Equity and currency markets are celebrating the overnight release of US Q3 GDP, up a half percent as I write with the US dollar breaking out. From the BEA:

Real gross domestic product — the value of the production of goods and services in the United States, adjusted for price changes — increased at an annual rate of 3.5 percent in the third quarter of 2014, according to the “advance” estimate released by the Bureau of Economic Analysis. In the second quarter, real GDP increased 4.6 percent.

…The increase in real GDP in the third quarter primarily reflected positive contributions from personal consumption expenditures (PCE), exports, nonresidential fixed investment, federal government spending, and state and local government spending that were partly offset by a negative contribution from private inventory investment. Imports, which are a subtraction in the calculation of GDP, decreased.

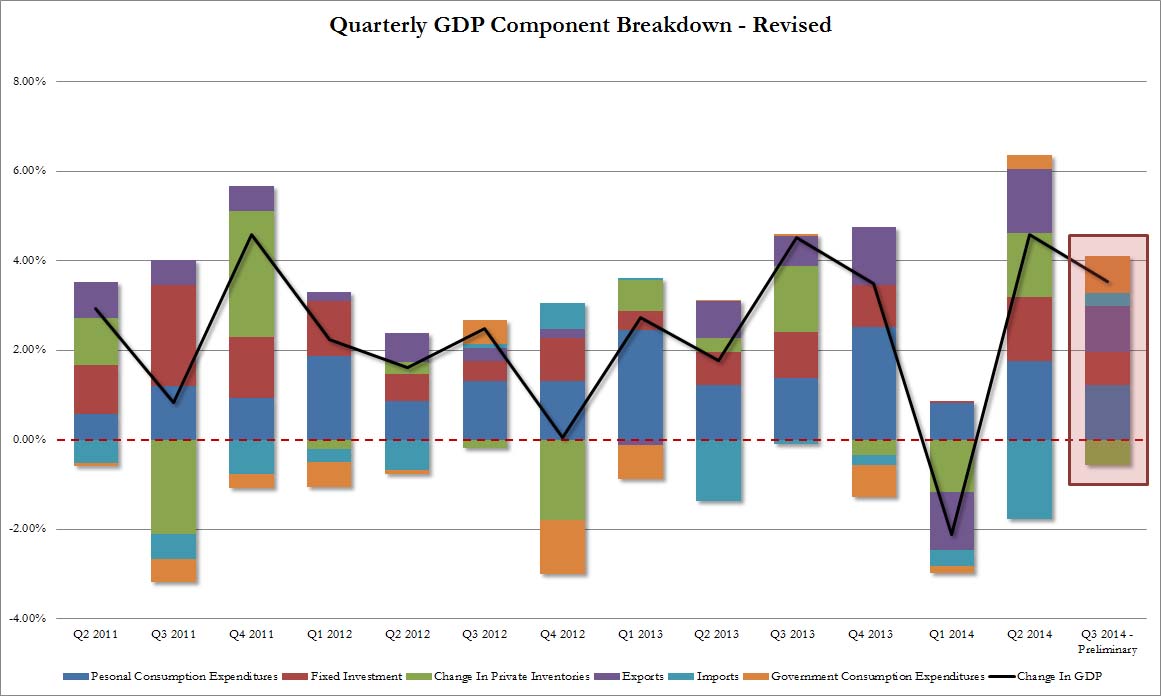

Here’s a chart of the mix:

It’s a good figure and if you remove the distortions around winter you can see the rising trend. Four points to make:

- first, note the lack of negatives for the quarter. This is quite unusual and unlikely to be repeated. Usually one or more of the inputs comes in more negative as many counter-balance each other;

- second, the government expenditure contribution is very high relative to the recent past;

- third, private expenditure and investment is quite low relative to the recent past;

- this mix gave rise to an unusually large contribution from net exports.

These are all reasons to wonder if this figure is as firm as it appears and helps explain why the bond market opted out of the party, further flattening with a firm bid across the curve.

Don’t get me wrong, I expect US growth to get closer to 3% this year but the grind upwards most likely remains.

{kind=link}