Deloitte Access Economics today released a high caliber report modelling different gas price scenarios for gas-consuming sectors if nothing is done to prevent price rises. The conclusions are stark:

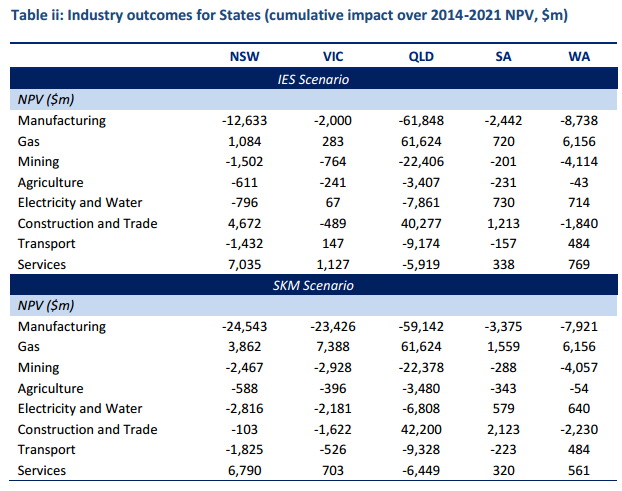

LNG developments on the East Coast wil create a new export industry involving signifcant production, employment and capital investment. However, gas market transformations on both the East and West Coasts wil also have adverse consequences. Table i shows the impact to industry output (equivalent to sales and services income) for al sectors in the veconomy in the years 2015, 2018 and 2021 and cumulatively over the period 2014-2021.

‘SKM Scenario’ asumes some market power. Both are compared to baseline scenarios in which Eastern LNG does not develop and the NWS recontracts to domestic customers in the West.

In each of the snap-shot years (2015, 2018 and 2021), with the exception of gas, services and the construction sector (which receives a boost through its role in suporting LNG developments), gas price increases and other drivers translate into a reduction in industry output for all other sectors in the economy compared to a baseline scenario. Similarly, over the period 2014-2021, al industries except the gas, construction and services experience a cumulative reduction in industry output (as measured by the net present value of the total year on year output reductions during the period). Output equates to gros income for the sectors concerned, and is distinct from Gross Domestic Product.

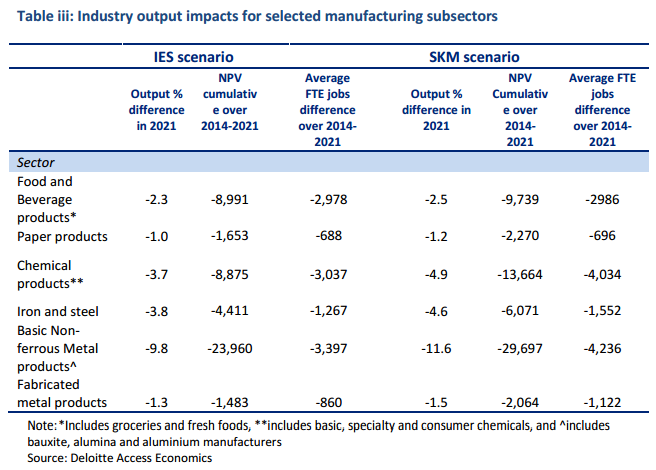

The manufacturing sector is projected to experience the greatest reduction in industry output. This is primarily due to its signifcant gas usage and high trade exposure, which largely limits the sector’s abilty to pas on higher gas input costs. In 2021, the final year modeled, manufacturing output is projected to be 3.6% (IES) to 4.4% (SKM) lower than in the baseline scenario. The net present value of the cumulative reduction in manufacturing output from 2014 to 2020 is around $8 bilion under the IES gas price projections, and $120 bilion under SKM gas price projections.

This is partial analysis that does not examine the overall impact of gas price rises for the economy. It was commissioned by gas-consuming lobby groups and only covers their losses not other’s gains.

It does, however, offer some unique insights into the magnitude of those losses under various pricing scenarios which is useful in a policy sense. And here they are:

Advertisement

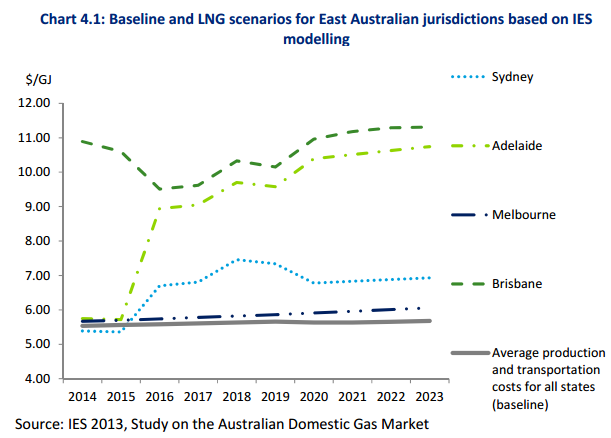

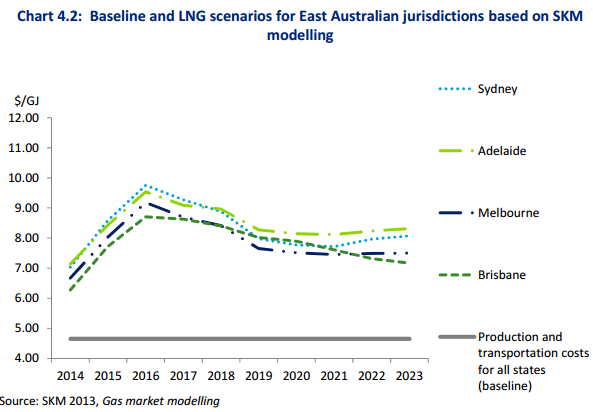

The two scenarios are based upon pre-existing gas price modelling. Here is how Deloitte describes it:

The IES modeling estimates price impacts associated with the link to international LNG markets under the assumption that the market is perfectly competitive and offers little opportunity to exert market power.

In contrast, the SKM modeling estimates price impacts under the assumption that gas producers and shippers are able to exert market power.

Advertisement

Deloitte agrees with SKM modelling (so do I) which shows an export net back price that spikes and then falls to an equilibrium at $7-8Gigajoule (mmBtu) is 95% equivalent. That equates to a North Asian price around $11-12. If the LNG contract system breaks down, no Australian LNG projects will make money at that price but that’s different story, it is the pricing range we’re headed for by 2018.

The study does not try to propose a way out but it’s guidance for gas prices is solid and the resulting damage to gas-consuming business is useful. The impact on employment, however, will not excite either the commissioning lobby groups or policy-makers:

Advertisement

14,626 jobs is roughly half of the expected job losses from the closure of the car manufacturers and parts suppliers. In both cases these are direct jobs, not accounting for spillovers, which would probably multiply the figure by a factor of two or three.

Even so, the lobbies that commissioned the report won’t be pleased. It’s not the kind of blockbusting figure to get anyone excited.

That is not to say that the decline of manufacturing should not addressed. Of course it should, on every front, and failing to do it with each cut of Dutch disease only ensures its accumulated doom.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.