From NAB today comes the business survey, which is powering on headline numbers:

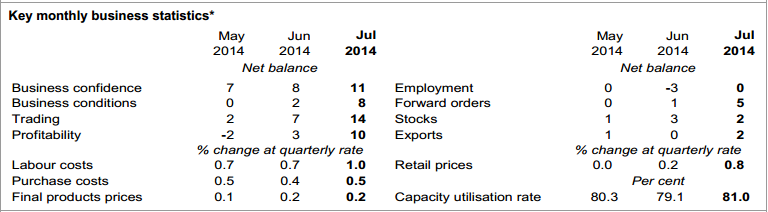

Business confidence again surprised on the upside, supported by better business conditions (largely reflecting sales and profits) and a surge in retailer confidence. Firms still unfazed about the Budget (for now). Conditions jumped to a four year high, but major improvements were narrowly based – with construction a standout. Employment improved modestly, but remains subdued. Stronger sales saw higher utilisation rates and positive capex. Forward orders suggest the better start to Q3 may continue. NAB forecasts softer in 2014/15, stronger on 2015/16. Unemployment rate on slightly higher track. Rates still on hold till late 2015 but risks of a cut rising.

Business confidence improved again in the month, reverting back to post-election highs. Firms still appear unfazed by the Federal government’s ‘tough budget’, possibly taking comfort in the bounce back in consumer confidence. A solid jump in business conditions and better forward orders is supporting the relatively optimistic position. Stronger sales and profits are driving the trend, but the recovery continues to be relatively jobless with the employment index seeing more moderate gains (remaining at subdued levels). Higher capacity utilisation rates suggest that the improvement is relatively capital intensive.

Business conditions rose in the month to their highest level since early-2010 – implying a strong start to Q3 demand. That said, much of the improvement is narrowly based. Construction surged again, propped up by high levels of building approvals that will drive construction activity for many months. Wholesale (a bellwether industry) also improved, but remains slightly negative – and are somewhat contrary to the kick up in forward orders. Changes in conditions varied across industries, as do the levels – construction and service industries are the stand out (mining and retail are weakest). In contrast to very strong readings for sales and profits, business is still very reluctant to employ.

Our wholesale leading indicator improved, but still suggests weak underlying conditions and below trend economic growth in the second quarter of 2014 – with moderate near term growth in prospect for demand.

Firms report moderate inflation pressures, although input cost prices accelerated. Both purchasing costs inflation and labour cost pressures lifted, but expected to be temporary. Retail inflation also accelerated.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.