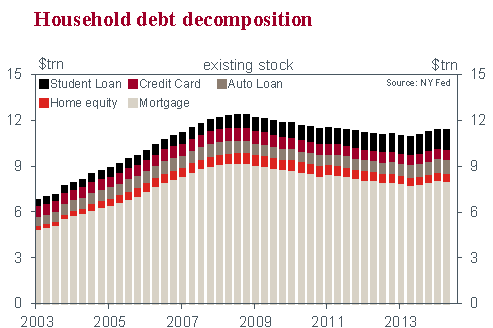

While it may not receive the press coverage of headline data outcomes, the NY Federal Reserve’s Quarterly Report on Household Debt and Credit is as important, providing an up-todate portrait of the evolving financial position of US households. As at June 2014, the accrual of additional debt remained decidedly out of favour amongst US households, with consumer indebtedness edging $18bn (0.2%) lower in the three months to June 2014 to $11.63trn.

Highlighting the distinct absence of activity in the US housing market, mortgage balances were reported to have declined by $69bn (0.8%) in the three months to June; the balance on Home Equity Lines of Credit (HELOC) also fell by $5bn (1.0%). The Q2 result continues a multi-year downtrend that has seen the stock of housing credit fall from $9.99trn in September 2008 to $8.62trn as at June. This is not just a function of existing households prepaying their mortgages and defaults; originations (incl. refinancing) fell to $286bn in the June quarter, the weakest pace since 2000.

In contrast, since September 2008, non-housing debt has risen from $2.69bn to $3.02bn. This has come as a result of a near doubling in the stock of student debt (from $0.61trn to $1.12trn) and, since June 2010, a $210bn increase in auto debt to $0.91trn (following a $110bn decline between September 2008 and June 2010). A $190bn decline in credit card debt (to $0.67trn) and a $90bn fall in ‘other’ consumer debt (to $0.32trn) have been partial offsets against the rise in student and auto debt.

Herein we see evidence of a lingering tension in the US economic narrative: consumer demand continues to strengthen in areas where credit is freely available. But, outside of this this subset, activity remains constrained by weak income growth. For housing, where lending standards are much tighter, many households’ still substantial legacy liabilities are a further (major) impediment.

On loans for education, with the system operated by the Federal Government and individuals typically unable to extinguish their debt in bankruptcy, there is little need for credit standards. The Government’s willingness to provide loans to students (and their parents) for undergraduate and post-graduate study incentivises demand, particularly in an era where strong education credentials are a necessary but not sufficient characteristic to vie for a quality position (i.e. full-time, permanent employment). From both a supply and demand perspective then, it is unsurprising that the stock of student debt continues to rise at a robust pace.

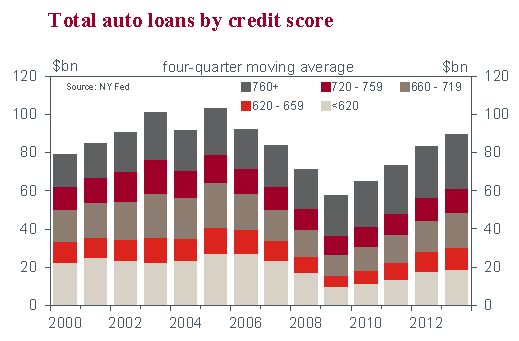

With respect to auto debt, we continue to see pent-up demand come to market as the labour market improves and we move further away from the GFC recession. $100bn of the $210bn increase in auto debt since June 2010 has been accrued in the past year; and, at $101bn, auto loan originations are now at their highest level since September 2006.

Interestingly, it has been the older age groups who have seen the strongest growth in auto debt, with the debt balance of those over 60 rising by almost 70% since mid-2010. That said, the other age groups have not been too far behind, seeing circa 50% gains. For all age groups, the increase in debt has been a function of more loans being written and the average loan size increasing in scale.

The size of the average loan taken out by each age group has now reached or exceeded its previous peak (with the exception of those aged between 30 and 39). The other dimension reported on by the NY Fed in Q2 was a breakdown of who has financed this increase in auto lending, with reference to the credit standing of auto loan borrowers.

In 2013, auto finance companies provided 53% of total car finance, a touch below the share seen immediately before the onset of recession – the 2007 average is 55%. Finance companies remained much more likely to lend to sub-prime borrowers in 2013, with 30% of finance company funded loans going to subprime borrowers (credit score <620) versus 14% for banks. The share of loans going to sub-prime borrowers is not (yet) back to the level seen ahead of the recession – the respective 2007 averages come in at 39% and 18%.

The above discussion has two main implications. Given sanguine conditions, it is reasonable to expect additional strength in durables spending and a further accrual of student debt by US households. However, absent a material improvement in labour force underutilisation and consequent trend improvement in income growth, this narrow focus on a subset of consumption willrestrict momentum elsewhere. Most notable amongst these ‘other areas’ of household demand is housing, a vital sector to which we will return next week.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.