From The Economist:

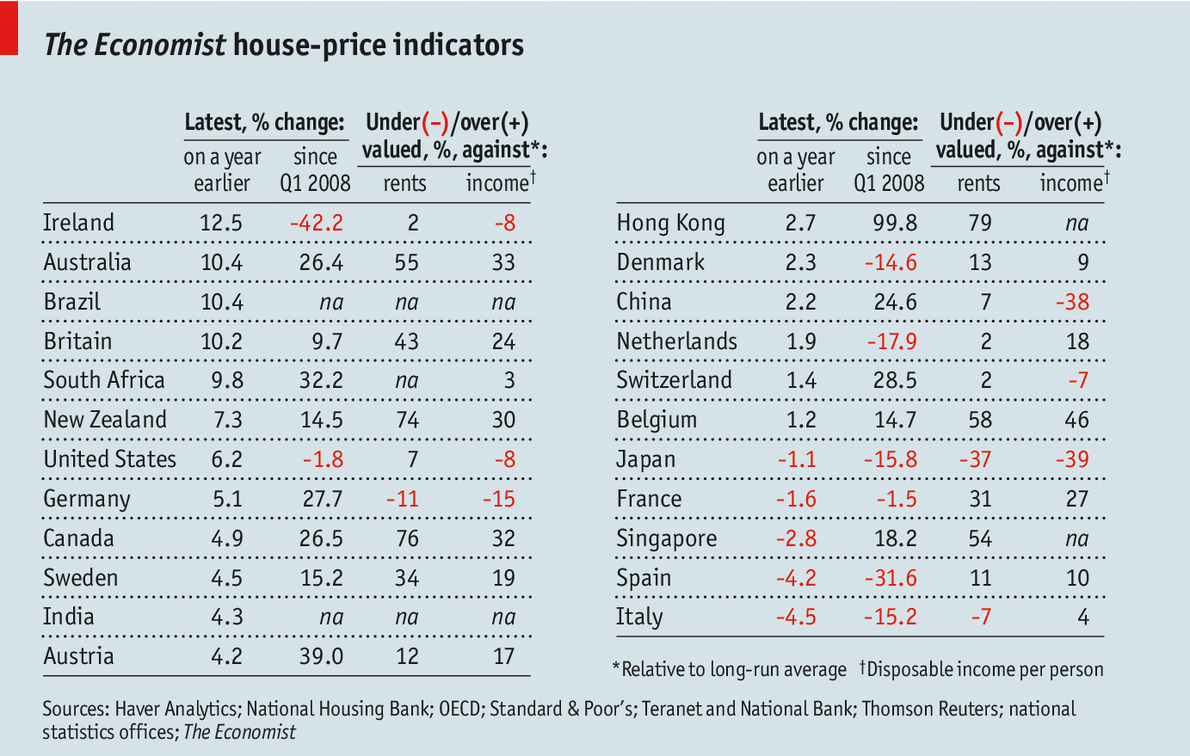

Since some recovery was bound to occur after the housing slump, how worrying are the renewed signs of exuberance? To assess whether house prices are at sustainable levels, we use two yardsticks. One is affordability, measured by the ratio of prices to income per person after tax. The other is the case for investing in housing, based on the ratio of house prices to rents, much as stockmarket investors look at the ratio of equity prices to earnings. If these gauges are higher than their historical averages then property is deemed overvalued; if they are lower, it is undervalued.

Based on an average of these measures, houses are at least 25% overvalued in nine countries. Judged by rents, the most glaring examples are in Hong Kong, Canada and New Zealand. The overshoot in these economies and others bears an unhappy resemblance to that prevailing in America at the height of its boom before the crisis.

55% on rents. 30% on incomes.