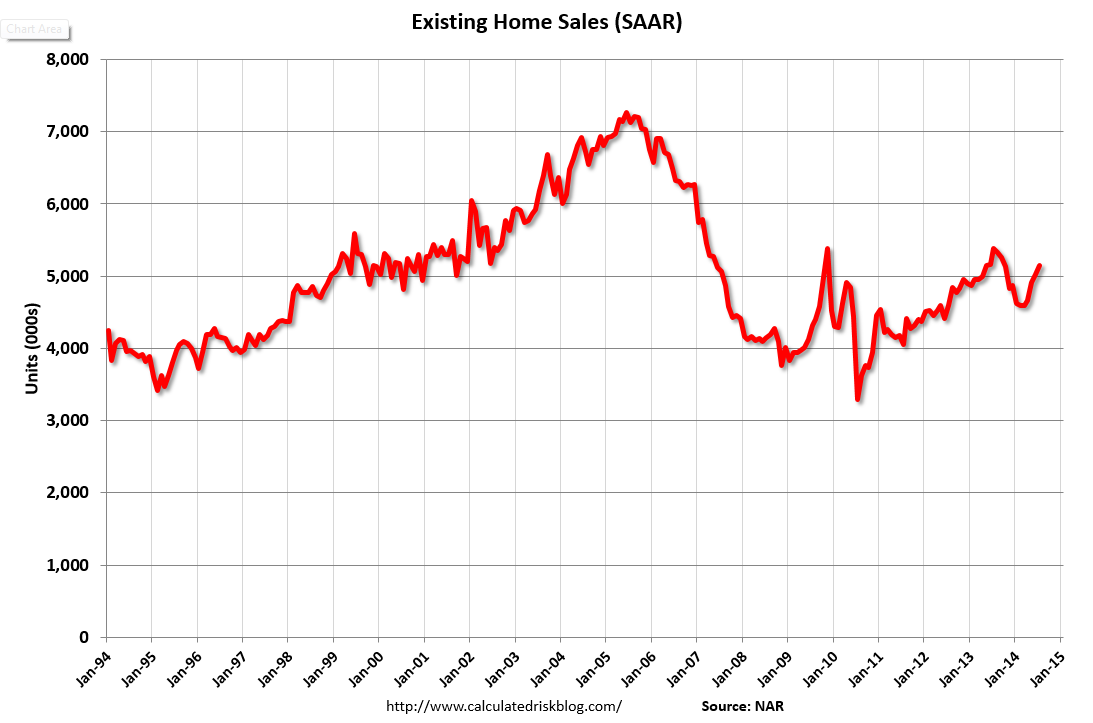

Not too hot to bring forward rate rises and not too cold to upset equity markets. That’s US data right now and overnight we got more of it. The NAR reported existing home sales and they were firm with rising inventories offsetting any price worries (all charts from Calculated Risk):

Total existing-home sales, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, rose 2.4 percent to a seasonally adjusted annual rate of 5.15 million in July from a slight downwardly-revised 5.03 million in June. Sales are at the highest pace of 2014 and have risen four consecutive months, but remain 4.3 percent below the 5.38 million-unit level from last July, which was the peak of 2013. …

