by Chris Weston

It will be an interesting week for short-term-focused traders, with a number of markets that have recently seen better trending conditions exerting clearly overbought or oversold conditions.

The sell-off that has materialised in the US bond market of late is coming at a time when we have seen some fairly bearish dynamics in other economies and, as a result, we’ve seen some strong trends in AUD/USD, EUR/USD and USD/JPY. These trends have led to some one-sided positioning, with the 14-day RSI on USD/JPY at the highest level since 2001. We seem to have got to a point where we could see traders taking some profits.

The USD could consolidate this week

The US bond market will therefore remain the key driver for the USD and, if we take the five-year US treasury in isolation on Friday, we saw a strong key day reversal. Here the yield traded aboveThursday’s high and closed well below Thursday’s low, which in theory could signal a change in trend. What’s more, the futures market has opened today and, as buyers have stepped in again, the yield has made a lower low. It’s hard to see aggressive buying in US fixed income though, especially after we saw the biggest weekly outflow of US bond funds for the year last week. However, if we do see consolidation in the US bond market, it may give those long USDs a chance to take profits.

Fundamental drivers this week will be Q2 US GDP revisions (expected to be revised up to 4.6%), with August durable goods and capital spending in play. I’d be looking more closely at narrative from the raft of Federal Reserve speakers this week, with Bill Dudley (dove and permanent voter) due in early US trade (00:05 AEST) today.

Certainly, the trend today has been to sell USDs, although it’s been interesting to also see good selling in silver and gold as well. Spot silver looks awful on either the daily or weekly chart. However, the metal is grossly oversold and given the ten-day correlation is negative 81%, we have to feel that, if the USD is offered this week, then perhaps short covering will materialise in silver.

It should be said that the trend is lower and the ease by which price smashed through the June 2013 lows has to be accounted for. Spot gold has hit a low of $1208.37 today, with the key objective for the gold bears clearly the 2013 double bottom of $1180. Still, while the momentum trade is to short these metals, both are technically oversold and rallies could provide a better opportunity.

Having said this, I would not be putting new money to work on the short side.

Equities have been sold in Asia today as well, as China leads the charge with the CSI 300 down 2.1%. Iron ore and rebar futures have collapsed again with both down around 3%, although local repo rates have also fallen on the back of last week’s capital injection by the PBOC – and this should have helped stabilise sentiment. It was interesting to see the underperformance of emerging markets in general of late, with investors pulling $1.1 billion out of emerging market equity funds, the first outflow seen in 15 weeks.

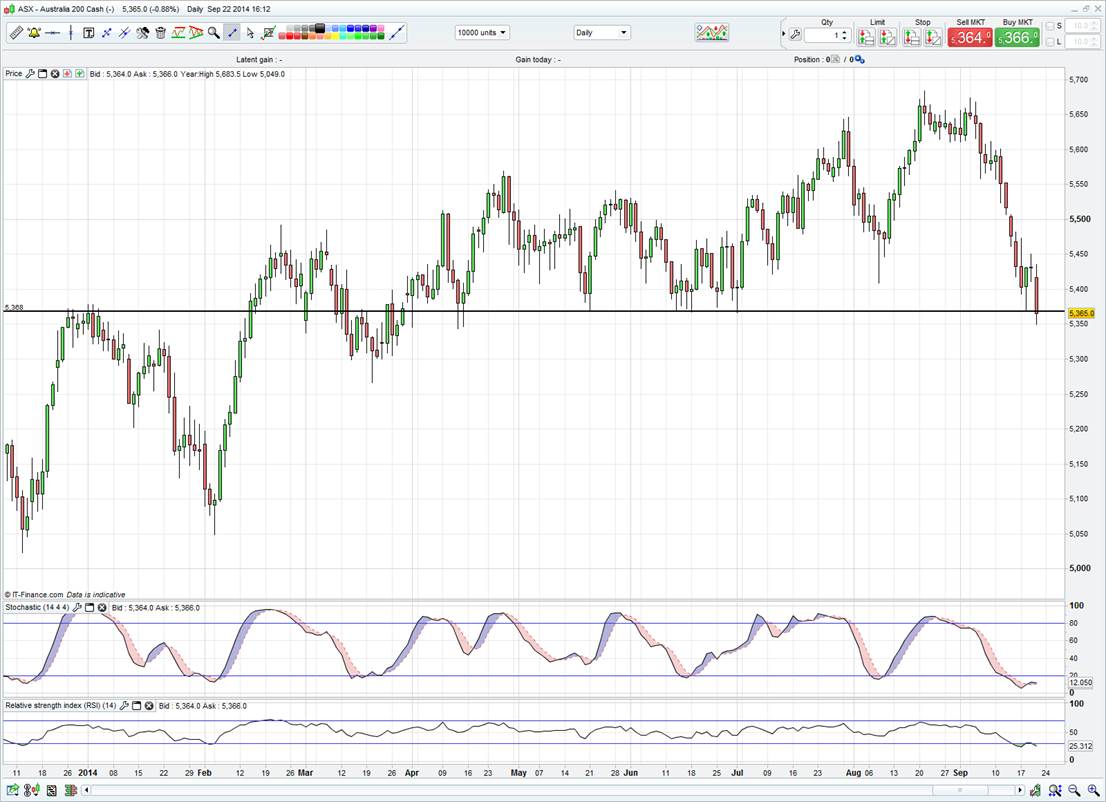

Bears in control of the ASX 200

The ASX 200 has closed down 1.3%, while the Nikkei is down 0.7% and the falls here have caused US futures to come under strong pressure today. S&P futures are down 0.5%.

The sell-off in the Aussie banks continues to be a talking point, with the financial sector having corrected just over 6% from the September pivot high. Material names have been smashed as well. Fortsecue Metal is down 4.7% and nearly three quarters of all client orders at IG today have been to open short positions and profit from the lack of clarity in the space.

The broader index has broken the 2012 uptrend now and is looking to close below strong horizontal support at 5370. This level has seen good bids coming in since May and a break here could see the March 20 swing low at 5266 come into play. It’s also interesting to see that, while the banks will naturally take out the lion’s share of the index points, the selling has been broad-based.

The ASX 200 has fallen 5% since 3 September and a cautious stance is clearly warranted, as I detailed last week. On 3 September only 32% of ASX 200 companies were below their short-term 21-day moving average, but now that figure stands at 81% – so it’s fairly clear that the selling has been broad-based.

Europe has challenges of its own, with various ECB officials debating policy over the weekend. Of note, commentary from Governing Council member Ignazio Visco pointed out that the falls in the EUR may reduce the need for future stimulus. Certainly, the collapse in EUR/USD from $1.3995 on May 8 should in theory put upside for inflation expectations. However, what is worrying is that five-year inflation expectations (I have looked at five year swaps) have pulled back to the lowest level since 2010 at 1.91%, well below the five year average of 2.28%.

Given the ECB look at this metric very closely, the fall in the EUR hasn’t translated into heightened inflation expectations – especially given they note every 10% decline in the EUR should increase inflation by forty to fifty basis points. It seems there are some very interesting and perhaps concerning dynamics playing out in Europe right now.