Right now markets don’t care about anything. They’re satisfied that all risks are contained and are pursuing the” trend is your friend” strategy that has dominated since the rise of Alan Greenspan. Everyone now expects only a gentle rise in US interest rates and wider risks only reinforce this assumption. As such, everyone is partying on one side of the ship, drunk and rowdy, as the seas remain calm.

Last week a few ripples appeared on the horizon in the form of restive US inflation. It appears to be a minor swell just now but the implications are enormous if it builds so is definitely worthy of a closer look. If this swell does build, and the US Federal Reserve is forced to hike rate earlier than currently expected, about a year away, then markets will rush to the other side of the ship. The results are predictable. From the FT:

In an age of abundant liquidity, when financial markets are humming as never before, the idea that trade in emerging market debt could seize up might seem unlikely.

But that is what some analysts are warning is at risk of happening in EM secondary debt markets, where bonds that have already been issued are bought and sold. The result could be a disorderly sell-off across EM assets if – as is widely expected – US interest rates start to rise.

The flood of global liquidity provided under quantitative easing by the US Federal Reserve and other central banks has supported a huge increase in bond issuance by EM governments and companies. Such issuance was already on the rise before the global crisis of 2008-09, as new investors came to emerging markets in search of higher yields.

The outstanding volume of EM debt rose from $650bn in 2001 to nearly $6.9tn at the end of last year, according to the Bank for International Settlements.

…The exit, when it comes, looks like being crowded. Buying bonds on primary markets – where they are issued – is one thing. But selling them on secondary markets is another. As EM issuance has increased over the past decade, daily trading volume as a proportion of the outstanding debt has declined.

…“It’s an asymmetrical market and it’s becoming increasingly difficult,” says Timothy Ash, EM strategist at Standard Bank. “The sell side is unable to provide liquidity and there is a much bigger buy side on the other side.”

Advertisement

An early US rate hike would trigger a rerun of last year’s “taper tantrum” but more so with the Australian dollar tumbling with commodity currencies, equities under pressure and bond yields jumping worldwide.

So, how likely is it? Westpac’s Elliot Clarke looked at US inflation dynamics last week:

…the CPI, which has risen from 1.6% in March to 2.6% in May. The FOMC’s preferred PCE measure has experienced a more modest acceleration, from 1.3% to 1.9%, leaving it just below the FOMC’s medium-term target.

This is not the first time we have seen such a pick-up in inflation in the post-GFC environment: 6-month annualised headline PCE and CPI inflation spiked to 3.5% and 5.0% in mid-2011 following a marked depreciation in the USD, a trend not apparent currently. Instead, the stabilisation of the USD on a TWI basis through 2014 following a notable appreciation against emerging markets in mid-2013 has only reduced its dampening influence on the price of imported goods, and therefore inflation. A simple proxy for this effect is the goods excluding energy and food category of the CPI, which has risen from –0.9% in February to –0.2% in May.

Relative to 2011 then, domestic inflation factors look to be having a much more significant role. To the extent that the unemployment rate is currently at 6.3% compared to around 9.0% in mid-2011, it is hardly surprising that a closing output gap driven by stronger demand has been seen by many as the cause. The crux of the matter then is twofold: is the obvious explanation also the correct one regarding where this inflation is coming from; and following on, how likely is it to persist?