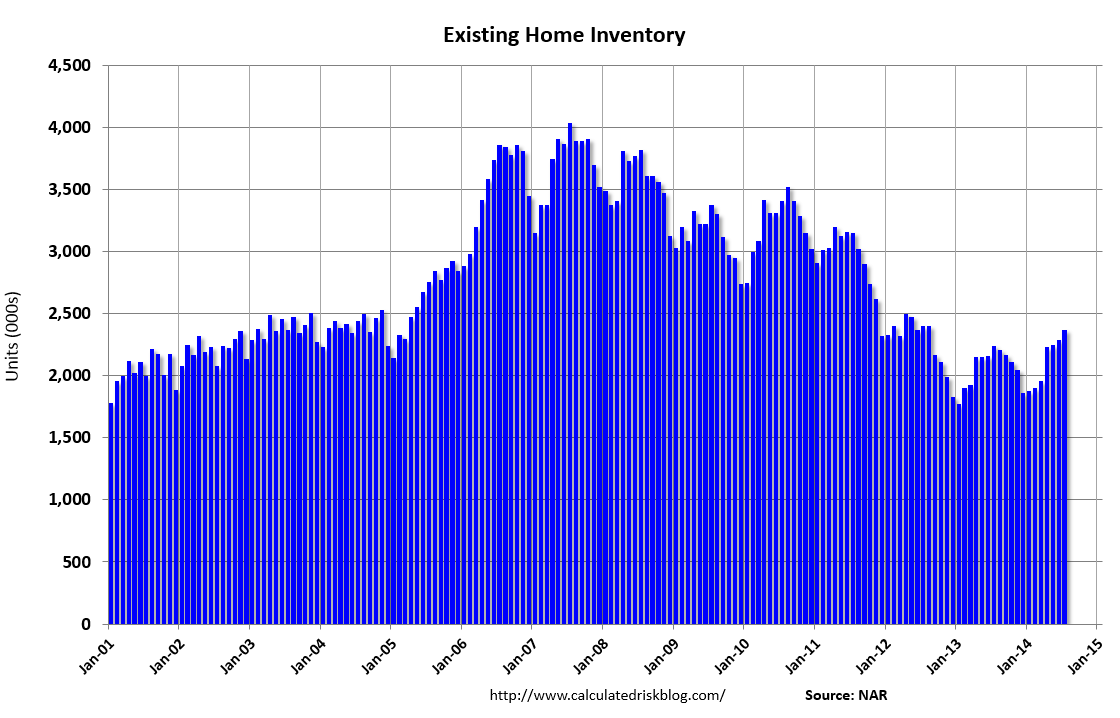

Total housing inventory at the end of July rose 3.5 percent to 2.37 million existing homes available for sale, which represents a 5.5-month supply at the current sales pace. Unsold inventory is 5.8 percent higher than a year ago, when there were 2.24 million existing homes available for sale.

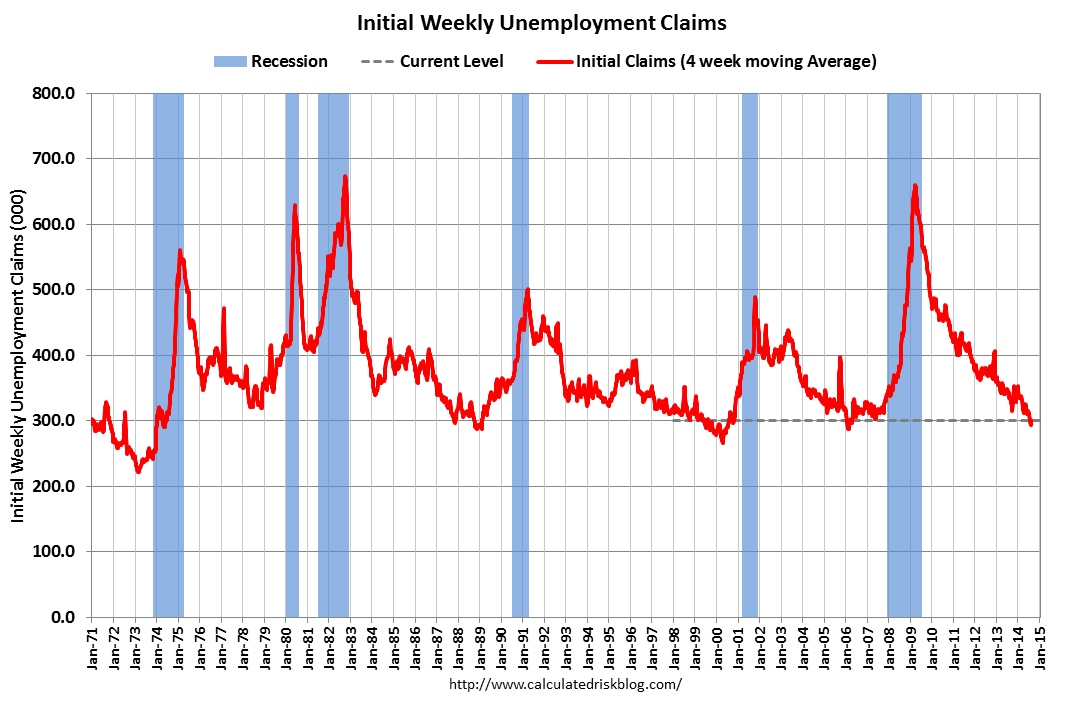

Weekly unemployment claims reversed last week’s big spike:

