Slowly but sure the smart money is figuring it out. From PIMCO today:

There has been ample analysis of the macroeconomic consequences of the terms-of-trade shock that Australia has undergone as the resources investment boom has tapered. Australia now must contend with a multi-year decline in the terms of trade and the required rebalancing towards the non-mining sectors of the economy as the country transitions from the investment phase to the export phase of the resource cycle.

For investors, it is important to assess how these macroeconomic forces will affect the corporate sector in Australia and thereby identify which credits are better placed to navigate the challenges that lie ahead.

The terms of trade is the ratio of export prices to import prices, and it determines the purchasing power of domestic output. Typically, a rise in the terms of trade (i.e. a rise in export prices relative to import prices) represents an increase in purchasing power and national income that helps drive higher investment, consumption and, hence, domestic demand.

On the flipside, a downswing in the terms of trade is generally associated with periods of falling national incomes, higher unemployment, constrained investment and lower consumption, resulting in below-average growth and inflation outcomes.

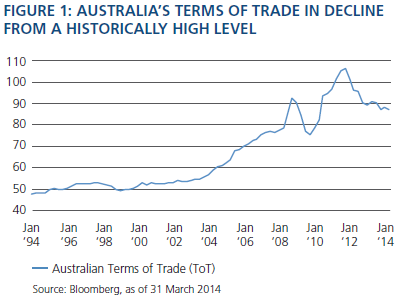

Figure 1 shows the extraordinary increase in Australia’s terms of trade as a result of the resources boom. However, since late 2011, the terms of trade has experienced a gradual decline, which is set to continue as commodity prices moderate due to an increase in supply; the completion of mining-related projects comes at a time when China, Australia’s major trading partner, is set to adjust to a slower rate of growth.

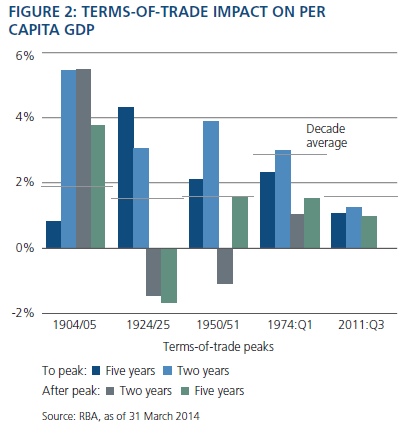

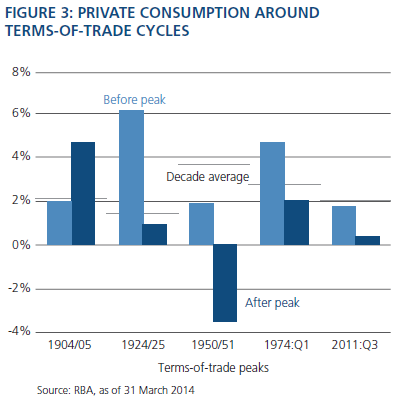

Figures 2 and 3 show per-capita GDP and private consumption during ToT spikes in Australia’s history. With the exception of 1904-1905, there is a clear history of above-trend growth prior to the ToT peak followed by a period of sub-trend growth.

Terms of trade from the corporate perspective

For companies, the macroeconomic consequences of a downswing in a nation’s terms of trade provide both challenges and benefits. The key for investors lies in identifying those firms that can best exploit the benefits and have the competitive stance to better withstand the challenges.

Simplistically, corporate profits are the difference between revenues (a function of output prices and volume) and costs (capital expenditure and wages). Clearly, the macro dynamics associated with a downswing in the terms of trade will weigh on revenue growth.

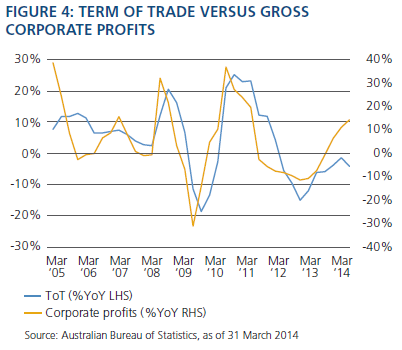

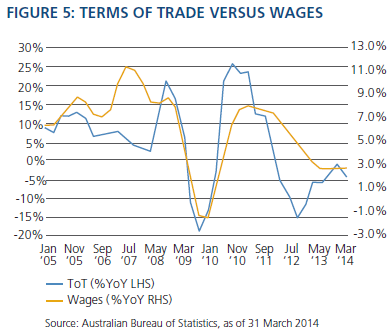

In general, sub-trend domestic demand conditions will constrain volume growth and output prices. Figure 4 and Figure 5 demonstrate the relationship between changes in Australia’s terms of trade and gross corporate profit growth (led one quarter) as well as wage growth.

While a moderate ongoing decline in the terms of trade for coming quarters will constrain profit growth, there are some benefits that are often overlooked, which should help many Australian corporates maintain strong credit fundamentals and provide investors with a framework for sector and company selection.

First, downswings in the terms of trade generally result in lower inflation. This will likely help contain wages, helping to maintain margins and cushion the fall in profit growth. Figure 5 shows that the most recent fall in terms of trade has kept wage growth at historically low levels.

