Most of Asia has continued to struggle today, with a degree of caution being exercised ahead of next week’s FOMC meeting, a raft of China data and fresh EU sanctions on Russia. The FOMC meeting takes place in the middle of next week and it seems the market is growing increasingly hawkish on the Fed. Additionally, with QE due to wind down completely, the Fed is expected to flesh out some detail around the exit strategy and no doubt the debate around the fed funds rate will continue.

Having said that, we do know economic data will be the trigger. Continuing to monitor how the economy is progressing will therefore be key. There has been plenty of talk of the beginning of a cycle US-dollar bull market and it seems USD/JPY and Japan have been the biggest beneficiaries of this so far. The assumption is that the market will continue to readjust its fed funds rate expectations to a Fed committee median.

Out of the US today we have retail sales, consumer sentiment and inflation expectations. Equities are mixed in China as we head into a couple of days of key data releases. New loans, money supply, industrial production, fixed asset investment and retail sales are all set to be released by tomorrow and will help set the tone for Monday trade.

As China and key commodities struggle, so has the AUD, which has printed a fresh five-month low against the greenback and is showing no signs of stabilising. A retest of $0.9000 seems to be on the cards in the near term.

Yen weakens ahead of Kuroda speech

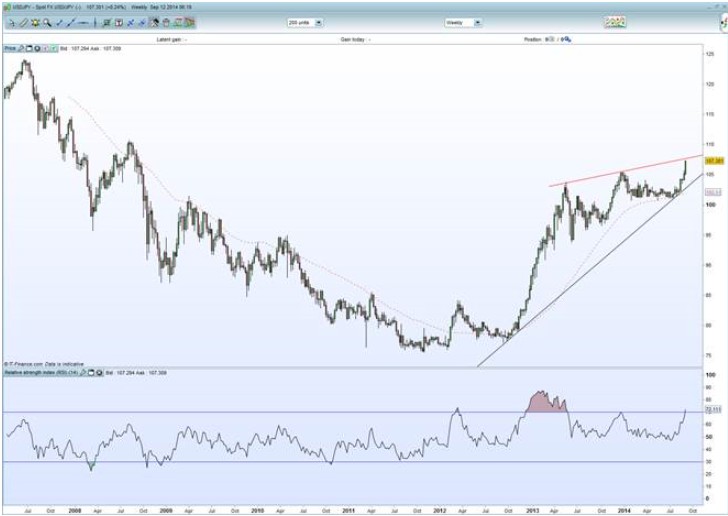

Japan has been an exception and excelled yet again in a choppy environment as USD/JPY continues its run. The pair has continued its run and has now taken out the ¥107.00 handle. It has now comprehensively pushed through December highs and is trading at its highest since September 2008. This has bolstered the exporters and in turn has aided gains for the Nikkei.

Earlier in the week, I highlighted how the Nikkei is paving its path back to 16,000 and we’re not at all far off from that level now. The Nikkei is likely to play catch up to the gains seen in USD/JPY and, once the 16,000 level is breached, traders will be targeting January highs above 16,000. The BoJ put seems to be back in full swing, as recent comments suggest they are ready to act if need be.

With governor Kuroda scheduled to speak again today, traders are happy to remain long Japanese equities. An interesting development on the USD/JPY weekly chart is a rising wedge pattern forming as the price action compresses. A rising wedge is actually a bearish signal and, as the trend lines converge, there is a risk a reversal will emerge. Essentially, this indicates the price momentum is weakening. The resistance currently lies at around ¥107.70. Having said that, the pair has only just nudged into overbought territory with the RSI now at 72. There could be more room to move. Importantly for traders already long USD/JPY, the most logical step would be to trail stops and see how the price action reacts in coming days.

(USD/JPY at 2008 highs)

Europe in for some nervous trading

Looking ahead to European trade, we’re calling the major bourses marginally firmer. Focus will primarily be on the fresh sanctions on Russia and reports the Kremlin is already planning a retaliatory package of its own. A number of new sanctions were imposed and mainly focus on barring state-owned banks from borrowing, debt financing to defence companies, energy-related restrictions, military technology and blacklisting some of the country’s oligarchs.

At the same time, the UK will be positioning ahead of the latest Sunday Times YouGov poll. Last weekend’s poll set the tone for the sterling and equities early in the week after showing the ‘yes’ vote in front for the first time. This could keep the FTSE at bay in today’s trade, with just a week to go before the vote. Should the vote spark further fears and the sanction situation intensifies, the euro and sterling’s stability could be temporarily affected.