by Chris Weston, IG Markets

Trading the ever-diverging paths from the major G10 central banks has been one of the most successful thematics that have played through the markets for the last couple of months. But has this trade become long in the tooth?

Fundamentally, this divergence doesn’t look like disappearing anytime soon. In fact, in the case of Europe it looks like the trade may still be in its infancy. As previously suggested, being short currencies where the central bank is trying to spur inflation (and predominately inflation expectations), while being long currencies in economies where we are likely to see more restrictive policy settings has a been a winner. The concern now is whether these extreme moves are negatively affecting underlying economics.

Certainly, in the case of Japan we have seen a number of top-ranking officials detail that the recent JPY weakness isn’t benefiting all corporations, with recent commentary from Shinzo Abe actually seen as talking up the local unit. In the US, we have now heard comments from Federal Reserve members Charles Evans and Bill Dudley on the recent USD move and, given the Fed’s own inflation forecasts is for core personal consumption expenditure (PCE) to hit 1.65% this year, there is concern that these predictions will be tough to achieve as a result.

Inflation expectations falling due to USD strength

What’s interesting is, if you look at the US bond market, we’ve seen inflation expectations coming off fairly quickly of late. As things stand, inflation is now expected to average a mere 1.68% over the coming five years – go back to July and the market’s expectations were 40 basis points (or 0.4% higher). If inflation is going to face sizeable headwinds from USD strength over the coming years (given its star qualities in the G10 region), then we have to think that this could act as a self-correcting mechanism as well.

With the USD index breaking the multi-year downtrend yesterday, it feels like today’s session could be very interesting. Naturally, most of the strength has been seen against the EUR and I question who is left to sell EUR/USD at current levels. From a pure risk-to-reward perspective, long positions are favoured, but there are no technical signs expected for rampantly oversold conditions.

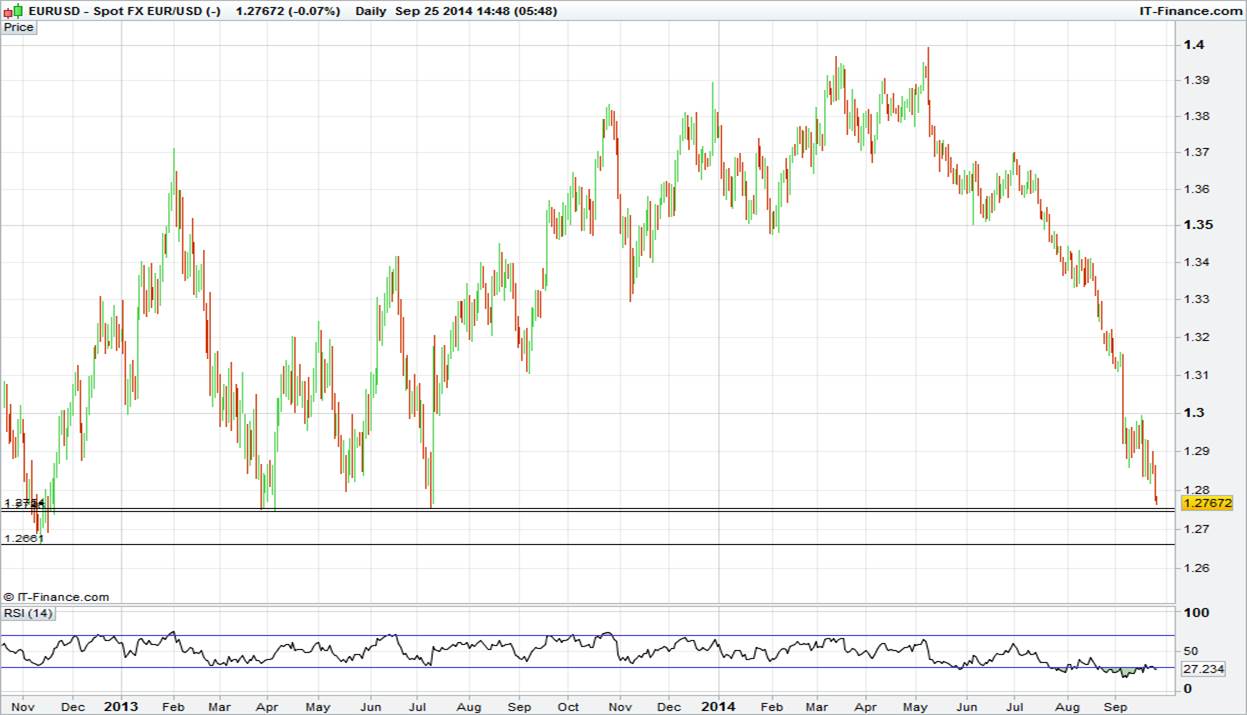

Sellers have been seen again today, with comments from Mario Draghi coming to light through midday trade. Once again, the ECB president highlighted the central banks’ ability to use unconventional instruments if needed. Judging by the European swaps markets, inflation expectations (at 1.92% over five years) suggest few believe the current targeted balance sheet expansion is going to create inflation, even with the ECB doing an excellent job of lowering the currency. Today’s Eurozone M3 money supply numbers could provide some support if we see a tick up (1.9% expected), especially with the 2013 lows of US$1.2746 firmly in the bears’ sights.

New highs expected in the S&P 500 and Dow

European markets had a strong day yesterday on the idea that the Fed is doing all possible to approach rate hikes with a ‘softly softly’ attitude, while bad news (German business climate) was seen as good news for stocks – the market has QE in its sights. The S&P 500 and Dow Jones Industrial average both printed bullish outside day reversals (ie the price traded below Tuesday’s low and closed firmly above Tuesday’s high), which suggests a continuation of the uptrend. It seems feasible that we’ll see new highs in both these markets.

Asian markets, with the exception of the ASX 200, look strong. the Shanghai Composite moved to the highest level since March 2013 and took the gains from June to 17%. Clearly no one is too concerned with speculation that the head of the PBOC (Zhou Xiaochuan) may be replaced in the coming months, although this may be because he is perceived by the market as fairly hawkish. In Japan, the Nikkei has traded to the highest level since 2007 courtesy of USD/JPY pushing to ¥109.34. As with EUR/USD, I struggle to understand who is left to buy USD/JPY. From a pure risk-reward perspective, shorts are preferred.

Perhaps a catalyst for USD profit taking will materialise today, with Atlanta Fed president Dennis Lockhart due to speak on the US economy. Recall he is to be a voting member next year, so his comments (notably around inflation and the USD) will be closely followed. We also get weekly jobless claims, durable goods and capital goods orders, which could play into future GDP reads. Elsewhere, BoE head Marc Carney will be speaking in Wales.