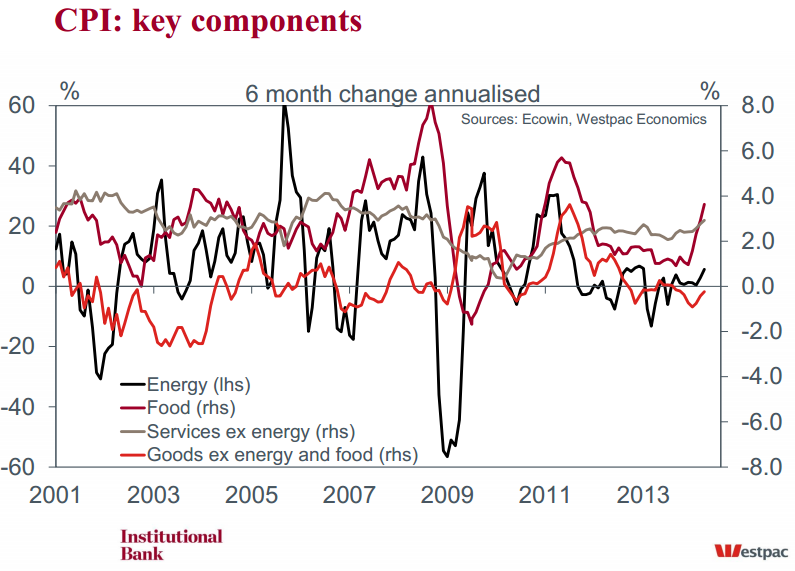

Delving into the inflation component detail, we see that the real action has been around food; energy; housing; and transport. For food, we note that the 6-month annualised pace of CPI inflation has risen from 1.0% in January to 3.6% as at May. Energy inflation has similarly jumped from 0.4% at March to 5.7% at May. Housing and transport costs are included in the CPI’s services ex energy component, which has seen inflation rise from 2.4% at December 2013 to 2.9% currently – a modest move in scale but not in aggregate effect, owing to the weight of the shelter component in the CPI.

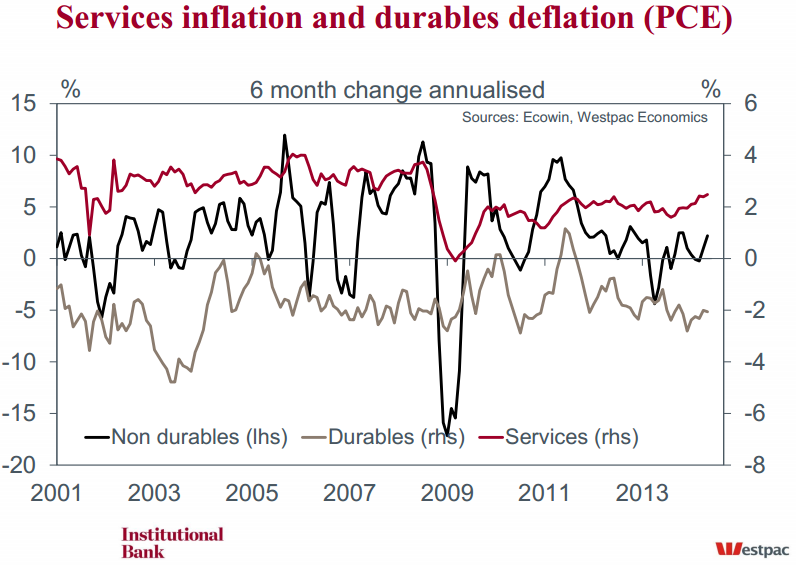

Switching to the PCE inflation data, we see that the pick-up in inflation through the first half of 2014 has been centred in services prices. Putting this observation together with the CPI trends noted above alludes to the housing and food services components being the driving force behind the rise in headline inflation. This is borne out in the PCE detail, with the pace of housing & utilities (housing) inflation accelerating sharply from 2.3% in December 2013 to 3.7% in May. Similarly, food services & accommodation (food services) price growth has almost quadrupled over the period, from 1.0% to 3.6% in May.

In both instances, it seems as though these price movements have not been driven by demand. This is particularly true for food services, which has seen growth in consumption volumes fall from 5.3% in November to –0.6% in May. Housing and utility demand has remained highly volatile, but there was no evidence of a ‘break out’ move in this component of personal consumption in early 2014, and growth has since slumped back to 0.2%. (This is not to say that rents have not contributed materially to the level of housing inflation in recent years; more below.)

