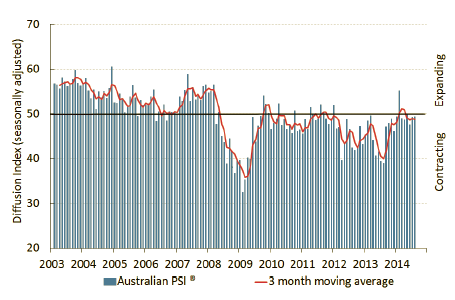

The seasonally adjusted Australian Industry Group Australian Performance of Services Index (Australian PSI®) was almost unchanged in August, at 49.4 points (49.3 points in July). This suggests conditions have been broadly stable within the services industries over the past two months (index readings below 50 points indicate contraction, with the distance from 50 points indicative of the strength of the contraction). The three-month moving average for the Australian PSI® was marginally lower this month, at 48.8 points.

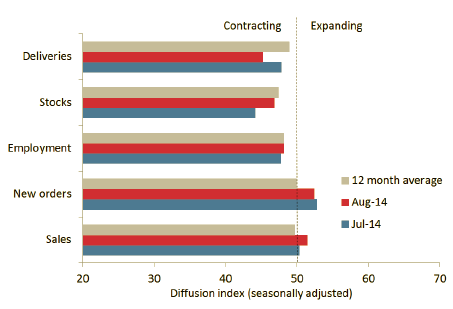

Encouragingly, both the sales and new orders sub-indexes in the Australian PSI® remained above 50 points in August, indicating a mild expansion. In contrast, the supplier deliveries, stocks and employment sub-indexes all continued to contract (below 50 points) this month, as service businesses remain very cautious about the economic outlook and continue to rein in their input costs.

Respondents to the Australian PSI® continued to raise concerns about the weak local economy and uncertainties surrounding various Federal Budget proposals. Consumer oriented services sub-sectors such as health and community services (52.7 points), finance and insurance (which includes superannuation) (60.6 points), and accommodation, cafes and restaurants (55.9 points) continued to expand this month (three month moving averages) and retail trade stabilised. But the downturn in mining related construction and ongoing weakness in the manufacturing industry have reduced the flow of work available to the more business-oriented services sub-sectors.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.