Yes, according to “Mad” Adam Carr:

If the Reserve Bank of Australia wants a lower currency, then the smartest thing it could do — right now — is hike rates.

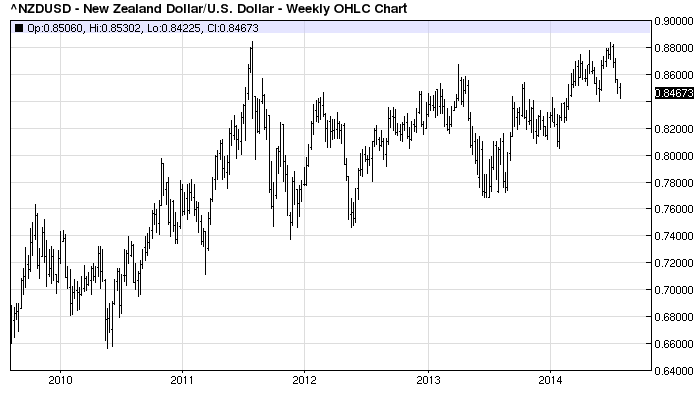

…take a look at New Zealand’s experience. The Reserve Bank of New Zealand has hiked rates four times in four months — a full percentage point to 3.5% — and the currency has done little. Indeed it’s one of the more remarkable features of its tightening cycle to date — just how stable the kiwi has been. Against the US dollar, the kiwi is virtually unchanged from March, when it started tightening, at US84.6c. Going back to the start of the year it’s not much worse, maybe 2c higher or so and only 3 and a bit cents higher compared to the average exchange rate since 2011.

Let’s take a look. Here’s the NZD/USD chart over the past five years:

Does that look to you like a currency that’s not rising? No. Obviously markets discount future moves and that’s exactly what’s happened in the Kiwi, up over 10% since mid 2013 in a larger rising trend since 2009.

Moreover, as MB’s five driver’s model of currency valuation is designed to show, a currency is driven by much more than interest rates. The New Zealand terms of trade have crashed since the rate hikes began, though it hasn’t yet shown up in official figures, yet the currency remains very high. That is, rate rises are offsetting other declining fundamentals in keeping the currency up.

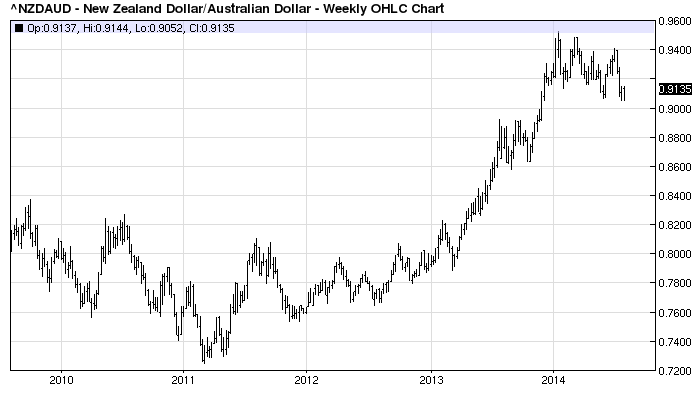

It’s even more obvious in the NZD/AUD, which screamed higher in anticipation of the rate hikes:

Now, yes, the rate hikes are slowing housing markets and the economy and so the NZD has retraced a little. But it’s economy is in a boom with rapidly falling unemployment.

In Australia’s case, with the capex cliff in full swing next year and trend unemployment marching higher, is it good policy to step on the economy to win the currency war?

A better idea might be to look at a few charts and then install macroprudential tools that enable you to lean against credit without blowing anything up.