Cross-posted from Investing in Chinese Stocks.

A series of recent stories tells the tale of China’s ongoing property developer shakeout. From Hexun comes the latest months of supply data:

Beijing is far down the list, but it’s not stopping some new building from cutting prices by 20%. The new threat to home prices in Beijing is the government housing that sold for about one-third less than the surrounding real estate.

This highlights the wonders of central planning and government’s uncanny knack of closing the barn door well after the horses have run off. Beijing’s affordable housing, which was seen as a way to hold down real estate prices, is hitting the market just as the housing market has peaked. The extra supply selling at one-third off is going to act as an accelerant on the way down:

“Now our goal is quick turnover, do our best to grab as much demand as possible, because in the future there will be more affordable housing in the market, and by then it might be too late to cut prices again,” an executive from a mid-sized developer told reporters.

In Jinan, it’s been three months and no land sales, from Ifeng:

Even though prices haven’t tumbled in Jinan, land sales have ground to a halt. In Q1, Jinan residential real estate investment grew at 4.3%, down from 35.4% a year earlier.

And a Changsha developer is finding life very lonely suddenly:

AdvertisementAdvertisement

The number of trusts in the bar is left scale. Money raised is right scale. The dark blue at the bottom of the bars is real estate.

Same pattern with newly established trusts:

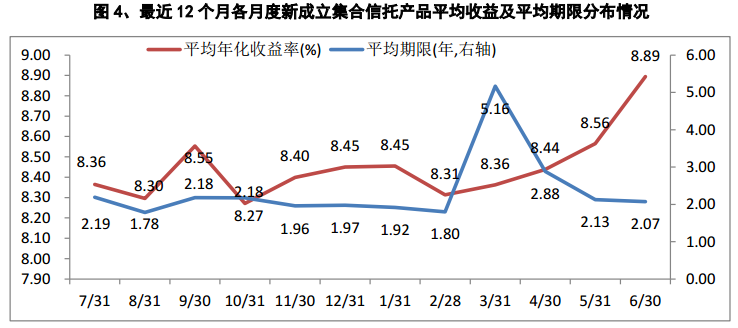

Here’s average maturity. Short-term trusts are disappearing:

Here’s average maturity and average interest rates. There’s your tight credit:

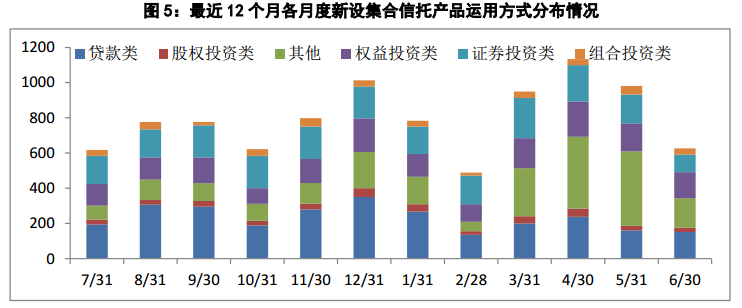

Here’s the type of trust by structure. Dark blue are loans and the light blue is securities, which includes debt. The average maturity of the securities class of trusts jumped from 1.71 years to 4.09 years in June.