More good data in the US overnight with Pending Home Sales strong:

The Pending Home Sales Index, a forward-looking indicator based on contract signings, climbed 3.3 percent to 105.9 in July from 102.5 in June, but is still 2.1 percent below July 2013 (108.2). The index is at its highest level since August 2013 (107.1) and is above 100 – considered an average level of contract activity – for the third consecutive month.

Weekly unemployment claims were firm:

In the week ending August 23, the advance figure for seasonally adjusted initial claims was 298,000, a decrease of 1,000 from the previous week’s revised level. The previous week’s level was revised up by 1,000 from 298,000 to 299,000. The 4-week moving average was 299,750, a decrease of 1,250 from the previous week’s revised average. The previous week’s average was revised up by 250 from 300,750 to 301,000.

Q2 GDP revisions were good:

Advertisement

Real gross domestic product — the output of goods and services produced by labor and property located in the United States — increased at an annual rate of 4.2 percent in the second quarter of 2014, according to the “second” estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP decreased 2.1 percent.

The GDP estimate released today is based on more complete source data than were available for the “advance” estimate issued last month. In the advance estimate, the increase in real GDP was 4.0 percent.

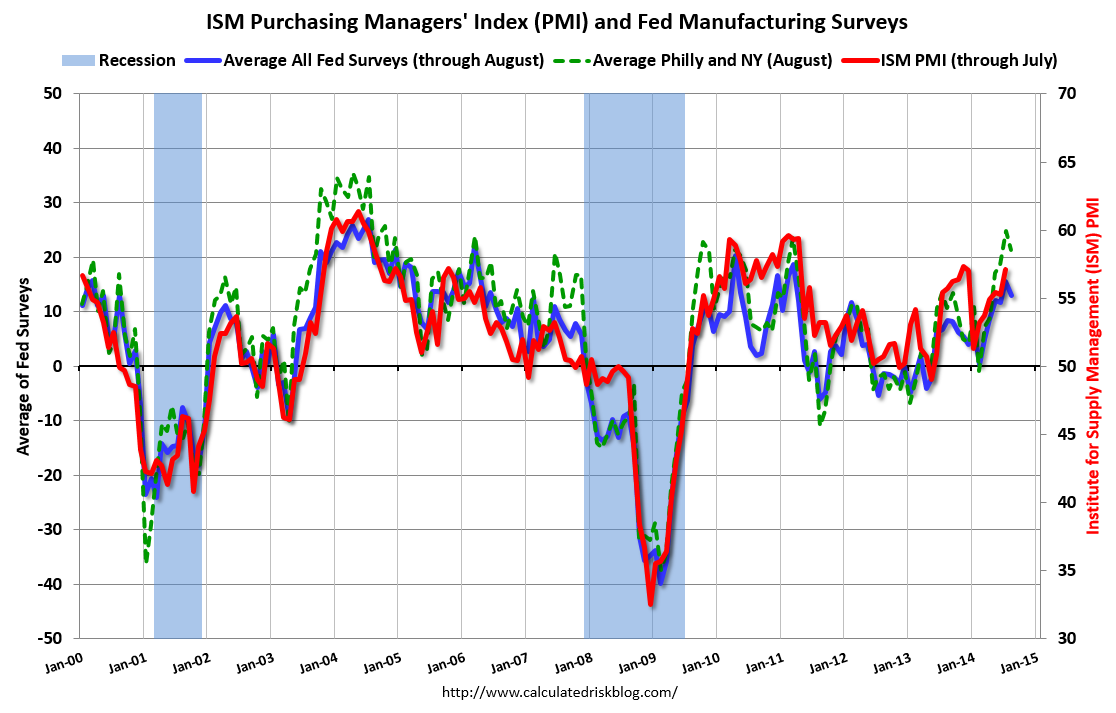

The Kansas City Fed manufacturing index eased from 6 to 3 but as Calculated Risk notes, the signs for the ISM are good:

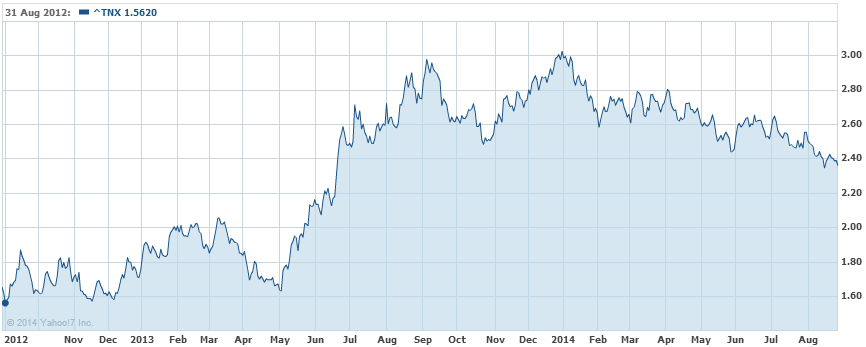

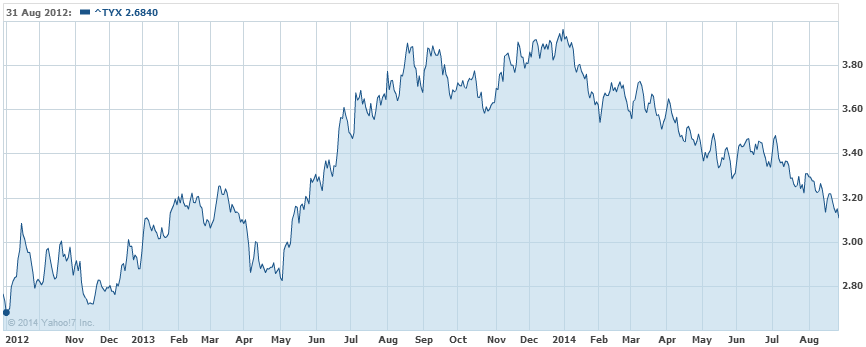

So, good momentum in the US economy but stocks still took a breather and long bonds were bid aggressively with the 30 and 10 year yields both at new 2014 lows:

Advertisement

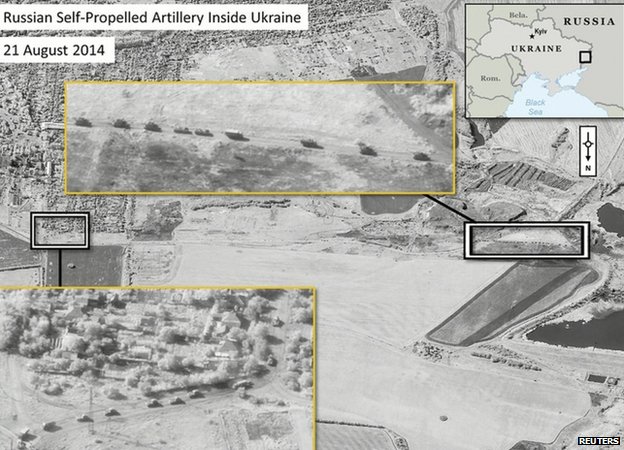

The proximate cause was war on two fronts. The first, in Iraq, is till building towards a bombing campaign by the US, UK and Australia. The second, in Ukraine, has escalated as Russia appears to have invadedin some way:

Nato has released satellite images it says show Russian armed forces inside Ukrainian territory to help rebels fight government forces.

Ukraine’s president held a security council meeting on Thursday over the “sharp aggravation of the situation“. Russia has denied the claims.

…At least 2,119 people have been killed in four months of fighting.

Amid condemnation from Western powers, the United Nations Security Council has held an emergency meeting in New York to discuss the crisis.

President Barack Obama acknowledged during an impromptu press conference on Thursday afternoon that the United States is considering new sanctions to impose against Russia over the escalating crisis in Ukraine.

From the White House, Pres. Obama told reporters that he’s certain Russia is playing a direct role in the ongoing fighting in eastern Ukraine between anti-Kiev separatists and the country’s military, and that the US is weighing further sanctions to intensify the restrictions previously waged against Moscow.

“As a result of the action Russia has already taken and the major sanctions we’ve imposed,” Obama said,“Russia is already more isolated than any time since the end of the cold war.”

“The separatists are backed, trained, armed, financed by Russia. Throughout this process we’ve seen deep Russian involvement in everything that they’ve done,” Obama added.

That behavior, he added, “will only bring more cost and consequences to Russia.” After speaking with allies, Obama continued, he expects a new wave of sanctions to come soon. The president is expected to meet with NATO partners next week, and said the US “will continue to stand firm with our allies and partners” to protect Ukraine from further encroachment.

I still don’t expect this to escalate beyond a proxy war but Russia is clearly going to push the envelope.

Advertisement

The upshot is a bid for US assets, though the USD took a breather and the Aussie climbed towards 94 cents. There’s no risk off yet.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.