In the week ending August 16, the advance figure for seasonally adjusted initial claims was 298,000, a decrease of 14,000 from the previous week’s revised level. The previous week’s level was revised up by 1,000 from 311,000 to 312,000. The 4-week moving average was 300,750, an increase of 4,750 from the previous week’s revised average. The previous week’s average was revised up by 250 from 295,750 to 296,000.

There were no special factors impacting this week’s initial claims.

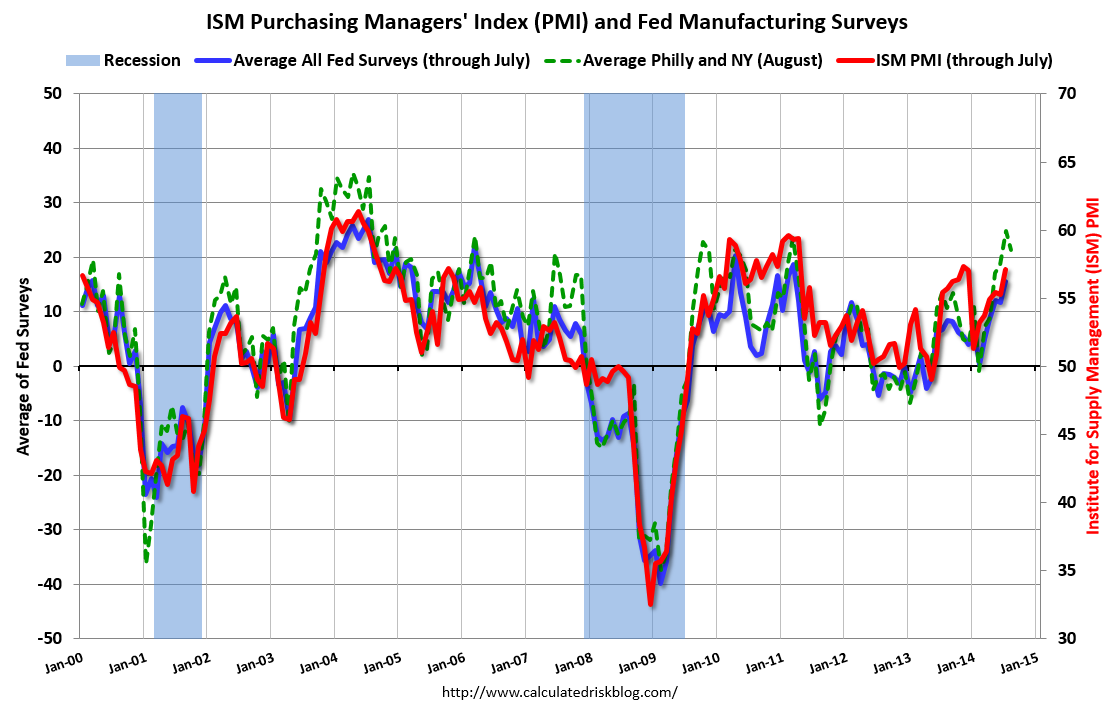

The Philly Fed manufacturing gauge launched to 28 and the Flash PMI jumped to 58. Both are setting up nicely for a ongoing strength in the ISM:

Advertisement

Markets loved it with equities at record highs and bonds rallying as well. The short end was stable while the long was bid up firmly. The US dollar took a breather, as did oil and gold. The Aussie recovered all of yesterday’s losses.

The US economy is traveling just right at between 2.5 and 3%. Tightening should begin mid next year. Q2 is an outside bet.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.