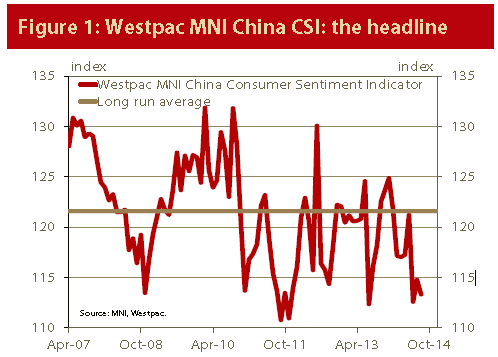

The Westpac MNI China Consumer Sentiment Indicator, hereafter the Westpac MNI China CSI, fell modestly to 113.3 in August from 114.8 in July, a –1.3% change over the month and –2.4% over the year. The August outcome is 6.8% below the long run average. The survey indicates that the anxieties gnawing away at the Chinese consumer through the first half of the year remain in evidence, and have arguably strengthened.

We noted at the time of the July release that a head-to-head comparison with the manufacturing surveys implied that households were less impressed with the state of the economy than the industrial sector. Taking into account the much softer than expected round of official July data that followed, and the weaker flash PMI for the month of August, it seems that the instinctive scepticism of the consumer was closer to the mark than industry’s relative optimism.

Three of the five components of the Westpac MNI China CSI declined from the previous month, with the exceptions being ‘business conditions one year ahead’ and ‘time to buy a major household item’. Current and expected family finances both declined, by 3.6% and 2.8% respectively, reflecting ongoing concerns regarding the outlook for jobs. ‘Business conditions five years ahead’ gave back a little of their July bounce, but remain well above their June trough.

The employment indicator continues to track at levels associated with policy easing in previous cycles. A further decline in August from the already depressed July reading implies that it would be most unwise for the authorities to declare victory too early on the growth front: particularly as the official CPI target of 3½% for 2014 seems unlikely to come under any threat, with inflation expectations still below their long run average.

The consumers’ confident attitude towards real estate in the first half of the year, which was in stark contrast to the gathering evidence of a deepening market correction, is beginning to fray at the edges. A less positive appraisal of theasset class shows up consistently across price expectations, ‘time to buy’, and the relevant questions on savings preferencesand motivations. In particular, ‘good time to buy a house’ fell below the long run average in August. The last time a sustained run of readings of this nature occurred was in 2011/12, a period when price declines were broad based across the country.

Notwithstanding all of the above, in absolute terms consumers are still reporting house price expectations that are above the long run average, which is an expression of collective faith that easier policy will eventually carry the day, even if the short term situation looks increasingly shaky.

From a balance sheet perspective, the risk appetite of consumers vis-à-vis their preferred asset classes increased marginally over July, with WMPs gaining share at the expense of bank deposits, but in absolute terms households continue to deploy their savings very conservatively (see page 4). Short term expectations for stock prices firmed for a second month.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.