We anticipate a change in market leadership away from Banks – but not necessarily all in favor of Resources. Such a rotation will have significant impact on the ASX Top 30 as a source of liquidity, and extension towards both cyclical and structural growth themes outside of that incumbency.

We hold our rolling 12-month index target of 5,800: It implies limited 3.5% capital upside. We see both major sectors, Banks and Resources, struggling to outperform.

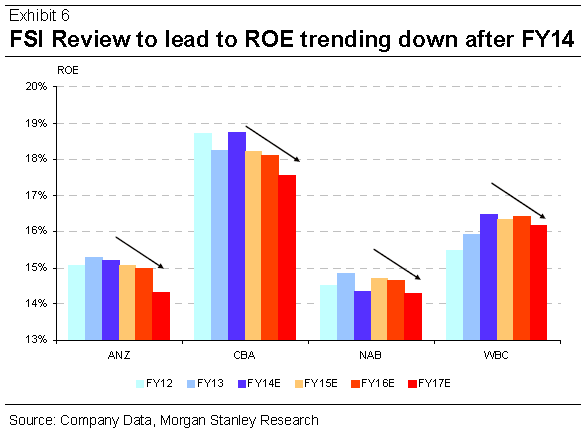

Banks and the FSI – more capital and lower ROE: In their accompanying report, our Banks team has taken a more negative stance on the group. We concur that likely recommendations of the final FSI report will challenge the market’s ability to justify already stretched valuations and limit both earnings and dividend growth.Our model portfolio now moves UW Banks with exposure to CBA, NAB and WBC, in line with our Banks team’s order of preference.

Resources can’t take it all: If life was simple, the “big switch” would be simply reallocating capital from Banks to Resources. Yet ongoing headwinds to commodity dynamics from China’s reform process make this only part of the story. We remain OW on BHP and ILU and move sector-neutral by lifting our RIO position to index.

Timing the yield unwind: The prospect of rates rising (eventually) will put some pressure on the yield trade. However, Australia has a broad spectrum of yield. We expect bond proxies to feel the brunt of any rise in long bond yields, but blue-chip yield (especially with growth) will remain supported while Australian cash rates are held low. We close underweight positions on TLS and WES. Where to focus? A change in market leadership away from Banks will affect a broad selection of sectors. Our focus and source of change within our model portfolio sits within Non-Bank Financials, Global Growth exposures, Blue Chip dividend growers and mid-caps with cycle agnostic and structural growth prospects. We retain our conviction in housing-linked themes and stocks with a view to retaining exposure to the domestic cycle.

I have obviously been shouting from the rooftops similar thoughts about asset allocation since late 2011. It poses a real problem for the traditional buy and hold baby boomer investor. Banks and miners constitute half of the bourse and most of that is in the ASX8. If banks roll over, and resources do worse than MS reckons on (it sees iron ore at $90 for the next two years) then there’s going to be no income growth in the economy and declining rates of lending growth that will seriously inhibit local-facing industrial profits as well.

What MS is really describing here is an oncoming gale for share market growth, with the exception of its non-resources external sector.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.