BofAML has useful inventory of the burgeoning Chinese housing policy supports today:

Weak property market calls for more concerns

The Minister of Housing and Urban-Rural Development (MOHURD), Chen Zhenggao, said on 18 July that one of the top priorities would be destocking of the housing market. A focus on sales may imply further price cuts or discounts, adding to the price concern.

The property market remains the major downturn risk for the Chinese economy, in our view. As one of the mini-stimulus measures, the PBoC has requested since mid-May that commercial banks lower mortgage rates and provide more credit to first-time home buyers. However, it remains doubtful if commercial banks have answered the PBoC’s call, with new medium- to long-term loans to households (mainly mortgage loans) barely rising in June from May.

A lot more cities eased restrictions

Evidence of countercyclical policy could be found in the hands of local governments. To boost housing sales, local governments may have strong motives to relax or remove HPRs…By 29 July, there were 33 cities that adjusted HPRs out of 46 cities. We expect more to come in support of home sales…The first two cities that removed HPRs, Hohhot and Jinan, saw average daily sales rise by 60% and 100%, respectively, following the move.

Mortgage rate is another key to demand

Signs of relaxed loan conditions have also come through recently. According to reports by the 21st Century Business Herald, Agriculture Bank of China (ABC) Shanghai will grant mortgages at 0.95x the benchmark rate to those with mortgage amounts greater than RMB2mn, regardless of primary or secondary housing, effective from August. Various sources point to even bigger discounts (10-15%) at smaller banks, including Minsheng Banks and Citic Bank. Moreover, loan approval has been made faster, according to a survey by Centaline.

Supply side fine-tuning: bond and ABS issuance

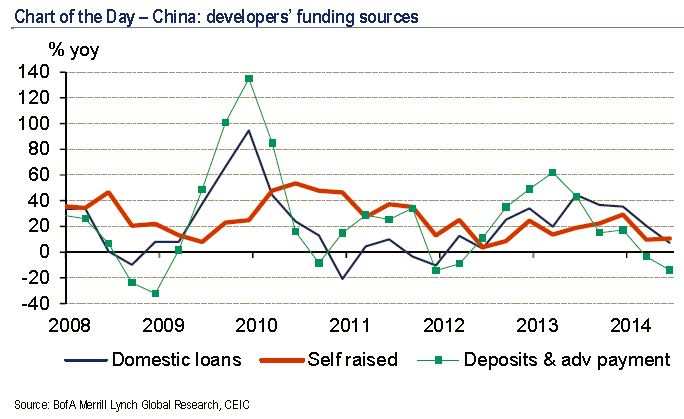

Property developers have suffered from fewer sources of funding into 2014, thanks to precautions by banks and a high base of sales proceeds in 2013 (Chart 1). Stock offerings and bond issuance have been not an option for developers since 2010 and 2009, respectively. The ongoing targeted easing still excluded developers as borrowers…On the funding channels front, a series of new findings are worth noting. In April, Tianjin Realty Development Group Co. issued an RMB1.2bn corporate bond, the first case in the past five years. Another developer issued an RMB2bn bond last week, suggesting an orderly removal of funding restrictions to developers.

Uncertainties ahead

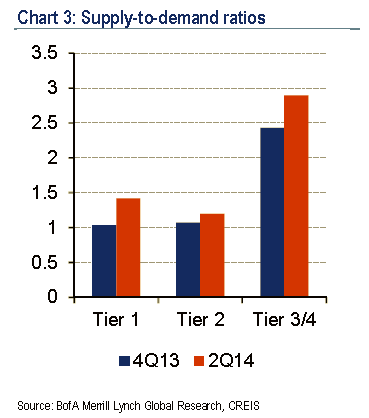

The contribution to headline growth by the property sector is likely to fall, not to mention the impact on related industries such as building materials…The residential house supply-to-demand ratio has risen remarkably for all categories in the past six months (Chart 3). Further slowing in the property sector is worth a close watch. In this regard, policy support could have been upgraded to resist the downward trend.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.