Weeoo, weeoo, weeoo.

As I wrote my recession risks post this morning I did spare a thought for The Pascometer, which hasn’t fired off a counter-contrarian sell-signal in some time. But lo, here it is:

It sometimes seems capital investment commentary in Australia concentrates on mining and manufacturing, perhaps because they are industries with unhappy outlooks – bad news is good news.

The reality is that the game has moved on, that the non-resources sector is substantially larger than mining and that manufacturing is but a small part of that non-resources story.

So while the immediate headline for the June quarter private fixed capital investment statistics is that capex was “less worse” than expected, it missed the real story: the outlook for non-resources capex is positive.

…The good news is that the other selected industries’ CFOs are saying in their June quarter “estimate 3” that they’ll invest $55.7 billion this year, a hefty 12.2 per cent more than last year’s “estimate 3”.

The other selected industries’ step up from estimate 1 to 2 and from 2 to 3 are all nicely strong. Should the trend hold, we can reasonably expect this category to finish 2014-15 somewhere about the $65 billion mark. Add on capex in the manufacturing sector and there’s more than $73 billion in non-resources private fixed capital investment

…While it can be very hard for the individuals involved, the coverage given to the obvious occasional high-profile manufacturing job losses then is rather disproportional if the industry accounts for less than 4 per cent of new capex. That of course doesn’t stop politicians grandstanding about, say, 350 jobs to be shed at BlueScope in a national labour force of 12 million.

What’s more, like Australia’s unsung heroes in the services sector, non-resources investment is growing despite the headwind of a stubbornly strong Australian dollar. Like the Reserve Bank, we can only hope what might be achieved by the animal spirits if they finally get a currency tailwind.

Did anyone see headlines yesterday reporting terrible capex figures? No. That’s because the media focused entirely upon the unexpected rise in investment in the current quarter. There was no hand-wringing, bodice-ripping or teeth-gnashing. There was a happily bullish narrative all day thoroughly celebrating Australia service sector heroes.

This is the heart of mechanism, you see, a counter-contrarian array of cogs and gears that whirs into action whatever the context. It may be a deliberate defense of the confidence-dependent real estate economy, poor judgement, or something else, I don’t know. But it sure is ironic when it complains about the high dollar, given the mindless embrace of confidence over competitiveness – the core of Pasconomics – is the major reason the currency hasn’t fallen.

Anyway, I won’t complain too much. Today’s siren-sounding is confirmation that yesterday’s capex figures were, in fact, disappointing. Even the optimistic Paul Bloxham struggled to put lippy in the pig:

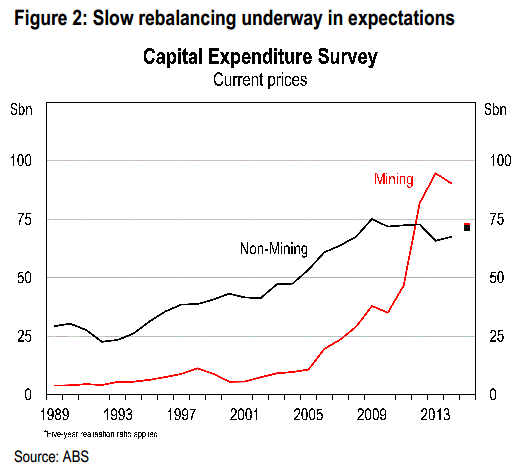

The second element of the survey is the forward-looking investment intentions component. Here the story is a little more positive as there are some signs that investment is rebalancing, although this process is slow. Applying a five-year realization ratio, as is a standard adjustment in this survey, suggests overall investment is expected to fall by -9% in 2014/15. As widely expected, mining investment is expected to fall by a sharp -20% next year, while manufacturing investment is expected to fall by -16%. However, firms in ‘other selected industries’ reported that they expect investment to rise by +9% next year. Indeed, adding up all of the non-mining industries suggests a +5% rise in investment in 2014/15. It is also worth keeping in mind that this survey does not cover all of the non-mining sectors of the economy and recent surveys of business conditions continue to show improvement. Of course, the current upswing in dwelling investment, not included in this survey, should also help to offset to fall in mining investment.

That is right. Too slow as the terms of trade come apart. Weeoo, weeoo, weeoo.