From Citi today comes a nicely reasoned base case for China:

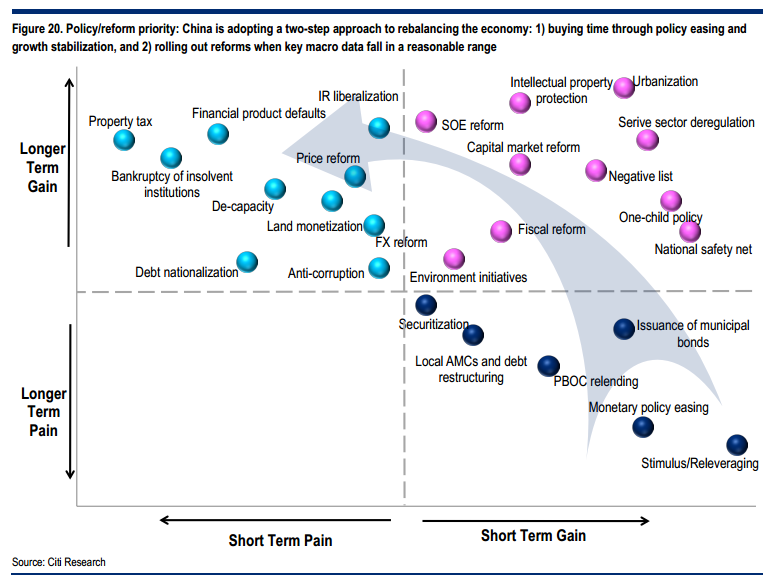

A tricky path, with cliffs on both sides – With a painful correction unfurling in the domestic property/construction sector, China officials are likely to accept stimulus risks and focus on cyclical policy measures to manage economic growth downside, with targeted actions to increase property demand while keeping monetary and credit conditions accommodative. A mild growth rebound is likely in 2H, but could be transitory, and we expect further moderation in 2015. More policy easing, including policy rate cuts in 1H15, looks likely to avoid risks of slipping into a hard-landing. Structural reform is meanwhile not forgotten, and the pace of reform has picked up a bit recently with a rough timetable of hukou, fiscal and SOE reforms emerging – but these measures are unlikely to be near-term game-changers, and structural reform initiatives will be taken slowly, cautiously.

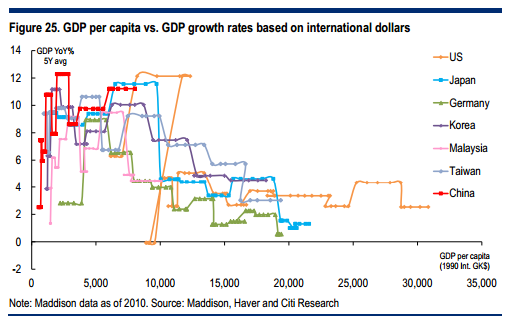

At a structural inflection point – International experiences suggest that GDP growth rates are often halved once GDP per capita hits the 10k international dollar mark. China is right at this inflection point. We believe China’s GDP growth is likely in the transition phase to a “new normal” of 5-6% in next five or so years as traditional growth drivers such as investment and exports are normalizing. China’s leaders are determined to sustain a growth mandate, targeting to double China’s 2010 GDP in real terms by 2020, implying at least 6.8% annual growth.

Putting a floor on growth rates – We see three key factors that should ensure growth does not decelerate too much in coming years:

– The cost of capital may be volatile but should trend down, which implies rate cuts, PBOC balance sheet expansion and an acceptable pace of re-leveraging.

– We assume a soft landing in the property sector, meaning around 10% property/construction investment growth.

– Reforms should be able to generate incremental demand and efficiency gains, lifting market/investor sentiment and confidence.

That is a very classy piece of analysis. Citi sees 7.5% this year and 7.1% next and then easing towards the new range over subsequent years.

I one have question. Citi’s key assumption is that to balance reform and growth priorities interest rates will fall. Given that that is the core of China’s investment imbalance – triggering capital mis-allocation, over-building, falling productivity and extend and pretend in the banking system – interest rates need to rise (at least in real terms) to ensure that finance moves to higher rates of return that sends capital towards productive businesses and so that household income is boosted to consume more and offset declining investment.

Advertisement

If so, growth will fall more quickly than Citi suggests, the investment component especially, though that does not necessarily imply crisis if household income is commensurately rising.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.