Yesterday, numerous people attempted to convince me that a 12yr high in unemployment is a “good thing” because it will lead to interest rates staying at historic lows. Yes, interest rates will stay at historic lows, but I can assure you there is absolutely NOTHING GOOD about a 12yr high in the unemployment rate. Interest rates are at historic lows because economic growth is below par. Simple. Households will now be even more worried about job security. Simple. Earnings growth will be even harder to generate. Simple. Credit growth will remain weak. Simple.

I believe there is only one strategic and tactical response required to the 12yr high in unemployment. This morning I am downgrading the Australian Bank Sector to UNDERWEIGHT.

In my opinion equity risk premium, in the form of lower P/E’s (higher prospective dividend yields) will be priced into the Australian banks to reflect both rising unemployment, slowing GDP growth, weak credit growth, rising disruptive risk (peer to peer lenders, supermarkets entering banking) and rising regulatory risk (capital ratios, trading revenue). Under that macro overlay I can see NO scenario where Australian Banks outperform the broader equity market.

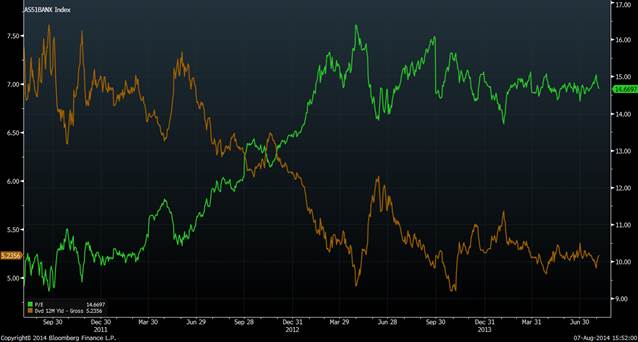

As I have been writing, the Australian banks have never been more owned by Australians. Foreign investors simply can’t come at the P/E’s or price to book multiples, multiples that are an inverse factor of the value of franking credits to domestic investors. What I believe comes next is Australian investors lock in some of the multi-year gains in Australian banks, particularly those who are using leverage to invest in Australian banks. Below is a chart of the P/E and dividend yield of the ASX200 Bank Index over the last 3 years. Yields have dropped from 7% to 5% and P/E expanded from 10x to 14.6x.

In April I downgraded the bank sector to “neutral” when my long held bullish 5.00%ff FY14 yield targets were hit/exceeded. Today I am downgrading to UNDERWEIGHT because I simply can’t see how the sector could outperform from here, feeling 6.00%ff FY15 yield based share price targets are more appropriate and banks are going to trade a little more like low growth utilities from here.

To put that in context, below is a chart of the ASX Banks Index (XXJ) vs the ASX200 Index (XJO) over the last few years. This outperformance is stunning considering the big 4 banks alone represent 30% of the benchmark index themselves.

XXJ vs XJO: common performance base

I believe this relative outperformance gap will start to narrow. This thinking is in line with my overall equity strategy of focusing on multi-year laggards and genuine growth stocks from this point.

Interesting, while big 4 Australian Banks are 30% of the ASX200, in my view some SMSF’s have over 50% of their money in Australian banks. There is a monumental private investor overweight in Australian banks and my point today is I simply don’t think that bet will work, in terms of generating relative outperformance, from this point. In fact, I think it will generate relative underperformance that is why I am moving to an UNDERWEIGHT recommendation this morning.

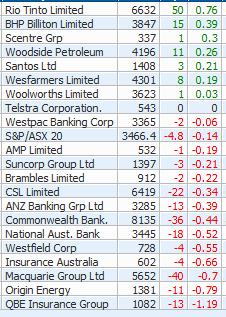

And it seems I wasn’t alone in thinking this way after the unemployment print yesterday. Below is the performance of the ASX20 Leaders Index, which represents 80% of the ASX200 Index. It clearly shows you that the big 4 banks were used as rotational funding vehicles to big resources and the two supermarket operators. In fact, we may be seeing the infancy of a relative rotation back to big resources from big banks.

Just to remind you of that relative relationship over the last few years, below is a chart of the ASX200 Banks Index (XXJ) vs the ASX200 Resources Index (XJR).

The chart above is trying to tell you that any profits taken/underweights initiated in the banking sector should be rotated to big cap resources as all things China facing turn up.

Hmmm, well, I agree on banks, largely for the same reasons that I think now is the time to sell housing: the cycle is getting old. But I can’t see all things China turning up, especially not resources, notwithstanding the fact that any insto rotation could support them longer than they deserve.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.