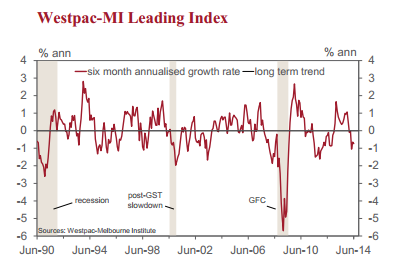

The six month annualised growth rate of the Index has now been growing below trend since February. It is indicating that growth in the Australian economy can be expected to remain below trend for the remainder of 2014 with limited momentum into 2015. The latest read on Australia’s growth rate was a 1.1% for the March quarter and 3.5% for the year, comfortably above trend. However, growth benefitted from a strong lift in resources exports in the March quarter associated with the rising capacity and favourable weather conditions. Domestic demand grew by a disappointing 1.6% over the same period. When there is a large discrepancy between GDP and domestic demand largely due to weather events then the Index will provide a more reliable guide to domestic demand.

Over the second half of 2014 Westpac is expecting GDP to grow at a 2.8% annualised pace while domestic demand is expected to grow at a 1.6% pace – still well below trend.

The first half of 2015 is expected to show GDP growing at an, above trend, 3.4% pace with the pace of domestic demand picking up to 2.3%. This modest lift in domestic demand growth will belie solid improvements in non-mining investment; housing; and consumer spending while the slowdown in mining investment will still act as a considerable drag on growth. Resource export growth, albeit at a more moderate pace, will continue to explain

the large gap between domestic demand and GDP growth.

Overall, Westpac expects GDP growth at 3.1% in both 2014 and 2015. However we do expect a lift in the pace of domestic demand growth from 1.4% in 2014 to 1.9% in 2015.

Over the course of the last six months the growth rate in the Index has fallen from 0.51ppts above trend to 0.73ppts below trend. Over this period the Index has been marked by a consistent drag from the Westpac-MI Consumer Sentiment (Expectations) Index although over the last six months this drag has not increased. The major explanations for the 1.24ppt deterioration in the growth rate in the first half of the year have been: commodity prices (–0.63 ppts); the yield spread (–0.54ppts) and dwelling approvals (–0.34ppts).

Note that yield spreads are commonly used in Leading Indexes. The theory is that if rates at the long end rise more than rates at the short end of the curve then markets are perceiving that the policy stance is more accommodative with growth prospects positive. If, as has been the case in Australia, long end rates fall more than short end rates, policy is assessed to be a more constraining influence on growth.

Partially offsetting these drags on the Index has been aggregate monthly hours worked (+0.20ppts). Notably, there has been no significant change in the Westpac-MI Unemployment Expectations Index, indicating that recent stability in the labour market has been a mild positive for the Index growth rate over the last few months.

The other components in the Index made a minor contribution to movements in the growth rate (ASX200 –0.04ppts and US industrial production +0.05ppts).

Over the month the level of the Index rose from 98.13 to 98.20. Movements of the components of the Index were: ASX200 (–1.77%); commodity prices (–2.82%); yield spread (–0.08ppts); Westpac–MI Consumer Sentiment Expectations Index (+3.81%); US industrial production (+0.17%); dwelling approvals (+9.87%); aggregate hours worked (+0.93%) and Westpac-MI Unemployment Expectations Index (–0.28%).

The Reserve Bank Board next meets on August 5. The minutes from the July Board meeting confirmed that the RBA continues to expect to hold rates steady. That seems to be the most prudent approach. Certainly the Leading Index is not indicating an imminent period of growth that might force the Bank’s hand to raise rates. The real issue is around how long this recent shock to confidence from the May Federal Budget will constrain the consumer. We expect that through the remainder of the year the consumer will begin a steady lift in confidence and activity as concerns around the Budget dissipate.

Such a scenario points to at least another year of steady rates. We do not expect to see a rate hike until August next year.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.