This then points to an exogenous shock being to blame for the recent jump. Further, the coincident nature of the inflation uptrends for food and housing services alludes to a common cause: the cost of energy. The 6.1% gain in total PCE energy prices from April 2013 to May 2014 corroborates this belief. To the extent that shifts in energy costs typically prove temporary, this inflationary impulse will likely dissipate in coming months – leaving aside current geopolitical concerns.

However, in considering the 2014 outlook, there are a number of potential upside risks which need to be kept in mind.

Beginning with the all-important housing component, its persistent uptrend since September 2009 points to more than energy costs being to blame. House prices have increased by a reasonable amount from the trough, and the growing role of large investors in the property market, alongside declining home ownership, have reduced the supply glut in the overall market – the net result being rising rents. “Owner’s equivalent rent” is a major driver of the CPI, and while the housing sector remains expansionary, it will be a defence against a return to a deflation scare. On the other hand, our reading of the lack of momentum in activity at present implies that it is unlikely to be the source of a demand-driven uplift in aggregate inflation above the FOMC’s target.

In addition, there is the impact of the ‘other’ major US weather event (the West Coast drought) on the price of food: note that PCE food goods inflation has risen from 0.3% in January to 3.4% in May. The persistence and scale of this phenomenon makes a protracted period of high food inflation a real risk.

Finally, there is the potential impact of minimum wage claims and the introduction of ‘Affordable Health Care’. These are yet two more factors which could, in part, be behind the inflation uptrend in the key service categories discussed above. These social trends are only just beginning to take effect, and their cumulative impact will only be known with time.

Overall, available evidence points to the recent acceleration in inflation pressures being driven principally by transitory factors. This is consistent with the weak pace of underlying activity growth we have discussed over the last two weeks. As has long been our expectation, the result would be inflation outcomes locked within a narrow band, with its upper bound the 2.0% target.

Advertisement

That’s a sound summary and I agree. Some food prices are already retracing sharply (wheat has tanked) so there are downside food price risks as well despite the weather. But oil will remain under upward pressure as the new proxy war doctrine takes hold in energy-centric global regions. That said, so long as the pricing pressure is a one-off jump rather than a chronic building in prices, the Fed will be able to “look through” the effects. Indeed, Janet Yellen has already intimated as much:

GREG IP. Madam Chair, Greg Ip of the Economist… How would the Committee respond if inflation did temporarily move above target in the near term before you achieve full employment?Your colleague John Williams and the IMF have both suggested that the Committee might consider allowing inflation to temporarily overshoot because that might achieve a faster, larger improvement in employment.

CHAIR YELLEN. So with respect to the question of overshooting, let me start by saying that inflation continues to run well below our objective, and we’re still some ways away from maximum employment. And for the moment, I don’t see any tradeoff whatsoever in achieving our two objectives. They both call for the same policy—namely, a highly accommodative monetary policy. …

Now, quite some time ago, the FOMC adopted, and we reaffirmed just in January, a statement on our longer-run goals and policy strategy. And what that statement said is that, first of all, whenever either inflation or employment are away from their preferred or mandate-consistent levels, it will always be the FOMC’s policy to make sure that we get back to those target levels over the medium term. But a principle that’s embodied in that statement is that the Committee will follow a so-called balanced approach in deciding on its policies. And, essentially, that means that when we see some conflict between achieving the two objectives, that we would consider in deciding on a policy just how far we are from achieving each of the objectives. And if the distance from achieving an objective is particularly large, it would be consistent with a balanced approach that we would tolerate some movement in the opposite direction on the other objective.

So, “look through” is quite possible and US bond yields have, if anything, fallen since this became as issue, reinforcing the “all good” view.

Advertisement

Of course, what we’re really talking about here is the timing of this crisis. One way or another it’s inevitable. The very absence of it ensures that it will happen in the long run, all the more severely. At this stage, at least, we can still be relatively comfortable that that is still in the medium term.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.