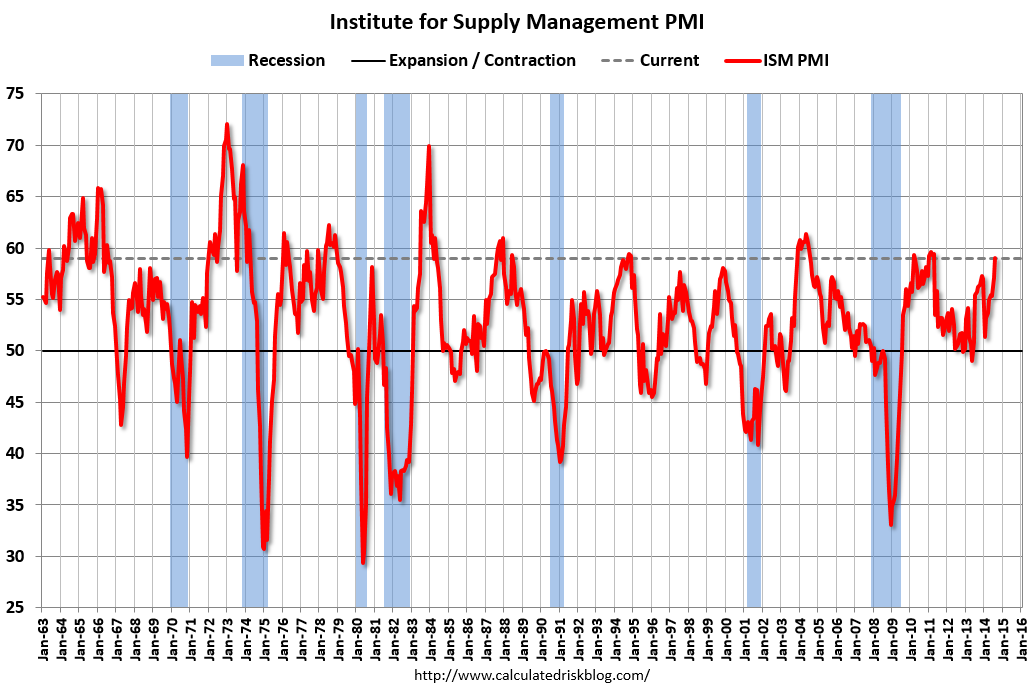

More Goldilocks US data overnight. The ISM manufacturing is booming (charts from Calculated Risk):

Economic activity in the manufacturing sector expanded in August for the 15th consecutive month, and the overall economy grew for the 63rd consecutive month, say the nation’s supply executives in the latest Manufacturing ISM® Report On Business®. “The August PMI® registered 59 percent, an increase of 1.9 percentage points from July’s reading of 57.1 percent, indicating continued expansion in manufacturing. This month’s PMI® reflects the highest reading since March 2011 when the index registered 59.1 percent. The New Orders Index registered 66.7 percent, an increase of 3.3 percentage points from the 63.4 percent reading in July, indicating growth in new orders for the 15th consecutive month. The Production Index registered 64.5 percent, 3.3 percentage points above the July reading of 61.2 percent. The Employment Index grew for the 14th consecutive month, registering 58.1 percent, a slight decrease of 0.1 percentage point below the July reading of 58.2 percent.

That is thumping along.

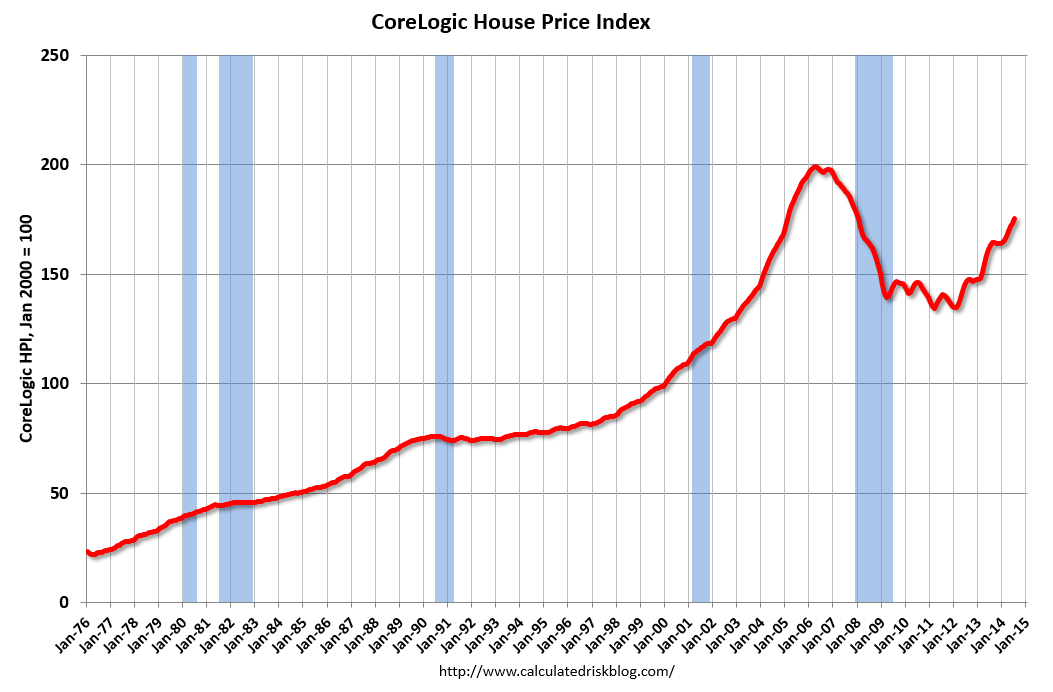

Housing, on the other hand, continues to track towards a soft landing. From Core Logic:

Home prices nationwide, including distressed sales, increased 7.4 percent in July 2014 compared to July 2013. This change represents 29 months of consecutive year-over-year increases in home prices nationally. On a month-over-month basis, home prices nationwide, including distressed sales, increased 1.2 percent in July 2014 compared to June 2014.

