After the strong run of payrolls outcomes through the first seven months of 2014 (annualised employment growth of 2%), attention is turning towards wage outcomes and implications for inflation.

As such, the Q2 Employment Cost Index (ECI) gave markets a jolt, the headline outcome reporting a 0.7% gain in total compensation, more than twice Q1’s 0.3% gain. Providing further food for thought was the 1.0% gain in the benefit component – again a stark contrast to its 0.4% Q1 rise. Annual total compensation growth is currently at 2.0%yr, with wages up 1.8%yr and benefits 2.6%yr higher. Effectively we are at the threshold for real wages growth.

The likelihood of an accelerating wages trend and its potential implications for the economy are therefore critical to consider. Herein, the ECI and nonfarm payroll industry detail are instructive.

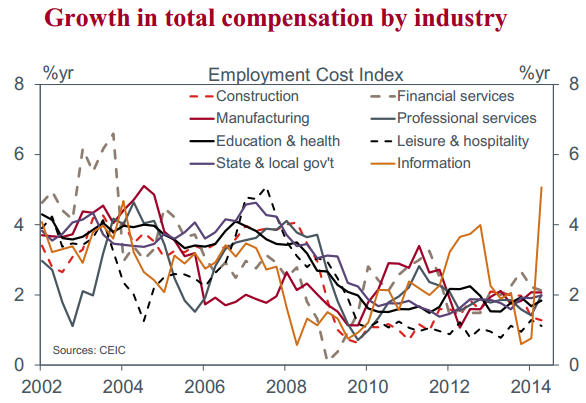

Considering the available detail for total compensation by industry, what becomes immediately apparent is that Q2’s upside surprise was essentially driven by one sector: information technology (IT).

In Q2, annual growth in total IT compensation rose from 0.8%yr to 5.1%yr, driven by a 4.8% spike in the quarter. This compensation growth was not primarily due to stronger wages growth, but rather surging non-wage benefits. IT wages growth was comparatively soft, a 0.9% gain in Q2 (following –0.2% and +0.4% outcomes in Q4 and Q1 respectively) leaving annual growth at 1.6%yr.

Detail on the benefits paid by industry and the key factors driving movements in each sector are not provided by the ECI. But we were told that the rise in total benefits has primarily been driven by a 2.4%yr rise in the cost of retirement benefits and, to a lesser extent, a 2.7%yr increase in health benefits. Anecdotally, given the IT sector is known to provide considerable non-wage benefits to its workforce and ‘Affordable Healthcare’ was introduced on 1 January 2014, the Q2 IT surge is likely due to health benefit costs.

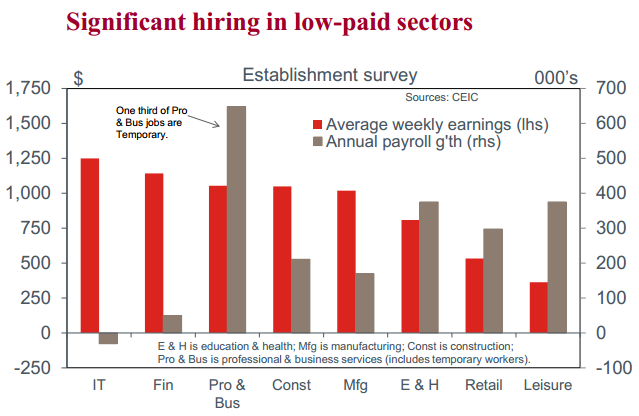

In considering the likely impact of this impulse for the aggregate economy, we need to consider the scale of the IT workforce and employment growth in the sector. From the payrolls survey, not only do we find that IT workers make up less than 2% of the total workforce, but also that employment in the sector has actually fallen by 31k over the past year. As such, the spike in compensation has effectively been wiped out by job losses.

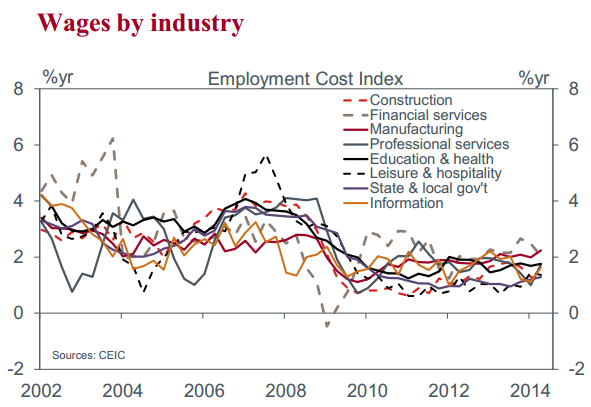

The wage trends for the sectors that have been hiring lack the momentum apparent in IT. Collectively, Education & Health (15%); Retail (12%); and Leisure & Hospitality (15%) have made up 42% of total jobs growth over the past year. Total compensation growth in these sectors remains broadly stable at 1.8%yr, 1.7%yr and 1.1%yr respectively. Wages growth has been similar, at: 1.8%yr; 1.6%yr; and 1.4%yr. Of these jobs, we do not know what proportion are full or part-time, the latter typically receiving no benefits and a lower weekly income owing to less hours being worked.

Similarly, for professional & business services (26% of total jobs over the past year), total compensation and wages have risen 2.0%yr and 1.7%yr respectively. As a third of these jobs have been temporary positions, the 1.7%yr gain in wages is likely to be the better proxy for income growth in the sector – as for part-timers, temporary workers do not rec eive benefits from their employers.

Given the above outcomes and that the core PCE inflation measure is up 1.9%yr, on both a wages and total compensation basis, real payments to households per unit of labour input have fallen further over the past year for the vast majority of workers.

Real wages growth would require additional strong quarters strung together; there is little evidence of such a trend developing.

Another critical factor to consider on the wages front is that new entrants seemingly continue to experience less favourable wage outcomes than established workers. This is apparent above in the importance of temporary workers; but of more concern are thewage outcomes of new graduates.

A recent Economic Letter by the San Francisco Federal Reserve found that “Starting wages of recent college graduates have essentially been flat since the onset of the Great Recession in 2007”. Further, this was attributed not to a switch in the type of jobs taken by graduates, but rather because “recent graduates experienced lower wage growth than other workers”.

Abstracting from IT, we continue to await a meaningful movement towards positive real wages growth. Further, it is unclear to what degree the reported wage outcomes have been mitigated by part-time hiring practices. Together with the absence of wages growth for new graduates over seven years, these results speak to considerable slack remaining in the US labour market.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.