Via FTAlphaville comes a question MB has asked many times. From UBS:

To an extent, this gradual transition has already started, albeit at a very incremental pace. In the past few years, consumption has contributed more to GDP growth than investment, thanks in part to slower credit growth and cooler investment in both infrastructure and property. The official (under-estimated) consumption share of GDP has risen since 2011 to almost 50% last year, recovering to its pre-global financial crisis level and putting a stop to almost a full decade of decline. Of course, given that overall economic growth has slowed from the pre-GFC double-digit pace to the current 7-8%, consumption growth has also slowed.

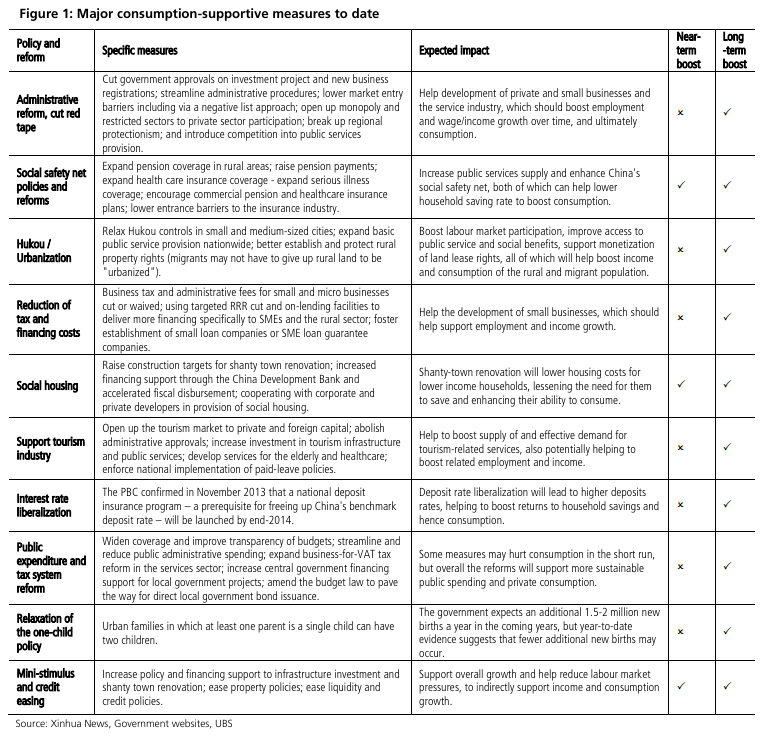

True, government mini-stimulus in 2014 has focused more on investment, but some stimulus measures are similarly supportive of consumption. Moreover, ongoing reforms are aiming to rebalance the economy over the medium term, by encouraging job creation, supporting income growth, enhancing China’s social safety net and increasing the supply of consumer goods and services where shortages and bottlenecks exist (see Figure 1 for more details).

However, from J Capital:

Advertisement

Consumer spending is second only to unemployment as the most atrociously tracked statistic in the economy, and the NBS numbers offer little insight. We have, however, been choosing two smaller cities per month as focuses of research, conducting interviews with vendors across commercial categories and triangulating the interview data with what we can see from the statistics. In each case, cities that have seen a decline in property sales almost immediately see a decline in spending in the industries we survey, with the sharpest downturns generally in property-related categories such as furniture and building materials. Next-weakest are usually consumer electronics and white goods, then food, while there is often growth left in clothing and personal care. The near identity between property and the consumer economy indicates that a slump in property must lead to a spike in investment in order to buoy the preferred areas.

The consumer segment, to the extent that it can be independently tracked, provides a clear trace for how capital moves through the economy at large and spills out in the form of commissions and kickbacks on contracts, higher compensation locally, and better liquidity for the housing market, leading individuals to spend.

…Just as Americans took out home equity loans and spent the proceeds, so Chinese have borrowed for years into the future; the difference is only that governments rather than households led the binge and guided a lions’s share of the proceeds into the hands of party and government officials, but also a portion of the proceeds into the hands of urban residents.

Now, the decline in spending we are seeing in each of the cities we survey is going hand in hand with the reduction in investment in new property. Absent a miraculous new source of fast wealth, there is no reason why consumption should not return to the pre-boom level, where it was in about 2006. The land-driven bonanza is over.

And so, growth will fall, except to the extent that clever policy boosts household income.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.