Last night saw more Goldilocks US data. Case Shiller house prices are now rising at 6.2% in the 20 city index and will likely ease further into a soft landing. Durable goods orders went mad on a spike in aircraft orders for Boeing, up 22.6% in the month and roughly $50 billion above any previous peak! Conference Board consumer confidence rose to the highest since late 2007. Gold and oil were flat, the US dollar firmed a touch, short end bonds were flat and the long end sold off a little.

But all eyes are on the S&P500, which closed above 2000 points for the first time:

How high can it go is the question on everyone’s lips. Not much further, answers Capital Economics in a nicely concise note:

Advertisement

Although the S&P 500 has broken above 2,000 this week for the first time, we doubt that the stock market will go from strength to strength. For now, we are sticking with our forecast that the index will end next year roughly where it is now.

Clearly, much is likely to depend on the stance of US monetary policy. Janet Yellen’s comments at Jackson Hole have cemented investors’ expectations that the FOMC will only raise rates very slowly given lingering uncertainty about the amount of slack in the labour market. However, we think the Committee is likely to move a little sooner and more aggressively than generally anticipated.

There will not necessarily be a major correction in the stock market if we are right. After all, the market has tended to shrug off both the prospect, and the onset, of higher interest rates in the past. The S&P 500 rose by an average of nearly 5% in the six months before the first rate hike in each of the last seven major tightening cycles. (Our view is that the first hike in the next cycle is nearly six months away.) And it also gained an average of about 5% in the nine months after the first hike. (This augurs well for the period between March 2015 and the end of next year.)

What’s more, the price of equity is currently much lower than the price of debt, which suggests that bond yields could increase quite significantly in response to higher interest rates without making the stock market appear expensive in relative terms.

However, none of these seven cycles featured large-scale asset purchases by the Fed, which are due to be phased out soon. These have given equity prices a big boost in recent years via portfolio rebalancing. As a result, the valuation of the S&P 500 is now more stretched than it was when the Fed first raised rates in most of these prior cycles. The only notable exception was in 1999/2000, when tighter monetary policy was soon followed by the bursting of the dot com bubble.

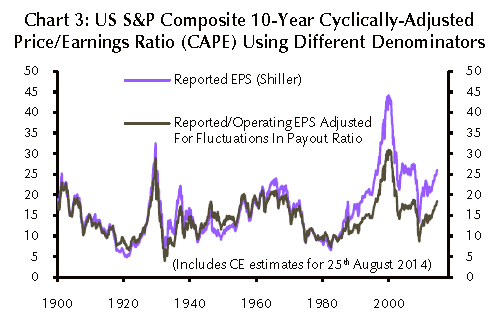

Granted, the cyclically-adjusted price/earnings ratio (CAPE) of the S&P 500 is nowhere near as high as it was at the turn of the century, especially when distortions to earnings and corporate payout policy are taken into account. But it is still about one third higher than its long-run average once these distortions are eliminated. So even if the equilibrium level of the CAPE today is a little higher than the long-run average, it is hard to make the case that equities are attractively valued in their own right.

The big risk remains a repeat of higher bond yields. Contrary to the CE view, I reckon any reasonable spike will immediately pressure equities, a la “taper tantrum”. But why would they spike? The Fed is not going to get ahead of markets on its rate hikes and, ironically, that’s the only reason that it should. There’s nothing in the real economy to threaten the inflation target with labour markets still soft internally despite good headline readings, commodity prices falling and the USD is rising.

Meanwhile, with Japan and increasingly Europe and China embarked on various forms of QE, there’s plenty of money to recycle into Treasuries and ride a higher US dollar. The bubble in markets is the only reason to hike rates and it will be ignored.

Advertisement

The US has entered a Goldilocks period of semi-stagnated growth that suits equities perfectly. So long China doesn’t lose control of its housing shakeout, new bubble highs could persist for much longer than most think.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.