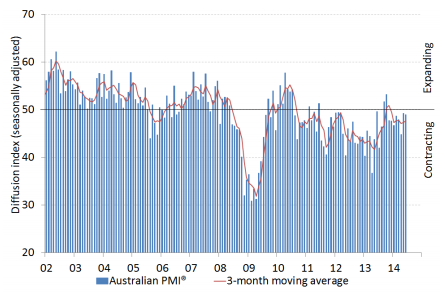

The latest Australian manufacturing PMI is out and nations around the world enjoy bounces- from China to the US – ours sags endlessly on:

The latest Australian Industry Group Australian Performance of Manufacturing Index (Australian PMI® ) remained in contraction for an eighth consecutive month in June. It moved down very slightly, by 0.3 points, to 48.9 points (seasonally adjusted). Readings below 50points in the Australian PMI® indicate contraction. The three-month-moving-average Australian PMI® was broadly unchanged in June, at 47.6 points, indicating mild contraction.

This month, many respondents to the Australian PMI® cited concerns about the renewed strength of the Australian dollar, which has increased import competition and lowered demand for locally made products. This has most strongly affected businesses in the metal products, machinery and equipment, and petroleum, coal, chemicals and rubber products sub-sectors. Although the Australian dollar is currently lower than the levels seen between 2011 and 2012, it has appreciated by around 8.5% since February this year and is sitting around US$0.94.

Across the eight manufacturing sub-sectors in the Australian PMI®, only the large food and beverages (52.5 points) and the smaller wood and paper products (54.2 points) sub-sectors expanded in June. The metal products, machinery and equipment, and petroleum, coal, chemicals and rubber products sub-sectors all contracted this month (i.e. below 50 points).

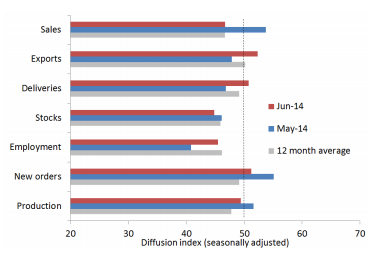

Both the production and sales sub-indexes declined into contraction June, following a brief expansion in May. Manufacturing employment contracted at a slower pace in June. More positively for the outlook, the new orders sub-index of the Australian PMI® stayed above 50 points this month (i.e. expansion). Conditions improved for manufacturing exports in June, despite the high dollar, but this month’s expansion in exports was limited to the food, beverages and tobacco sub-sector and a handful of businesses in other sub-sectors.

Internals are probably weaker than the headline with deliveries and employment offsetting second derivative falls in new orders and production:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.