The Melbourne Institute (MI) Inflationary Expectations are now reported as a 30% symmetric trimmed mean utilising all responses except for the ‘don’t know’ responses.

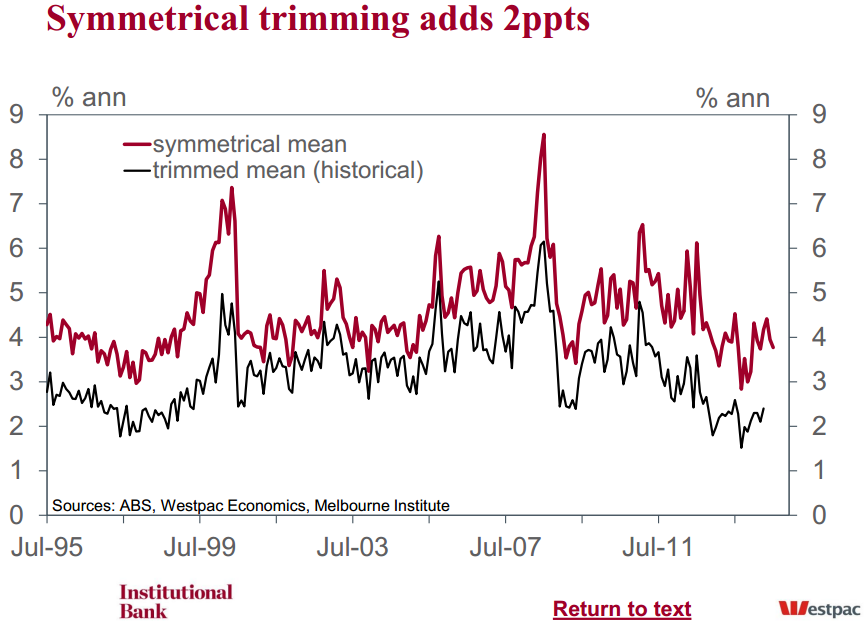

These changes have added about 2ppt to the level of the index compared to the old trimmed mean (chart 6). But more importantly, the new series appears to express a greater cyclical amplitude (chart 7 & 8) which is useful in picking turning points in the inflation cycle.

The consumer expected inflation rate fell by 0.2ppts to 3.8% in Jul. The trend of the trimmed mean series fell 0.1ppt to 4.0% in Jul; Jun was revised down to 4.1% from 4.2% and May has been revised down from an original estimate of 4.3% to 4.1%.

The trend series had been narrowing in on the long run average of 4.5% (chart 10) but this has since reversed. Too early to call a new trend but expectations are still below the long-run average.

Well that’s kind of confusing but appears to mean that expectations remain anchored.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.