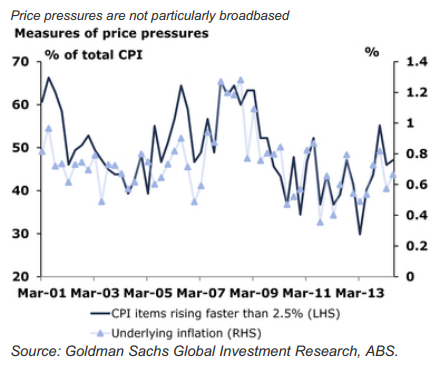

Although annual headline inflation is now at the top of the RBA’s target band, the pace of inflation has decelerated materially over the past 3 quarters and even without the removal of the carbon tax annual inflation looks set to decline sharply in 3Q14 as the 1.2% qoq in 3Q13 falls out of the annual calculation. With the removal of the carbon tax likely to take approximately 0.7% from inflation in the coming quarters, headline inflation is set to decline rapidly over the coming 12 months. Moreover, it is worth noting that the increase in tobacco taxes provided the 3rd highest contribution to inflation in the quarter, an effect which will also dissipate in the coming quarters. Importantly, measures of inflation dispersion remained benign in the quarter with well under 50% of items in the basket of underlying CPI rising by less than the mid-point of the RBA target band. Together with a higher A$, which will suppress tradable goods inflation, subdued wage pressure, declining upstream commodity prices, well anchored inflation expectations, and ongoing evidence of an easing in private sector non-tradable inflation, it is clear that ex tax increases inflationary pressures remain benign in Australia. The August Statement of Monetary Policy now looms large as the forum for the RBA to lower its inflation forecasts post the removal of the carbon tax, which in concert with insipid domestic demand growth, can be expected to see the RBA declare that the top of the inflation cycle has passed and a period of inflation closer to the bottom of its target band is in prospect in the year ahead. We retain our view that the RBA will look to ease interest rates in 2014, most likely in September.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.