The second important impact from a credit fundamentals perspective is that typically during the declining phase of a terms-of-trade cycle, business investment remains below-trend, ensuring that corporates keep leverage contained, and hence, credit fundamentals remain positive for investors. Figure 6 shows that both business credit growth and non-mining business investment remain historically low.

Finally, as the benefit of the investment phase is realised, business productivity should begin to lift. The most recent report on productivity, from the first quarter of this year, offers some sign that productivity growth has stabilised and should start to improve.

In the current environment, currency appreciation is also a factor. Exogenous forces are keeping the Australian dollar more elevated than what fundamentals and the experience of prior terms-of-trade episodes would imply. As a result, the Reserve Bank of Australia will likely have to lean more heavily on interest rates as a lever to help rebalance the economy.

Indeed, in its recent communications, the RBA has gone to great lengths to reassure the public that stable monetary policy is just that: a stable cash rate over the cyclical horizon. This should help increase business confidence that interest costs will stay stable in an absolute sense.

Companies that optimise the mix of these offsetting dynamics and enhance productivity will be better able to withstand the headwinds to corporate profitability. Thus, in evaluating the Australian corporate landscape under the prevailing macro environment, we place great importance on identifying firms that possess these features:

They hold oligopolistic or monopolistic positions that ensure greater pricing power and hence retain margins.

They operate within their geographical footprints (whether domestically or internationally) on a competitive basis and are beneficiaries of supply and demand fundamentals.

They focus on cost control, while improving efficiency, operational leverage and thus productivity.

Examining credit fundamentals

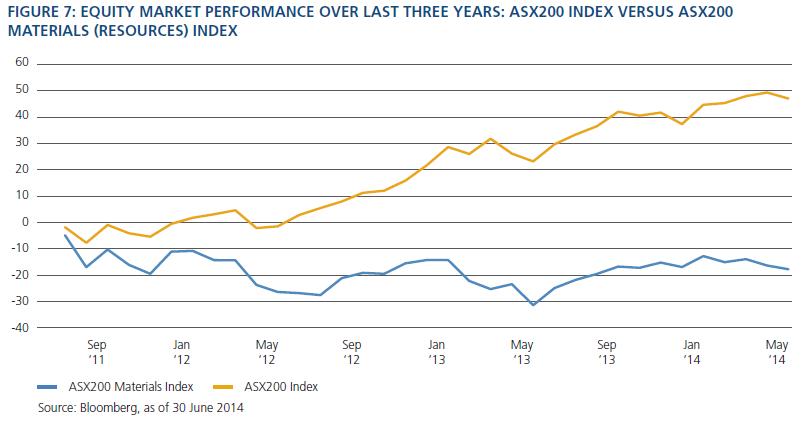

The end of the resources investment boom has not only affected Australia’s terms of trade, but also equity market performance over the last few years. Figure 7 shows the underperformance of the resource equity sector against the broader ASX200 Index.

When assessing potential investment opportunities we look for companies that show operational efficiencies and good cost control, and operate from strong market positions as they deal with economic headwinds. They should also have the benefit of offering bonds in multiple offshore currencies, which may provide better liquidity. (See the case studies for examples of what we would consider when assessing a company.)

Accessing high quality Australian infrastructure assets which have monopolistic traits via publicly listed bond markets may be another potential source of attractive returns in Australia.

PIMCO believes accessing these assets through liquid, publicly traded bond markets is a better option than the Australian private loan market, which can be illiquid. Transurban is an example of an issuer with such traits that has been an issuer in the local Australian domestic bond market and that last year completed its inaugural euro-denominated issue. Other monopolistic infrastructure assets that have also issued bonds in the global, publicly traded markets are Sydney Airport and Melbourne Airport (Australia Pacific Airports).

Demand strong for high quality Australian credit

Investor demand for high quality Australian credit has been astounding over the last year. The global backdrop of a slower growth outlook, allowing developed-market central banks to maintain lower interest rates, supports the continued high demand for quality, income-producing assets among global investors. Domestically, many investors are likely reacting to the drop in interest rates on bank term deposits by seeking higher-income assets, such as credit securities.

From the companies’ and banks’ perspectives, issuing into domestic and global bond markets has become a funding option of choice, given investors’ hunt for yield in the low-rate environment. Just recently, the newly formed Scentre Property Group (the restructured Westfield Retail Trust) was able to successfully issue €2 billion ($A2.88bn) in bonds across several maturities, with reports of a staggering €5 billion in demand for the deal. It was the largest-ever European bond deal by an Australian company outside of banking and mining.

At PIMCO, our credit picks tend to be issuers in global funding markets that can provide offshore investors with diversification through high quality Australian credits. We draw on our network of credit portfolio managers and research analysts around the globe to select and gain exposure to high quality Australian credits.

In conclusion, the Australian economy is currently facing headwinds associated with a decline in the terms of trade. The challenge for credit investors is to find those companies that are able to navigate these headwinds competitively through superior operational efficiencies, cost control, strong market positioning and prudent balance sheet management. It is also important to find companies with a clear, demonstrated understanding of the macro environment in which their businesses are operating.

Somewhat mitigating the negative implications of a declining terms-of-trade environment is the current structural paradigm of lower interest rates globally, which has fueled demand for higher-yielding, high quality credit. The Australian corporate environment has proven to be supportive for these high quality credits and should continue to be, despite the macro headwinds.

That amounts to a declaration that the only Australian firms worth investing in are those operating outside of Australia!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.