Cross-posed from Investing in Chinese Stocks.

From 21st Century Business Herald. A failed real estate project in Anhui has left behind more than ¥10 billion in debt with multiple trusts exposed. Creditors are already taking legal action to secure their rights after the developer declared bankruptcy. At one point another firm was prepared to step in and take over, but it could not determine the company’s liabilities and backed out. Now begins the court’s take of unraveling who owes what to whom.

Based on the stories in the Chinese financial media, the trust industry is already in crisis, from Caixin:

The country’s formerly booming trust investment industry might have reached what one observer called “a tipping point,” as growth plateaus and risk gets more attention.

Recent data from the China Trustee Association shows the industry shrunk in June, the first monthly decline since it took off in China in 2008. As of June 30, the assets of all 68 trust companies in the country stood at 12.48 trillion yuan, down 0.24 trillion yuan from the end of May.

The assets increased by 46 percent last year compared with 2012, which marked the end of a string of four years that saw annual growth rate of higher than 50 percent.

That’s a major deceleration. From 50% growth to contraction in a little over a year:

Forty-three companies submitted their reports in July and the results show that their combined risk assets – investments at risk, including but are not limited to bad assets where the borrower has failed to make repayments on time – have exceeded 70 billion yuan.

Of that, 50 billion yuan worth of assets were at high risk, meaning their underlying assets were illiquid or not worth as much as the investment.

Citic Trust, Huarong International Trust and New China Trust reported an amount of risk assets that exceeded net assets at times during the past several months.

Does the ¥70 billion figure include the ¥10 billion project that failed in Anhui? Losses could pile up very quickly if the economy slows further. Remember that when comparing the state of things to the world’s last big real estate shakeout in the United States, Chinese “sub-prime” are the developers that borrowed madly from shadow banks during the building boom, and the “toxic assets” are the trusts that now house those loans.

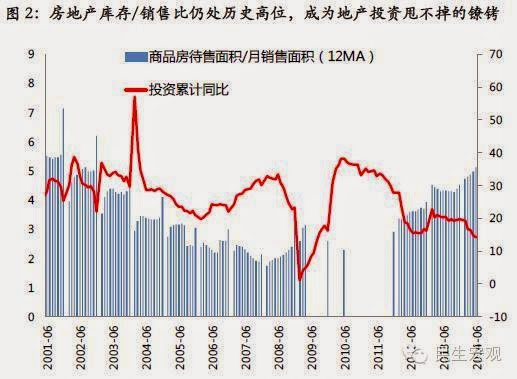

Meanwhile, Minsheng Securities has issued a report that illustrates the state of the developer market:

1. Can the real estate market stabilize? Property market slowdown worse than in 2011 and 2008. Included are the following two charts. The first shows inventory in blue bars (floor space for sale divided by 12-month average sales) versus cumulative real estate investment. The second shows developer capital (blue bars) versus average mortgage rates.

2. Can infrastructure investment continue to grow rapidly? Here is a chart of government land sale revenue (blue) and planned sales (red). Land sales fund infrastructure development at the local level.

3. Can the micro-stimulus be repeated? This was a concern of mine since it was reported that some governments started projects in Q2 instead of later this year, pulling forward spending. This chart shows the surplus money from the first half (blue bar). There is not enough money to repeat the micro stimulus in Q3 and Q4, assuming credit doesn’t ease.

4. Can Chinese exports recover?

Chinese Containerized Freight Index (CCFI) and Baltic Dri Index (BDI). Minsheng does not see export growth continuing due to rising costs and weak growth in developed markets.