The annual Newport Consulting mining outlook study is out and is sickly reading.

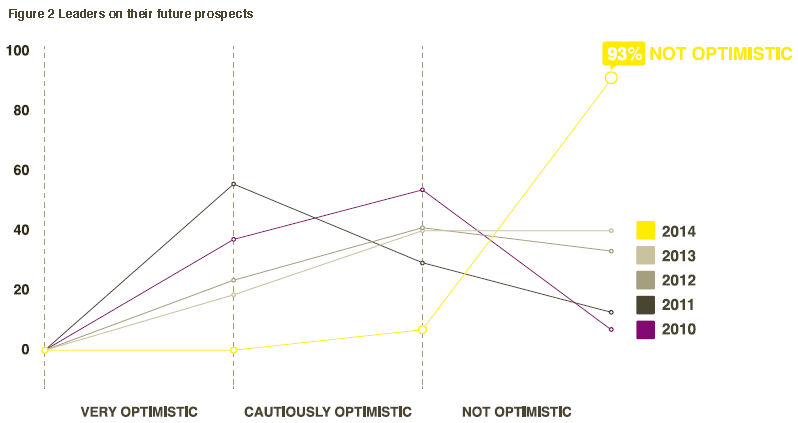

Future outlook reaches a new five-year low.

An overwhelming 93 percent of mining leaders in this year’s report were not optimistic about their growth prospects for the next 12 months – up by more than 50 percent compared to last year. Most hold low hopes of the sector resuming large-scale projects in the next 12 month, and only 7 percent believe they will see some large-scale projects return during this time.

New federal government embraced, but industry wants more action.

A sizeable 70 percent of mining leaders had anticipated major changes to the sector in the new government’s first year, but say that they have not seen adequate action yet or election promises delivered on. The sector is calling for more assistance with industrial relations laws, and a fast-tracking of the promised infrastructure investments that hold the key to economic growth.

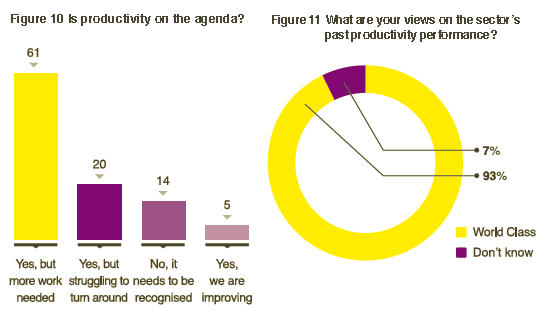

Knee-jerk cost-cutting reactions are hampering productivity.

A trend was observed this year of mining companies equating better operations with cost-cutting, evident in the number of retrenchments made over the last 18 months. The mining sector shed 26,000 jobs between May 2012 and the end of June 2013, and is likely to lose more in the coming year. Investment is also down. Both factors are likely to place enormous economic stress on the regional towns where mines close.

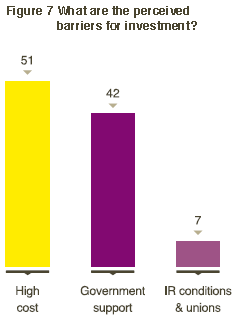

Investment inhibited due to high business costs and a tough regulatory environment.

Our mining leaders spoke at length of the high costs of doing business, especially wages and energy, plus the negative effects following six years of an anti-mining government. They criticised the arduous process of getting developments approved, and government regulations that make new mining projects difficult to start.

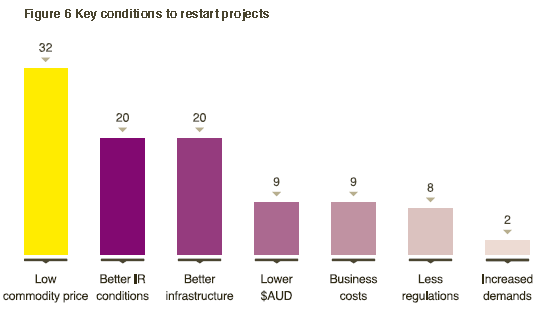

Low commodity prices and falling demand are the largest concerns for mining leaders.

Tough and volatile market conditions continue to drive the gloomy outlook of mining leaders, with 68 percent citing this as their main concern. A further one-quarter of respondents were concerned most by falling demand in key markets such as China. Meanwhile, demand from other markets remains hampered due to the Australian dollar’s high price in comparison to the currencies of other resource producers such as Brazil and South Africa.

Saul Eslake appears with a guest interview:

How has the end of the mining boom contributed to the current state of Australia’s economy?

As the investment phase of the mining boom draws to a close, and commodity prices continue to decline following their peak three years ago, this is the first commodities boom in Australia’s history that hasn’t ended in double-digit inflation followed by recession. This fact is probably under-appreciated.

This unprecedented ending is a tribute to three great reforms of the 1980s and 1990s: the floating of the exchange rate, the creation of an independent central bank, and the decentralisation of Australia’s wage-fixing system. It makes for a vastly better outcome than might be expected, despite the below‑trend rate of mining investment (which peaked as a share of GDP in the first half of 2013), and the upwards creep of unemployment.

Other factors have also contributed to Australia’s economic performance during this period. These include the patchy recoveries in the major advanced economies, the slowing in the more important emerging economies (in particular China), the maintenance of unorthodox monetary policies (zero interest rates and quantitative easing) in the major advanced economies, the persistent strength of the Aussie dollar in the face of falling commodity prices, and declining Australian interest rates.

What is the outlook for the next 12 months?

I agree entirely with the RBA’s and Treasury’s assessment that overall economic growth is likely to continue at a below-trend pace over the next 12 months, and that the unemployment rate will continue to edge upwards.

Do you see confidence in large scale mining projects returning?

I don’t expect any major new mining projects to commence in the next few years. That’s partly because there is now a fairly wide consensus that commodity prices will continue to decline as more supply comes on stream globally, while the growth rate of global demand for most commodities continues to slow.

It also reflects the fact that Australia has become a relatively high-cost location for resources projects. Aside from a recent wages slowdown, wages and other costs including energy have generally risen over the past decade. Meanwhile, the Australian dollar remains strong while other resources‑based currencies (such as the Brazilian real, South African rand and Indonesian rupiah) have declined. I don’t think this is likely to change in the next 12 months.

Outside of the mining sector, confidence remains below average, and the brief improvement associated with last year’s change of government appears to have evaporated.

Exactly right, Mr Eslake. This means the following:

Advertisement

the mining capex cliff will be as large as it can be with a high probability that it will overshoot estimates to the downside by 2017. Australian growth will remain sub-trend, and

cost-out deflation is the new normal for mining. The super-cycle is going to be followed by a decade long period of efficiency drives and reducing head counts. Productivity is going to rise and employment fall, a lot.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.