From Westpac:

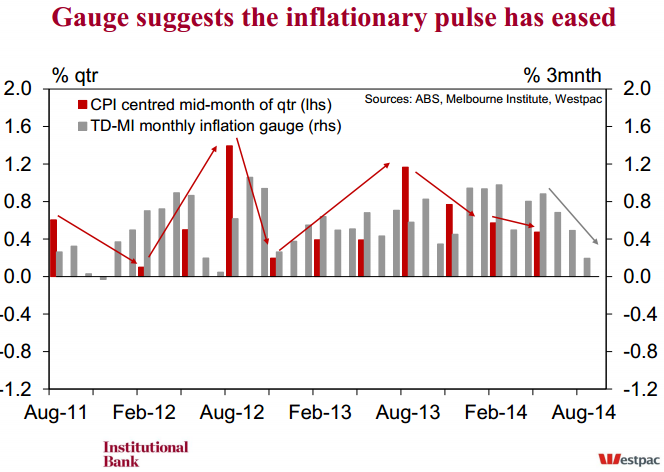

The Gauge was flat in August (–0.01% at two decimal places) following a 0.2% increase in July and a flat print in June. The annual pace has accelerated eased back to 2.5%yr in August from 2.6%yr in July and a recent peak of 3.0% in June. The most recent low was 2.1%yr in Oct 2013.

• Whereas a few months ago the gauge was threatening to breach the RBA’s inflation target band, now it has eased back into the mid-point. Westpac had been forecasting inflation to pick up in late 2013/early 2014 and then ease but we have to admit we are surprised by the rate of deceleration.

• The annualised three monthly pace is now just 0.8% from 2.0% in July and 3.8% in June. For the month, Westpac estimates a small historical negative seasonal factor for August and notes we are heading into the seasonally softer fourth quarter.

• The trimmed mean fell 0.1% in August, following a rise of 0.4% in July. The trimmed mean increased by 0.4% over the three months to August, following a rise of 0.5% for the three months to July. In the year to August, the trimmed mean rose by 2.7%.

• TD-MI reports that contributing to the overall change in August were price rises for fruit & vegetables (+2.3%), furniture & furnishings (+1.3%), and newspapers, books & stationery (+3.8%). These were offset by falls in health (-0.8%), automotive fuel (-3.5%), and holiday travel & accommodation (-1.2%).

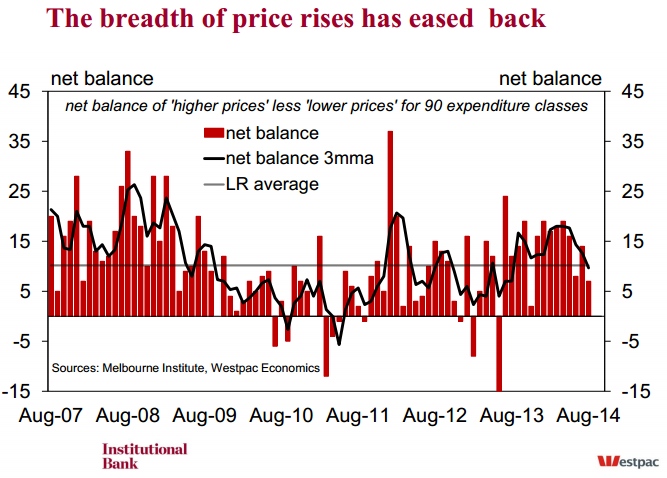

• The net balance (number of price rises less number of price falls) has eased back to 7 from 14 in July. It is still now less than the long run average of 10 and the 2013 average of 9. It is also a step down for the average of 14 for the last six months.

• The Q2 CPI surprised with a modest 0.6%qtr and as such, left the Gauge tracking well ahead of it. The August Gauge is pointing (now we have the mid-month of the quarter to work with) to a very benign 0.2% rise in the Q3 CPI. But the Gauge has been running well ahead of the CPI and historically, there have been points like this where the CPI has “caught up”.

As expected. The moment housing slows, rate cuts will flow. Full report here.