…Excluding distressed sales, home prices nationally increased 6.8 percent in July 2014 compared to July 2013 and 1.1 percent month over month compared to June 2014.

Advertisement

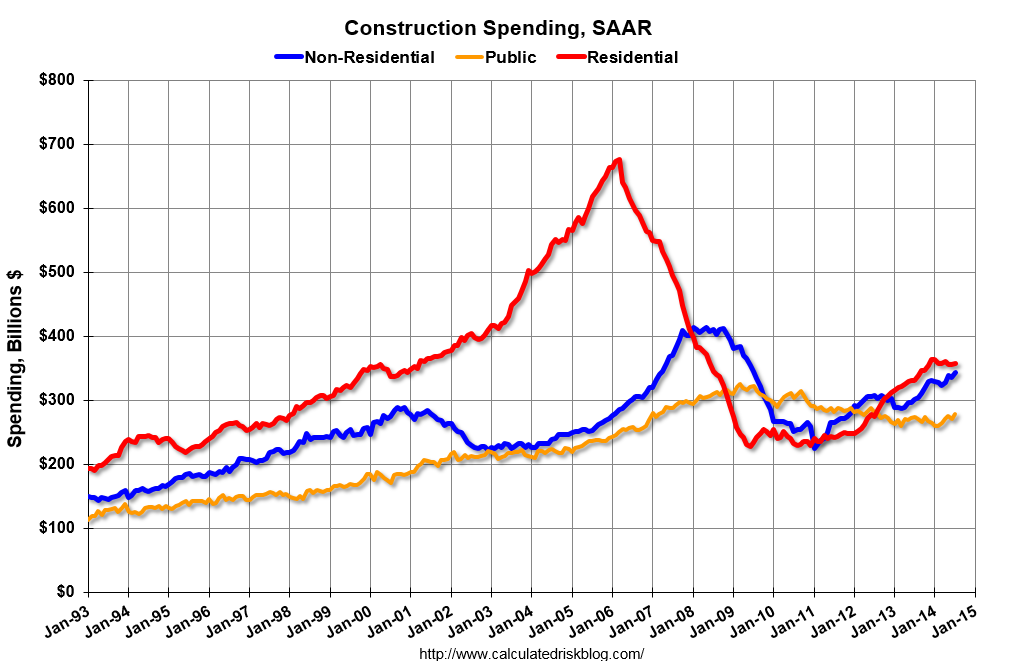

The index chart looks bubbly but price rises are easing and will be half today’s in year-on-year terms within six months. Meanwhile, construction spending rose but looks soft:

The U.S. Census Bureau of the Department of Commerce announced today that construction spending during July 2014 was estimated at a seasonally adjusted annual rate of $981.3 billion, 1.8 percent above the revised June estimate of $963.7 billion. The July figure is 8.2 percent above the July 2013 estimate of $906.6 billion.

Note that residential construction is tapering.

Advertisement

A great combination of rising business construction, booming manufacturing, and moderating house prices. Enough to get the equities bulls mulling an historic expansion. From BofAML:

Business cycles don’t die of old age, they die of overheating. Debt dynamics, particularly in the US, paint the picture of a more prudent household sector and well-managed corporate sector, both of which remain far from the heights of leverage typically associated with risks to business cycle expansions. Moreover, volatility in the economy has trended lower over time, owing in part to technological advances that have helped companies remain nimble when sudden changes in aggregate demand occur, and in part to a rising share of companies that carry no inventory.

The current expansion is more than five years old, and with little evidence of global synchronicity, there are no signs as yet that the global economy is overheating. The current US expansion has already lasted longer than the average expansion in the post-WWII period, but the factors we monitor and have discussed here lead us to conclude that it isn’t unreasonable to expect that this expansion could be the longest on record. In a scenario where the cycle does extend for several more years, earnings could grow modestly as well. The US Equity Strategy team notes that EPS growth of 6% per year from 2015-2020 would drive S&P500 earnings to near $170. A 17x multiple would translate into a peak level for the S&P500 near 3000 under this scenario.

Of course, no one can predict unforeseen shocks to the economy – be it fiscal or monetary policy missteps domestically, geopolitical events abroad, or even major natural disasters. But our title, “2020 Vision”, is our tongue-in-cheek way to desribe the idea that the current US expansion could prove to be the longest ever and perhaps last until 2020.

There are a number of ways the current expansion could get derailed. Europe and China are already slowing and near recession in some parts. Japan is highly dependent on the success of policy. US reforms on key issues like the budget, taxes and entitlements, and immigration seem a long way off and are likely to cause much angst in the coming years. And after a prolonged period of unprecedented monetary policy accommodation, we are on the cusp of removal of that accommodation – also in an unprecedented way. So by no means can we say that six or seven more years of expansion are an obvious outcome. But, all else being equal, the metrics we analyzed in this note are unlikely to be the root cause if this expansion were to be cut short.

That’s mature business cycle ecstasy if I’ve ever seen it! The US already has bubbles in its debt and equity markets. They’ll likely get bigger before bursting but it’s not going to take until 2020!

Markets reacted strongly to the data. The S&P was stable but bonds reversed aggressively at the long end, with yields up 3% on the 30 year. The short end was weak but less so. The US dollar powered to a new high for the move and the Aussie was hit below 93 cents. Gold was spanked 1.5% and oil was down 3%.

Advertisement

All moves consistent with US rate rises. I remain unchanged in my view that they will not come until Q2 next year. Why disrupt this dream run?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.