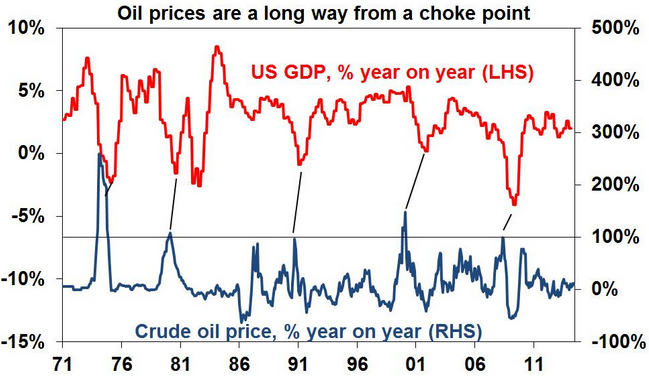

Yesterday Shane Oliver produced the following chart to assuage fears that a spiking oil price could impact global growth:

The assumption in this chart is that it is the year on year change in oil prices that hurts growth. There are two possible channels for that. If the year-on-year change is high then it flows into inflation and causes interest rate rises. Given the consistently high oil price over the past few years that’s not a danger this time around so fair enough.

The second channel is still in force, however, and that’s the transfer of income from non-oil-producing states to oil-producers. Capital Economics points out today that that is not without cost:

…surges in oil prices are usually soon followed by a slowdown in economic activity. Every $10 rise in the price of a barrel of oil transfers an amount equivalent to around 0.5% of world GDP from oil consumers to oil producers. This in turn dampens global demand because producers of oil generally spend a lower proportion of their income than consumers. We suggest that, as a rule of thumb, the net impact of a $10 rise in oil prices is to cut global growth by around 0.2-0.3 percentage points…it seems reasonable to flag up $120 as the danger point for the global economy if the Iraq crisis escalates and oil prices continue to climb on fears of further supply disruption.

For Australia the equation is further complicated by the dollar. As it falls in the year ahead, the oil price is likely to rise significantly year-on-year and it is one of the channels through which tradable inflation appears most swiftly in the economy. The RBA won’t be raising interest rates whatever happens. But it has shown a strong dispensation to prioritise inflation ahead of growth so an enduring oil price spike, which seems likely, will put further pressure on the bank to not cut rates.

Thus, the rising oil price weighs against my rate cut forecast for later this year but I still see it given the magnitude of growth fade coming down the pipe. Having said that, over time, oil is shaping as another factor preventing the RBA from addressing the economy’s real problem in a timely manner: the over-valued real exchange rate.