The sell side is piling into the banks now. From Morgan Stanley:

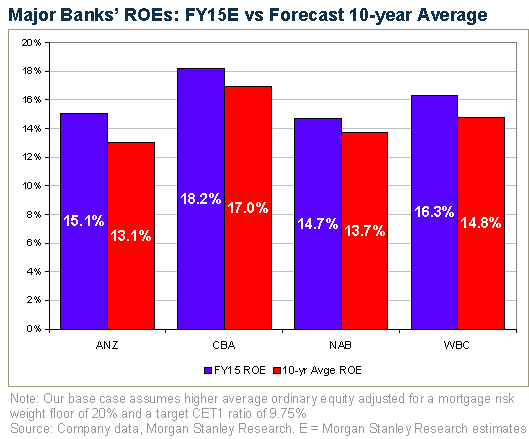

We believe the Murray Inquiry will lead to more onerous capital requirements for the major Australian banks, and our revised forecasts assume a 2% D-SIB buffer (vs 1% currently) and an increase in mortgage risk weightings (via a 20% RW floor). This implies an additional capital requirement of ~A$24bn, based on our FY15 CET1 forecasts. While near-term EPS dilution could be mitigated by a 2-3 year transition period and oligopoly pricing power, we ultimately expect more capital to drag on the major banks’ ROEs. Our Chart of the Week shows that we forecast the 10-yr average ROE to be 1-2%pts lower than the FY15E level. With the Murray Inquiry’s Final Report due at about the same time as the G20 Summit in November, we believe the prospect of more onerous capital requirements and lower “sustainable” ROE will be top of mind for investors. Accordingly, we feel that the risk of a trading multiple de-rating will increase.

The AFR’s Chris Joye quotes UBS as more aggressive still:

UBS’s top ranked bank research team have almost doubled their estimates of the amount of capital Australia’s major banks may have to raise in response to David Murray’s financial system inquiry, from $23 billion to $41.1 billion.

In a new report, UBS say that “given Australia’s unique situation as a small, commodity based economy, heavily reliant on foreign capital, with a very concentrated banking system, David Murray is likely to err on the side of caution.

…In July UBS analysts Jonathon Mott and Adam Lee – who were ranked Australia’s number one bank researchers in two well-respected surveys – calculated that the majors would have to source an extra $23 billion of common equity tier one capital assuming the FSI recommended a 3 per cent capital buffer for too-big-to-fail (TBTF) institutions. APRA’s current TBTF capital buffer is 1 per cent, which the FSI says is low by international standards.

Mr Mott and Mr Lee say they believe “it is highly likely the FSI will recommend adopting measures that have the effect of increasing the risk weights on mortgages for [the major banks and Macquarie]”.

“We believe this not only addresses the issue of competition within the mortgage space, but also goes to the issue of reliability of models used to calculate the majors’ risk weights.”

Advertisement

Let’s hope so. I’ll note again that there is a difference between the inquiry, the Government’s response and what the regulators want.

It throws up a vital question. If MS is right then we’ll still talking 14-16% ROE for the banks. If UBS is right then it’ll be more like 12-14%. These are still spectacular returns for any business, let alone banks. They are, in fact, still far too high if we’re serious about resilience. As Martin Wolf recently argued:

The business model of contemporary banking has been this: employ as much implicitly or explicitly guaranteed debt as possible; employ as little equity as one can; promise a high return on equity; link bonuses to the achievement of this return target in the short term; ensure that as few as possible of those rewards are clawed back in the event of catastrophe; and become rich. This was a wonderful model for banks. For everybody else, it was a disaster.

The new regulatory regime is an astonishingly complex response to the failures of this model. But “keep it simple, stupid” is as good a rule in regulation as it is in life. The sensible solution seems clear: force banks to fund themselves with equity to a far greater extent than they do today.

So how much capital would do? A great deal more than the 3 per cent ratio being discussed in Basel is the answer. As Anat Admati and Martin Hellwig argue in their important book, The Bankers’ New Clothes, significantly higher capital – with true leverage certainly no greater than 10 to one and, ideally, lower still – would bring important advantages: it would limit the implicit subsidy to banks, particularly “too big to fail” ones; it would reduce the need for such intrusive and complex regulation; and it would lower the likelihood of panics.

Advertisement

10% true equity as a bare minimum. But for banks to be genuinely stable they should be delivering utility-like returns in the 7% range, capital of more like 15%, two and a half times what is being contemplated for our banks.

A little perspective there for when next you hear a banker whine.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.