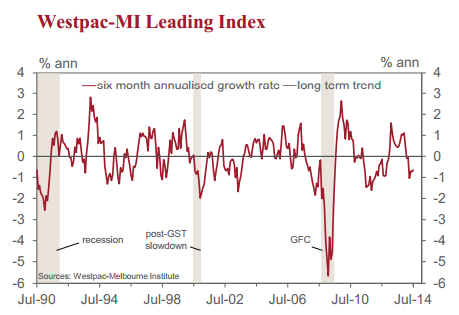

Although the deviation from trend narrowed a little the key message from the Index remains intact. This is the sixth straight month that the growth rate in the Index has been below trend.

The index continues to indicate that we can expect growth in the Australian economy to stay below trend in the second half of 2014 and into 2015.

That view is consistent with the revised forecasts recently released by the Reserve Bank of Australia in its August Statement on Monetary Policy. While the Bank forecasts using ranges, an analysis of the mid points of these ranges indicates that its forecasts imply that the growth ‘pace’ of the Australian economy is likely to have slowed to 2% (annualised) in the second half of 2014. It has also lowered its forecast (mid-point) for 2015 from 3.25% to a below trend 3%. Growth momentum in the first half of 2015 is forecast to lift from 2% to 3% below trend).

Westpac is more optimistic around the growth outlook than the Reserve Bank. Consistent with the signal from the Leading Index we expect below trend growth in the second half of 2014 but at a 2.75% annualised pace rather than the 2% implied by the Reserve Bank. In particular we are expecting the pace of consumer spending in the second half to lift from 2% (annualised) in the first half of 2014 to 3% in the second half. That more positive

consumer outlook is expected to strengthen further in the first half of 2015, reaching a 3.5% annualised pace. That is consistent with our slightly more upbeat view on the first half of 2015 than implied by the index. We expect that growth momentum in the economy can lift to an above trend 3.5% pace in the first half of 2015.

Over the last six months the index’s growth rate has remained at a below trend growth pace. However the components of the index which have been driving this below trend pace have changed. In February, when the Index’s growth rate was 0.09% below trend, the key drivers were: the Westpac –MI Consumer Sentiment Expectations index (–0.35ppts) and the Westpac MI Unemployment Expectations index (–0.24ppts). Offsetting

those negative effects were dwelling approvals (0.30ppts); US industrial production (0.21ppts) and the yield spread (0.12ppts). Commodity prices, the S&P/ASX200, and hours worked had limited impact on the growth rate.

The six month annualised deviation from trend growth rate of the Westpac Melbourne Institute Leading Index which indicates the likely pace of economic growth three to nine months into the future increased to –0.65% in July from –0.73% in June.

In July the growth rate in the Index has fallen further below trend to –0.65%. The major contributors are now: commodity prices(–0.69ppts); yield spread (–0.32ppts); aggregate hours worked (–0.17ppts). Offsetting those drags on growth are US industrial production (0.36ppts) and the S&P/ASX200 (0.18ppts). Overall though, the main drag on momentum has shifted from the consumer to commodity prices and the yield spread.

The changed contribution from the yield spread results from a flattening of the yield curve. A fall in long rates which is not matched by lower short rates indicates that the stance of monetary policy may have tightened. Of course the yield curve, in particular the long end of the curve, is capturing both domestic and international influences.

We do not expect to see the Reserve Bank changing rates anytime over the next year. Indeed, the Bank once again confirmed its intentions in its August board minutes for a period of stability in rates. Westpac expects that, with our expectation of a more favourable economic environment than is anticipated by the Reserve Bank, the next move in rates will be a tightening but not until the second half of 2015, with August currently pencilled in for the date of the first move.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.