More action from the PBOC this afternoon with the Chinese central bank cutting the 14-day repurchase rate by 20 basis points to 3.5 per cent. This is more easing though again questionable as stimulus. From ANZ via the SMH blog:

We think the market should consider this as an important move as China has relied more on managing short-term market interest rates to push forward interest rate liberalisation.

We think the market should consider this as an important move as China has relied more on managing short-term market interest rates to push forward interest rate liberalisation.- In our view, this is another policy easing effort following yesterday’s liquidity injection via Standing Lending Facility (SLF). However, none of the commercial banks or the central bank confirmed the SLF so far. The non-transparent monetary policy implementation will increase the market volatility. In addition, the banks who receive the SLF will have the ‘first mover advantage’ and this ‘information asymmetry’ will bring about more market uncertainties.

- The recent moves will help improve the growth momentum somewhat but will unlikely turnaround the growth trajectory without further easing policies. Notably, commercial banks remain cautious on credit extension amid economic slowdown and property softness.

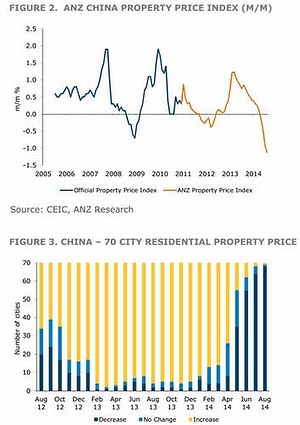

- We believe that the current downward trend in the property prices will be extended to next year.

- As the housing investment represents 25% of the total fixed asset investment and is closely associated with many industries and the banking sector, Chinese authorities will likely introduce more supportive policies, including favourable tax and mortgage policies, before the end of this year to ease the downward pressures on the property market.

- Currently, only seven cities (Beijing, Shanghai, Guangzhou, Shenzhen, Zhuhai, Nanjing and Lanzhou) still maintain the ‘property purchase limit’ policy, compared with 46 at the end of last year.

- We thus expect more monetary policy easing in the remainder of this year, if the upcoming data continue to remain lukewarm. We cannot discount the possibility of an outright 50bps RRR cut for the whole banking system, or even a policy rate cut.

Jeez, you wish. This has been the ANZ line for years now as it’s trailed the PBOC and growth down. It’s clear that the PBOC is supporting the banks with greater liquidity but if they wanted to “counter the slowdown” then it’d be doing much more than this.

Again, this is a managed structural adjustment to slower growth driven by less credit-intensive and more productive sectors and supported by fiscal spending (some of it funded monetarily), not a normal Western credit cycle. If the rate cuts that ANZ has been screaming for for years finally come then it will be a sign either of panic or satisfaction that the adjustment is underway and no credit rebound is in the offing.