Property launches in China are set to surge in the latter half of the year with developers sticking to their schedules despite mounting inventories, spelling double trouble for a market hammered by months of falling prices.

Prices started to decline in March as the slowing economy hit demand, inventories ballooned and developers began offering discounts. The current slump was confirmed by official data only around the middle of the year, way after developers had already committed themselves to completing projects for 2014.

Developers also have little choice but to heap even more supply in a bloated market due to regulations that stop them from sitting on undeveloped land. Those that fail to break ground on new projects a year after purchasing land will face fines, while those that wait more than two years could have their land confiscated.

The rush to expedite projects will worsen chronic oversupply that analysts warn may take years to clear. Unsold properties will also have broader implications – the sector accounts for over 15 per cent of the economy and its fortunes are tied to other industries such as concrete and steel.

…”Buyers’ attitude has changed. They feel they can wait,” said CIFI Holdings Chief Financial Officer Albert Yau.

Hmmm, that one slipped through the Gina screen. This is a disaster for iron ore in the making with residential construction accounting for one third or more of steel output.

The question is is the glut cyclical or structural? In my view it is more the latter than the former so we’re therefore on the verge of a plateau in Chinese steel production and falls if the shakeout turns disorderly, even though aggregate output will remain high.

Advertisement

Danske Bank has a note out today that examines this question and draws a glass-half-full conclusion versus my half empty one:

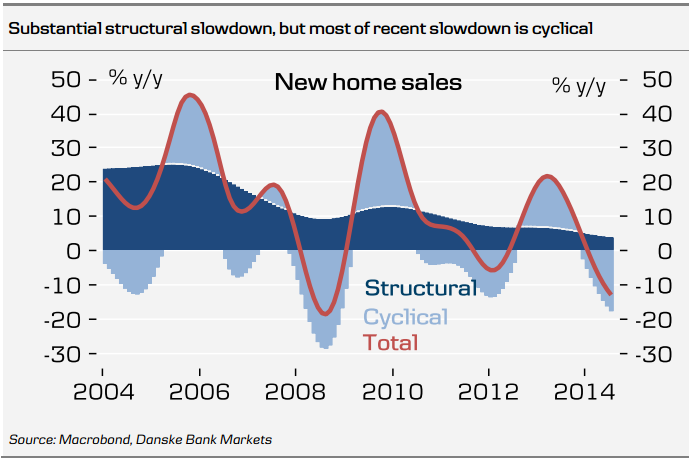

Since 2006 there has been a substantial slowdown in new home investments. Our calculations suggest that structural growth in new home investments could already have declined below 7%.

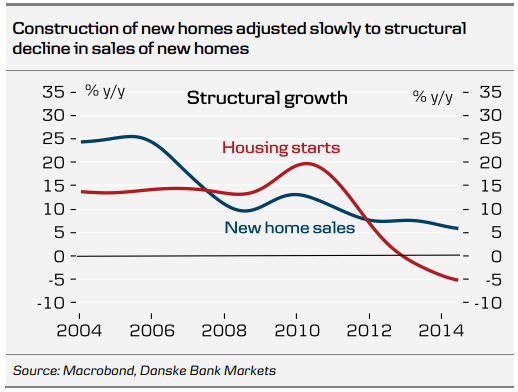

The structural slowdown mainly reflects that the pace of urbanisation has peaked in China. However, excess supply has also added to the structural slowdown as construction of new homes has been slow to respond to the structural slowdown in demand for new homes.

Nonetheless, at least 70% of the decline in new home investments over the past year appears to be cyclical and can largely be explained by tighter financial conditions.

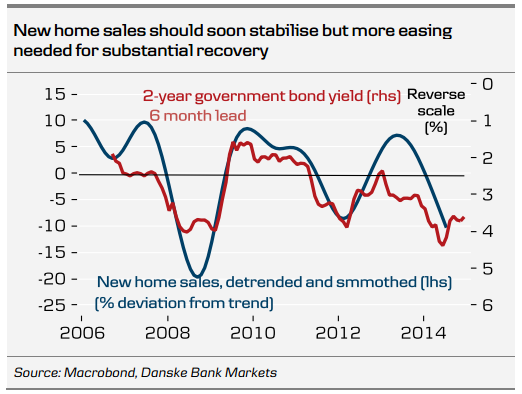

There should gradually be less headwind from the housing market in the coming quarters as financial conditions have so far eased in 2014.

However, the recovery will be weak as financial conditions have only eased slightly and the structural slowdown will continue to weigh on new home investments.

Despite the structural headwinds we still think an interest rate cut would be an effective tool to boost the housing market in China.

This is a nice piece of work, operating in the appropriate context. It’s good to see an acknowledgement that the “pace of urbanisaiton has peaked”. As I’ve explained many times to The Pascometer, it doesn’t matter if China builds Europe every year if the isn’t more than last year. It’s the rate of change that matters to growth and commodity prices amid a supply response.

Advertisement

I come down more bearish in the structure versus cycle split for one simple reason. In my experience “structural” of “underlying” housing demand is nearly always inflated during periods of strong price gains. When they end, and attitudes change (see above AFR story), some of that demand ends too and suddenly what looked like fundamental shortage or balance becomes excess.

The hope of a turnaround by year end looks quite forlorn given recent soft credit indicators.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.