uncertain. That is likely to see the RBA’s growth forecasts stay around the same levels (GDP growth of 2.5% annualised, in 2014 H2; and 3% in 2015).

A weak global growth environment is certainly weighing on markets.

We are decidedly nervous about the fact that markets are predicting AUD rates to remain unchanged over the course of both 2015 and 2016.

In contrast Westpac is expecting 50bps of hikes in the latter half of 2015 and a further 100bps in 2016.

Back in March we were quite out of step with the Economics community. We did not expect the RBA to begin hiking until August 2015 whereas 60% of forecasters expected rate hikes by the March quarter and 15% expected rate cuts.

All those rate hawks have been forced to revise their views. The latest survey indicates that 85% of economics forecasters are still predicting higher rates by end 2015 (with 50% expecting hikes to begin in the June quarter – but expect that proportion to dwindle by year’s end).

Only 15% (four forecasters) are pushing the market’s line.

Unusually we find ourselves buried in the economists’ consensus. Why are we comfortable with a view that is so at odds with the market?

We expect that the economists’ consensus is giving most weight to house prices and leverage. We are focussing on world growth and Australia’s own growth dynamics.

We think the market is being too pessimistic about the world economy and Australia’s likely growth profile in 2015 and 2016.

On the world economy we are expecting growth to lift from 2.9% in 2014 to 3.7% in 2015 and 4.5% in 2016.

That 2016 outlook will hold the key. In particular, it requires US growth to lift from 2.5% in 2015 (long run potential) to 3.25% in 2016 (well above long run potential). With the strongest bilateral links between the major economic blocs being from US to China we expect a strong US economy to boost China’s exports pushing a 1ppt contribution to China’s growth from net exports. That will lift China’s economic performance in 2016 to 8% growth.

We are not expecting the Fed to start raising rates until September next year with two hikes in 2015. That is in line with market pricing (unlike

FOMC ‘dot’ indicators of 150bps in 2015) but we expect the Fed to be more active in 2016, moving rates up by a further 150bps compared to current market expectations of ‘only’ 100bps. That is primarily based around a more upbeat view on the US economy in 2016 than we suspect is the view of the market.

With the Fed pushing rates up by a total of 200bps by end 2016 we struggle to see the market’s rationale that rates will remain on hold in

Australia (note that the long term average margin between Australian and US rates is 150bps).

The market must also be more pessimistic around the outlook for Australia’s growth.

There are certain ‘knowns’ for the Australian economy:

1) the mining sector will continue to add around 1ppt to GDP growth (after adjusting the investment downturn for the lift in net exports).

2) Australian businesses are cautious and are unlikely to lift employment, wages and investment until they see a sustained lift in demand. Past performance is not a reliable indicator of future performance. The forecasts given above are predictive in character. Whilst every effort has been taken to ensure that the assumptions on which the forecasts are based are reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The results ultimately achieved may differ substantially from these forecasts.

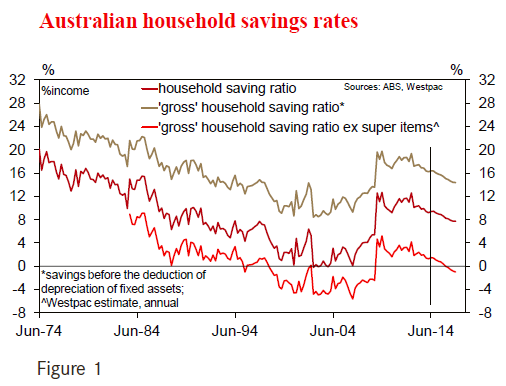

3) The balance sheet of Australia’s household sector has strengthened significantly and there are signs that the household sector is gradually lowering its savings rate.

Figure 1 shows three measures of Australia’s household savings rate: the official rate; a ‘gross’ rate before the deduction of an imputed charge for depreciation; and a ‘gross’ rate excluding super contributions and earnings. Note how the 10 years before the GFC, when house prices were appreciating solidly, Australians ran a negative ‘gross’ ex super savings rate. Since the GFC this savings rate has been positive. Reflecting this lift in savings household balance sheets have been bolstered by sizeable increases in liquid assets – term deposits; loan offset accounts; and on line savings accounts. In addition, Australian households have benefitted from sizeable increases in overall wealth with the lift in property and equity prices complementing the boost in superannuation.

We are expecting to see further evidence of a gradual moderation in the savings rate (partly reflecting rising house prices) that will lift spending growth and signal to business that sustained improvements in demand are underway.

In turn that will encourage businesses to further lift employment; investment and wages growth.

That self- sustaining momentum can be “short circuited” by shocks.

The most obvious “candidates” are an external shock or a policy shock (potentially associated with a financial crisis in either Europe or China).

The sharp drags on confidence following the European financial crisis in 2011 or this year’s Commonwealth Budget are clear testimony to these risks.

Clearly, markets are much more sceptical about the prospects for a sustained lift in demand than Westpac – developments over the next 6 months will tell the tale.

I don’t buy it. Global growth will improve next year, sure, but not that much. And the mix will also change unfavourably for Australia with the US leading and China dragging. The corollary is that falls in the terms of trade will continue, incomes will remain under pressure, investment will continue to fall, as well as only partially rebalance and the labour market remain weak.

Our Bill also obviously underestimates macroprudential which, just a few weeks ago he argued was not coming. It is coming and it will make a difference, in my view quite a bit of difference, to a very unbalanced housing market. Prices will slow, possibly a lot, and begin to fall in some cities (I’m looking at you, Perth!).

Households will not be running down savings in that environment. Rates will go lower with the dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.